#include <singlefactorbsmbasketengine.hpp>

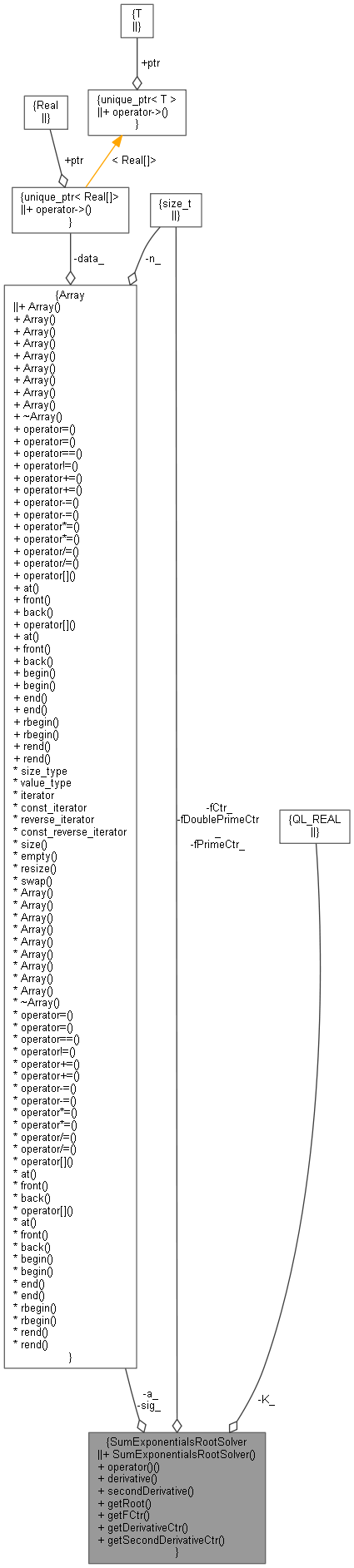

Collaboration diagram for SumExponentialsRootSolver:

Collaboration diagram for SumExponentialsRootSolver:

Public Types | |

| enum | Strategy { Ridder , Newton , Brent , Halley } |

Public Member Functions | |

| SumExponentialsRootSolver (Array a, Array sig, Real K) | |

| Real | operator() (Real x) const |

| Real | derivative (Real x) const |

| Real | secondDerivative (Real x) const |

| Real | getRoot (Real xTol=1e6 *QL_EPSILON, Strategy strategy=Brent) const |

| Size | getFCtr () const |

| Size | getDerivativeCtr () const |

| Size | getSecondDerivativeCtr () const |

Private Attributes | |

| const Array | a_ |

| const Array | sig_ |

| const Real | K_ |

| Size | fCtr_ = 0 |

| Size | fPrimeCtr_ = 0 |

| Size | fDoublePrimeCtr_ = 0 |

Detailed Description

Definition at line 57 of file singlefactorbsmbasketengine.hpp.

Member Enumeration Documentation

◆ Strategy

| enum Strategy |

| Enumerator | |

|---|---|

| Ridder | |

| Newton | |

| Brent | |

| Halley | |

Definition at line 59 of file singlefactorbsmbasketengine.hpp.

Constructor & Destructor Documentation

◆ SumExponentialsRootSolver()

| SumExponentialsRootSolver | ( | Array | a, |

| Array | sig, | ||

| Real | K | ||

| ) |

Definition at line 36 of file singlefactorbsmbasketengine.cpp.

Here is the call graph for this function:

Member Function Documentation

◆ operator()()

Definition at line 43 of file singlefactorbsmbasketengine.cpp.

Here is the call graph for this function:

◆ derivative()

Definition at line 52 of file singlefactorbsmbasketengine.cpp.

Here is the call graph for this function:

◆ secondDerivative()

Definition at line 61 of file singlefactorbsmbasketengine.cpp.

Here is the call graph for this function:

◆ getRoot()

| Real getRoot | ( | Real | xTol = 1e6*QL_EPSILON, |

| Strategy | strategy = Brent |

||

| ) | const |

Definition at line 82 of file singlefactorbsmbasketengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ getFCtr()

| Size getFCtr | ( | ) | const |

Definition at line 70 of file singlefactorbsmbasketengine.cpp.

◆ getDerivativeCtr()

| Size getDerivativeCtr | ( | ) | const |

Definition at line 74 of file singlefactorbsmbasketengine.cpp.

◆ getSecondDerivativeCtr()

| Size getSecondDerivativeCtr | ( | ) | const |

Definition at line 78 of file singlefactorbsmbasketengine.cpp.

Member Data Documentation

◆ a_

|

private |

Definition at line 74 of file singlefactorbsmbasketengine.hpp.

◆ sig_

|

private |

Definition at line 74 of file singlefactorbsmbasketengine.hpp.

◆ K_

|

private |

Definition at line 75 of file singlefactorbsmbasketengine.hpp.

◆ fCtr_

|

mutableprivate |

Definition at line 76 of file singlefactorbsmbasketengine.hpp.

◆ fPrimeCtr_

|

private |

Definition at line 76 of file singlefactorbsmbasketengine.hpp.

◆ fDoublePrimeCtr_

|

private |

Definition at line 76 of file singlefactorbsmbasketengine.hpp.