Implied vol term structure at a given date in the future. More...

#include <impliedvoltermstructure.hpp>

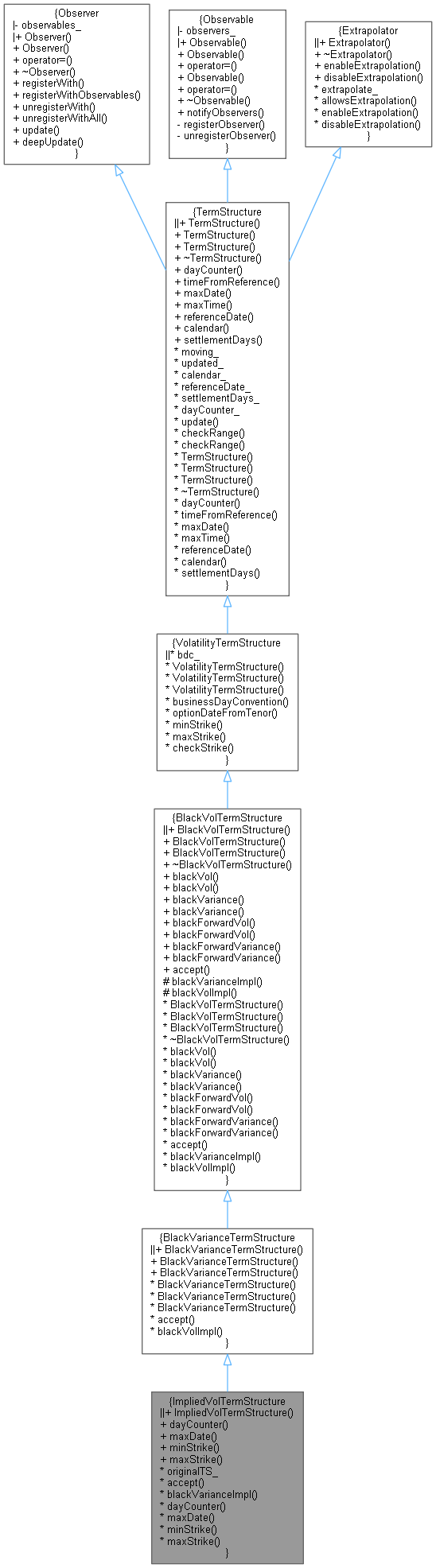

Inheritance diagram for ImpliedVolTermStructure:

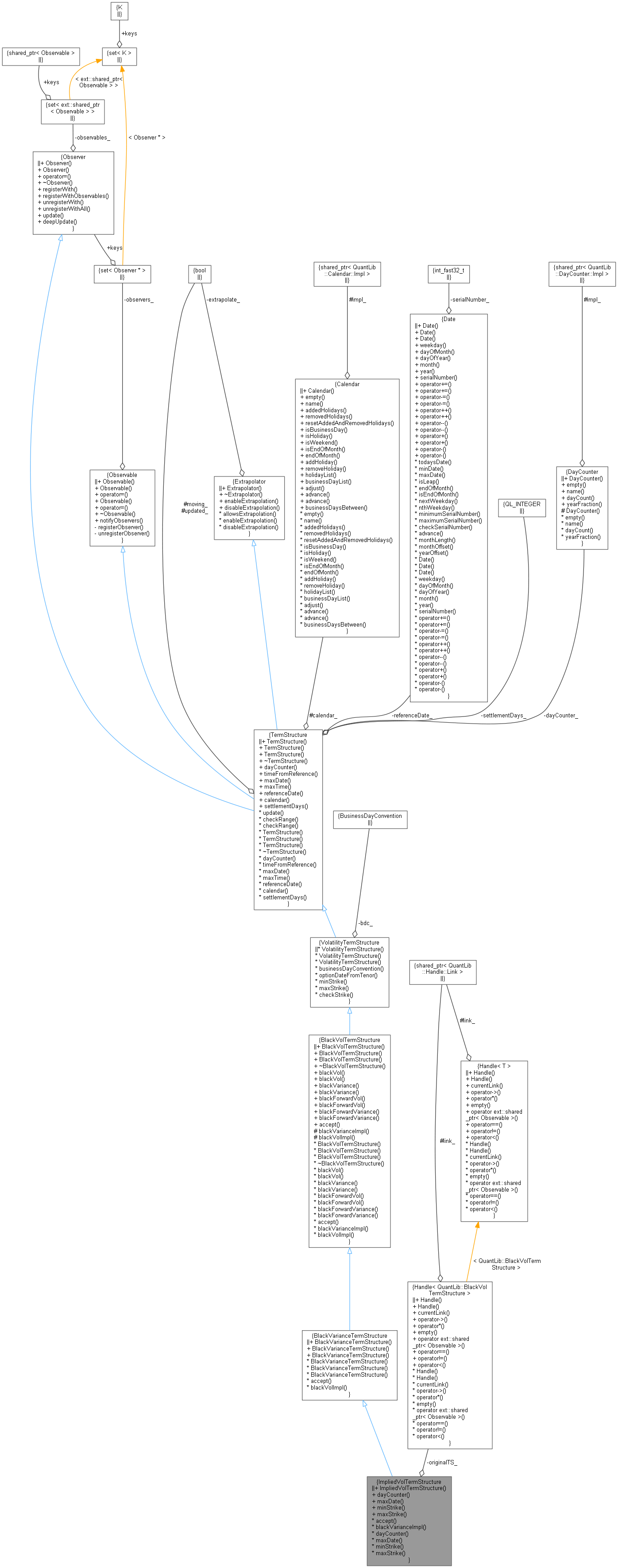

Inheritance diagram for ImpliedVolTermStructure: Collaboration diagram for ImpliedVolTermStructure:

Collaboration diagram for ImpliedVolTermStructure:

Public Member Functions | |

| ImpliedVolTermStructure (Handle< BlackVolTermStructure > origTS, const Date &referenceDate) | |

TermStructure interface | |

| DayCounter | dayCounter () const override |

| the day counter used for date/time conversion More... | |

| Date | maxDate () const override |

| the latest date for which the curve can return values More... | |

VolatilityTermStructure interface | |

| Real | minStrike () const override |

| the minimum strike for which the term structure can return vols More... | |

| Real | maxStrike () const override |

| the maximum strike for which the term structure can return vols More... | |

| Public Member Functions inherited from BlackVarianceTermStructure | |

| BlackVarianceTermStructure (BusinessDayConvention bdc=Following, const DayCounter &dc=DayCounter()) | |

| default constructor More... | |

| BlackVarianceTermStructure (const Date &referenceDate, const Calendar &cal=Calendar(), BusinessDayConvention bdc=Following, const DayCounter &dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| BlackVarianceTermStructure (Natural settlementDays, const Calendar &, BusinessDayConvention bdc=Following, const DayCounter &dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| Public Member Functions inherited from BlackVolTermStructure | |

| BlackVolTermStructure (BusinessDayConvention bdc=Following, const DayCounter &dc=DayCounter()) | |

| default constructor More... | |

| BlackVolTermStructure (const Date &referenceDate, const Calendar &cal=Calendar(), BusinessDayConvention bdc=Following, const DayCounter &dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| BlackVolTermStructure (Natural settlementDays, const Calendar &, BusinessDayConvention bdc=Following, const DayCounter &dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| ~BlackVolTermStructure () override=default | |

| Volatility | blackVol (const Date &maturity, Real strike, bool extrapolate=false) const |

| spot volatility More... | |

| Volatility | blackVol (Time maturity, Real strike, bool extrapolate=false) const |

| spot volatility More... | |

| Real | blackVariance (const Date &maturity, Real strike, bool extrapolate=false) const |

| spot variance More... | |

| Real | blackVariance (Time maturity, Real strike, bool extrapolate=false) const |

| spot variance More... | |

| Volatility | blackForwardVol (const Date &date1, const Date &date2, Real strike, bool extrapolate=false) const |

| forward (at-the-money) volatility More... | |

| Volatility | blackForwardVol (Time time1, Time time2, Real strike, bool extrapolate=false) const |

| forward (at-the-money) volatility More... | |

| Real | blackForwardVariance (const Date &date1, const Date &date2, Real strike, bool extrapolate=false) const |

| forward (at-the-money) variance More... | |

| Real | blackForwardVariance (Time time1, Time time2, Real strike, bool extrapolate=false) const |

| forward (at-the-money) variance More... | |

| Public Member Functions inherited from VolatilityTermStructure | |

| VolatilityTermStructure (BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| VolatilityTermStructure (const Date &referenceDate, const Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| VolatilityTermStructure (Natural settlementDays, const Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| virtual BusinessDayConvention | businessDayConvention () const |

| the business day convention used in tenor to date conversion More... | |

| Date | optionDateFromTenor (const Period &) const |

| period/date conversion More... | |

| Public Member Functions inherited from TermStructure | |

| TermStructure (DayCounter dc=DayCounter()) | |

| default constructor More... | |

| TermStructure (const Date &referenceDate, Calendar calendar=Calendar(), DayCounter dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| TermStructure (Natural settlementDays, Calendar, DayCounter dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| ~TermStructure () override=default | |

| Time | timeFromReference (const Date &date) const |

| date/time conversion More... | |

| virtual Time | maxTime () const |

| the latest time for which the curve can return values More... | |

| virtual const Date & | referenceDate () const |

| the date at which discount = 1.0 and/or variance = 0.0 More... | |

| virtual Calendar | calendar () const |

| the calendar used for reference and/or option date calculation More... | |

| virtual Natural | settlementDays () const |

| the settlementDays used for reference date calculation More... | |

| void | update () override |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Extrapolator | |

| Extrapolator ()=default | |

| virtual | ~Extrapolator ()=default |

| void | enableExtrapolation (bool b=true) |

| enable extrapolation in subsequent calls More... | |

| void | disableExtrapolation (bool b=true) |

| disable extrapolation in subsequent calls More... | |

| bool | allowsExtrapolation () const |

| tells whether extrapolation is enabled More... | |

Visitability | |

| Handle< BlackVolTermStructure > | originalTS_ |

| void | accept (AcyclicVisitor &) override |

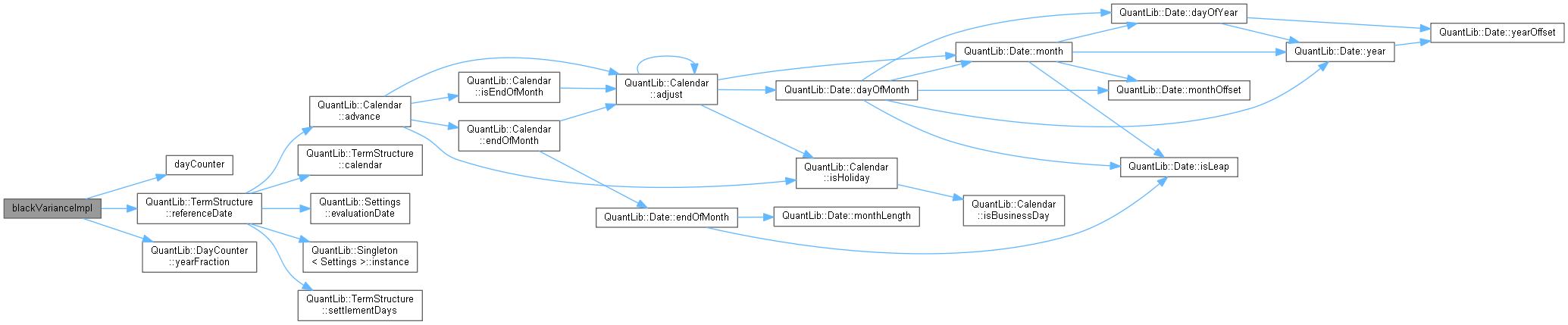

| Real | blackVarianceImpl (Time t, Real strike) const override |

| Black variance calculation. More... | |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from BlackVarianceTermStructure | |

| Volatility | blackVolImpl (Time t, Real strike) const override |

Calculations | |

These methods must be implemented in derived classes to perform the actual volatility calculations. When they are called, range check has already been performed; therefore, they must assume that extrapolation is required. | |

| Protected Member Functions inherited from VolatilityTermStructure | |

| void | checkStrike (Rate strike, bool extrapolate) const |

| strike-range check More... | |

| Protected Member Functions inherited from TermStructure | |

| void | checkRange (const Date &d, bool extrapolate) const |

| date-range check More... | |

| void | checkRange (Time t, bool extrapolate) const |

| time-range check More... | |

| Protected Attributes inherited from TermStructure | |

| bool | moving_ = false |

| bool | updated_ = true |

| Calendar | calendar_ |

Detailed Description

Implied vol term structure at a given date in the future.

The given date will be the implied reference date.

- Note

- This term structure will remain linked to the original structure, i.e., any changes in the latter will be reflected in this structure as well.

- Warning:

- It doesn't make financial sense to have an asset-dependant implied Vol Term Structure. This class should be used with term structures that are time dependant only.

Definition at line 43 of file impliedvoltermstructure.hpp.

Constructor & Destructor Documentation

◆ ImpliedVolTermStructure()

| ImpliedVolTermStructure | ( | Handle< BlackVolTermStructure > | origTS, |

| const Date & | referenceDate | ||

| ) |

Definition at line 70 of file impliedvoltermstructure.hpp.

Here is the call graph for this function:

Member Function Documentation

◆ dayCounter()

|

overridevirtual |

the day counter used for date/time conversion

Reimplemented from TermStructure.

Definition at line 48 of file impliedvoltermstructure.hpp.

Here is the caller graph for this function:

◆ maxDate()

|

overridevirtual |

the latest date for which the curve can return values

Implements TermStructure.

Definition at line 76 of file impliedvoltermstructure.hpp.

◆ minStrike()

|

overridevirtual |

the minimum strike for which the term structure can return vols

Implements VolatilityTermStructure.

Definition at line 80 of file impliedvoltermstructure.hpp.

◆ maxStrike()

|

overridevirtual |

the maximum strike for which the term structure can return vols

Implements VolatilityTermStructure.

Definition at line 84 of file impliedvoltermstructure.hpp.

◆ accept()

|

overridevirtual |

Reimplemented from BlackVarianceTermStructure.

Definition at line 88 of file impliedvoltermstructure.hpp.

Here is the call graph for this function:

◆ blackVarianceImpl()

Black variance calculation.

Implements BlackVolTermStructure.

Definition at line 96 of file impliedvoltermstructure.hpp.

Here is the call graph for this function:

Member Data Documentation

◆ originalTS_

|

private |

Definition at line 64 of file impliedvoltermstructure.hpp.