Inheritance diagram for BasketGeneratingEngine::MatchHelper:

Inheritance diagram for BasketGeneratingEngine::MatchHelper: Collaboration diagram for BasketGeneratingEngine::MatchHelper:

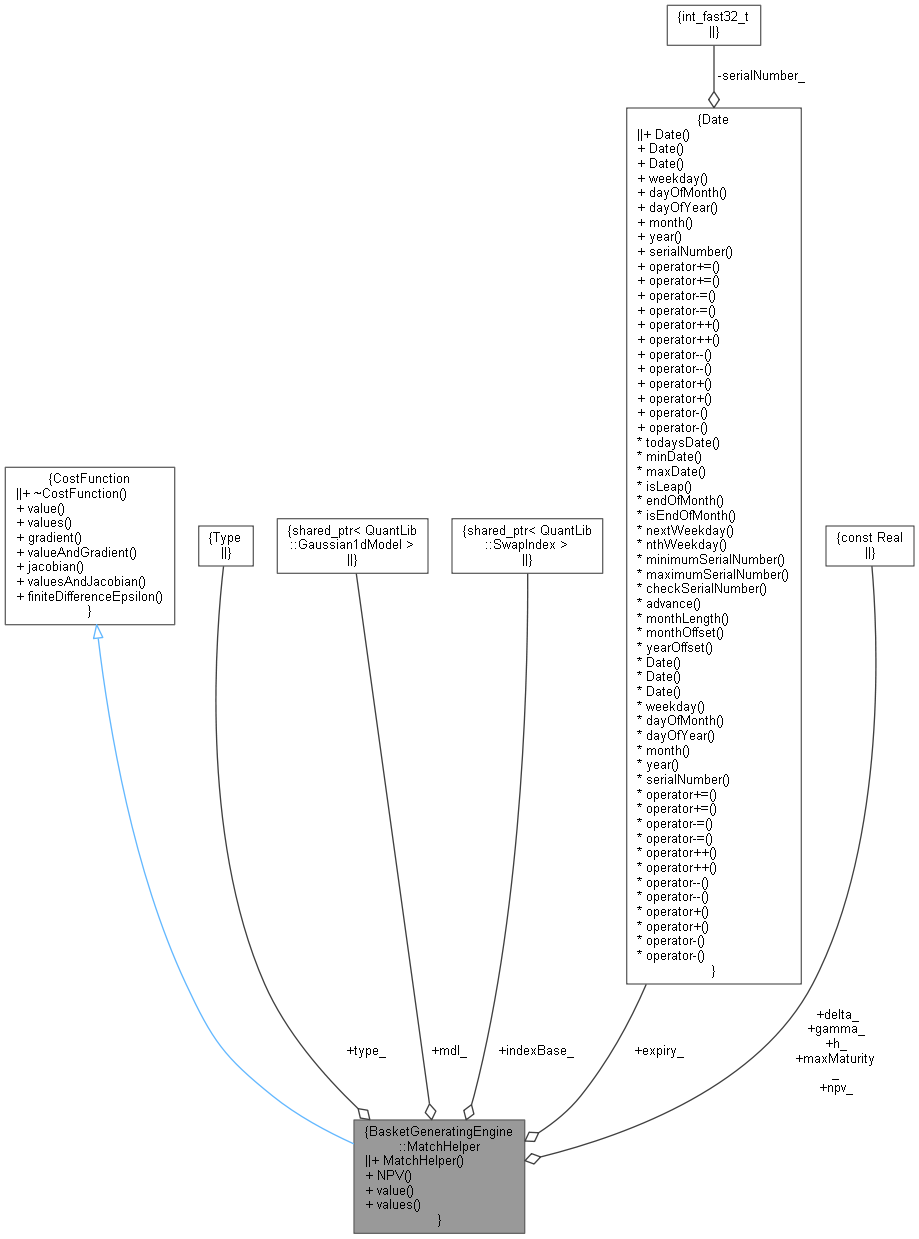

Collaboration diagram for BasketGeneratingEngine::MatchHelper:

Public Member Functions | |

| MatchHelper (const Swap::Type type, const Real npv, const Real delta, const Real gamma, ext::shared_ptr< Gaussian1dModel > model, ext::shared_ptr< SwapIndex > indexBase, const Date &expiry, const Real maxMaturity, const Real h) | |

| Real | NPV (const ext::shared_ptr< VanillaSwap > &swap, Real fixedRate, Real nominal, Real y, int type) const |

| Real | value (const Array &v) const override |

| method to overload to compute the cost function value in x More... | |

| Array | values (const Array &v) const override |

| method to overload to compute the cost function values in x More... | |

| Public Member Functions inherited from CostFunction | |

| virtual | ~CostFunction ()=default |

| virtual Real | value (const Array &x) const |

| method to overload to compute the cost function value in x More... | |

| virtual Array | values (const Array &x) const =0 |

| method to overload to compute the cost function values in x More... | |

| virtual void | gradient (Array &grad, const Array &x) const |

| method to overload to compute grad_f, the first derivative of More... | |

| virtual Real | valueAndGradient (Array &grad, const Array &x) const |

| method to overload to compute grad_f, the first derivative of More... | |

| virtual void | jacobian (Matrix &jac, const Array &x) const |

| method to overload to compute J_f, the jacobian of More... | |

| virtual Array | valuesAndJacobian (Matrix &jac, const Array &x) const |

| method to overload to compute J_f, the jacobian of More... | |

| virtual Real | finiteDifferenceEpsilon () const |

| Default epsilon for finite difference method : More... | |

Public Attributes | |

| const Swap::Type | type_ |

| const ext::shared_ptr< Gaussian1dModel > | mdl_ |

| const ext::shared_ptr< SwapIndex > | indexBase_ |

| const Date | expiry_ |

| const Real | maxMaturity_ |

| const Real | npv_ |

| const Real | delta_ |

| const Real | gamma_ |

| const Real | h_ |

Detailed Description

Definition at line 101 of file basketgeneratingengine.hpp.

Constructor & Destructor Documentation

◆ MatchHelper()

| MatchHelper | ( | const Swap::Type | type, |

| const Real | npv, | ||

| const Real | delta, | ||

| const Real | gamma, | ||

| ext::shared_ptr< Gaussian1dModel > | model, | ||

| ext::shared_ptr< SwapIndex > | indexBase, | ||

| const Date & | expiry, | ||

| const Real | maxMaturity, | ||

| const Real | h | ||

| ) |

Definition at line 103 of file basketgeneratingengine.hpp.

Member Function Documentation

◆ NPV()

| Real NPV | ( | const ext::shared_ptr< VanillaSwap > & | swap, |

| Real | fixedRate, | ||

| Real | nominal, | ||

| Real | y, | ||

| int | type | ||

| ) | const |

Definition at line 116 of file basketgeneratingengine.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

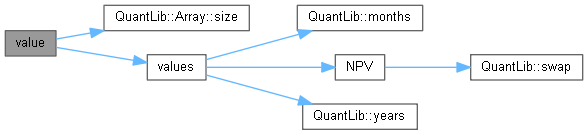

◆ value()

method to overload to compute the cost function value in x

Reimplemented from CostFunction.

Definition at line 142 of file basketgeneratingengine.hpp.

Here is the call graph for this function:

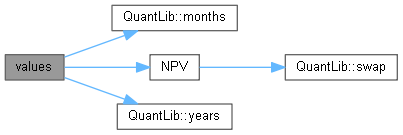

◆ values()

method to overload to compute the cost function values in x

Implements CostFunction.

Definition at line 151 of file basketgeneratingengine.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ type_

| const Swap::Type type_ |

Definition at line 225 of file basketgeneratingengine.hpp.

◆ mdl_

| const ext::shared_ptr<Gaussian1dModel> mdl_ |

Definition at line 226 of file basketgeneratingengine.hpp.

◆ indexBase_

| const ext::shared_ptr<SwapIndex> indexBase_ |

Definition at line 227 of file basketgeneratingengine.hpp.

◆ expiry_

| const Date expiry_ |

Definition at line 228 of file basketgeneratingengine.hpp.

◆ maxMaturity_

| const Real maxMaturity_ |

Definition at line 229 of file basketgeneratingengine.hpp.

◆ npv_

| const Real npv_ |

Definition at line 230 of file basketgeneratingengine.hpp.

◆ delta_

| const Real delta_ |

Definition at line 230 of file basketgeneratingengine.hpp.

◆ gamma_

| const Real gamma_ |

Definition at line 230 of file basketgeneratingengine.hpp.

◆ h_

| const Real h_ |

Definition at line 230 of file basketgeneratingengine.hpp.