#include <fdmblackscholesmesher.hpp>

|

| | FdmBlackScholesMesher (Size size, const ext::shared_ptr< GeneralizedBlackScholesProcess > &process, Time maturity, Real strike, Real xMinConstraint=Null< Real >(), Real xMaxConstraint=Null< Real >(), Real eps=0.0001, Real scaleFactor=1.5, const std::pair< Real, Real > &cPoint={ Null< Real >(), Null< Real >() }, const DividendSchedule ÷ndSchedule={}, const ext::shared_ptr< FdmQuantoHelper > &fdmQuantoHelper={}, Real spotAdjustment=0.0) |

| |

| | Fdm1dMesher (Size size) |

| |

| virtual | ~Fdm1dMesher ()=default |

| |

| Size | size () const |

| |

| Real | dplus (Size index) const |

| |

| Real | dminus (Size index) const |

| |

| Real | location (Size index) const |

| |

| const std::vector< Real > & | locations () const |

| |

Definition at line 39 of file fdmblackscholesmesher.hpp.

◆ FdmBlackScholesMesher()

| FdmBlackScholesMesher |

( |

Size |

size, |

|

|

const ext::shared_ptr< GeneralizedBlackScholesProcess > & |

process, |

|

|

Time |

maturity, |

|

|

Real |

strike, |

|

|

Real |

xMinConstraint = Null<Real>(), |

|

|

Real |

xMaxConstraint = Null<Real>(), |

|

|

Real |

eps = 0.0001, |

|

|

Real |

scaleFactor = 1.5, |

|

|

const std::pair< Real, Real > & |

cPoint = { Null<Real>(), Null<Real>() }, |

|

|

const DividendSchedule & |

dividendSchedule = {}, |

|

|

const ext::shared_ptr< FdmQuantoHelper > & |

fdmQuantoHelper = {}, |

|

|

Real |

spotAdjustment = 0.0 |

|

) |

| |

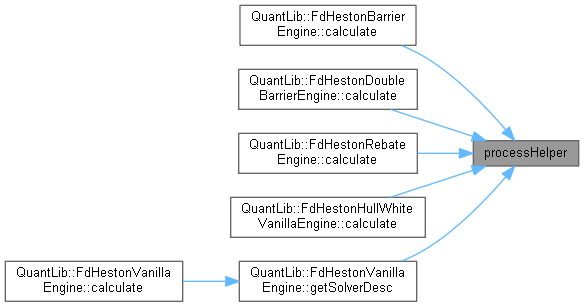

◆ processHelper()

Inheritance diagram for FdmBlackScholesMesher:

Inheritance diagram for FdmBlackScholesMesher: