#include <btp.hpp>

Inheritance diagram for RendistatoCalculator:

Inheritance diagram for RendistatoCalculator: Collaboration diagram for RendistatoCalculator:

Collaboration diagram for RendistatoCalculator:

Public Member Functions | |

| RendistatoCalculator (ext::shared_ptr< RendistatoBasket > basket, ext::shared_ptr< Euribor > euriborIndex, Handle< YieldTermStructure > discountCurve) | |

Calculations | |

| Rate | yield () const |

| Time | duration () const |

| const std::vector< Rate > & | yields () const |

| const std::vector< Time > & | durations () const |

| const std::vector< Time > & | swapLengths () const |

| const std::vector< Rate > & | swapRates () const |

| const std::vector< Rate > & | swapYields () const |

| const std::vector< Time > & | swapDurations () const |

Equivalent Swap proxy | |

| ext::shared_ptr< VanillaSwap > | equivalentSwap () const |

| Rate | equivalentSwapRate () const |

| Rate | equivalentSwapYield () const |

| Time | equivalentSwapDuration () const |

| Time | equivalentSwapLength () const |

| Spread | equivalentSwapSpread () const |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

LazyObject interface | |

| ext::shared_ptr< RendistatoBasket > | basket_ |

| ext::shared_ptr< Euribor > | euriborIndex_ |

| Handle< YieldTermStructure > | discountCurve_ |

| std::vector< Rate > | yields_ |

| std::vector< Time > | durations_ |

| Time | duration_ |

| Size | equivalentSwapIndex_ |

| Size | nSwaps_ = 15 |

| std::vector< ext::shared_ptr< VanillaSwap > > | swaps_ |

| std::vector< Time > | swapLengths_ |

| std::vector< Time > | swapBondDurations_ |

| std::vector< Rate > | swapBondYields_ |

| std::vector< Rate > | swapRates_ |

| void | performCalculations () const override |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

Constructor & Destructor Documentation

◆ RendistatoCalculator()

| RendistatoCalculator | ( | ext::shared_ptr< RendistatoBasket > | basket, |

| ext::shared_ptr< Euribor > | euriborIndex, | ||

| Handle< YieldTermStructure > | discountCurve | ||

| ) |

Member Function Documentation

◆ yield()

| Rate yield | ( | ) | const |

◆ duration()

| Time duration | ( | ) | const |

◆ yields()

| const std::vector< Rate > & yields | ( | ) | const |

◆ durations()

| const std::vector< Time > & durations | ( | ) | const |

◆ swapLengths()

◆ swapRates()

| const std::vector< Rate > & swapRates | ( | ) | const |

◆ swapYields()

| const std::vector< Rate > & swapYields | ( | ) | const |

◆ swapDurations()

| const std::vector< Time > & swapDurations | ( | ) | const |

◆ equivalentSwap()

| ext::shared_ptr< VanillaSwap > equivalentSwap | ( | ) | const |

◆ equivalentSwapRate()

| Rate equivalentSwapRate | ( | ) | const |

◆ equivalentSwapYield()

| Rate equivalentSwapYield | ( | ) | const |

◆ equivalentSwapDuration()

| Time equivalentSwapDuration | ( | ) | const |

◆ equivalentSwapLength()

| Time equivalentSwapLength | ( | ) | const |

◆ equivalentSwapSpread()

| Spread equivalentSwapSpread | ( | ) | const |

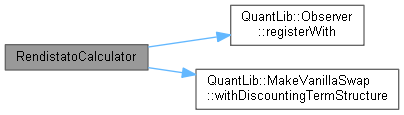

◆ performCalculations()

|

overrideprotectedvirtual |

This method must implement any calculations which must be (re)done in order to calculate the desired results.

Implements LazyObject.

Definition at line 156 of file btp.cpp.

Here is the call graph for this function:

Member Data Documentation

◆ basket_

|

private |

◆ euriborIndex_

◆ discountCurve_

|

private |

◆ yields_

◆ durations_

◆ duration_

◆ equivalentSwapIndex_

◆ nSwaps_

◆ swaps_

|

mutableprivate |