#include <correlationstructure.hpp>

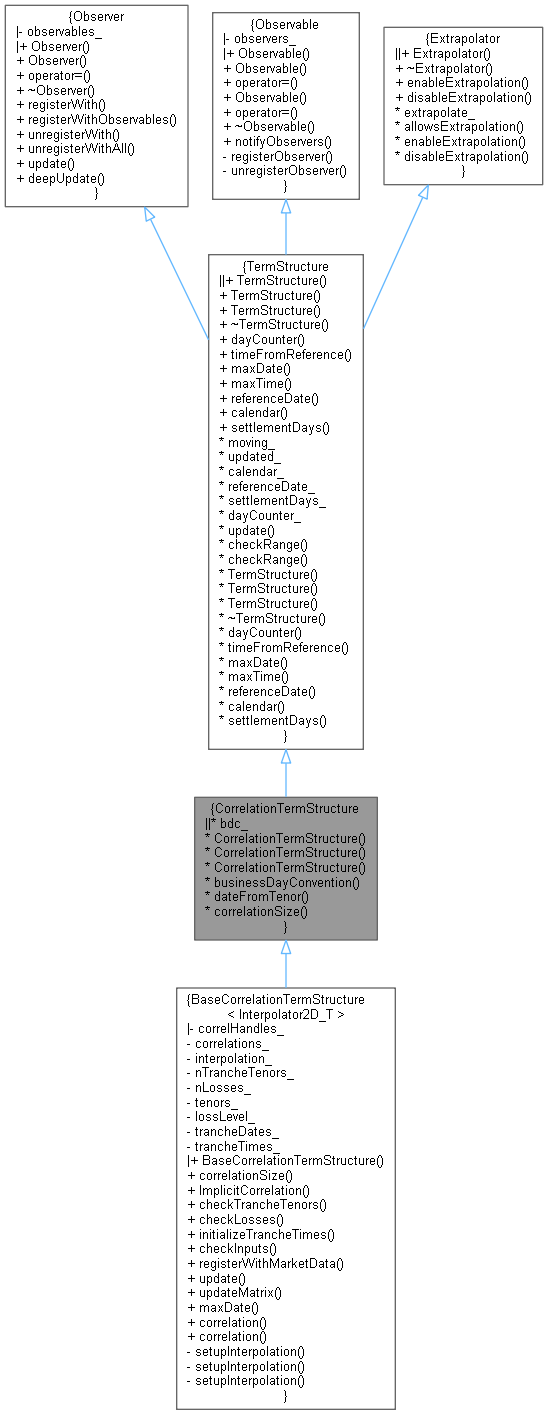

Inheritance diagram for CorrelationTermStructure:

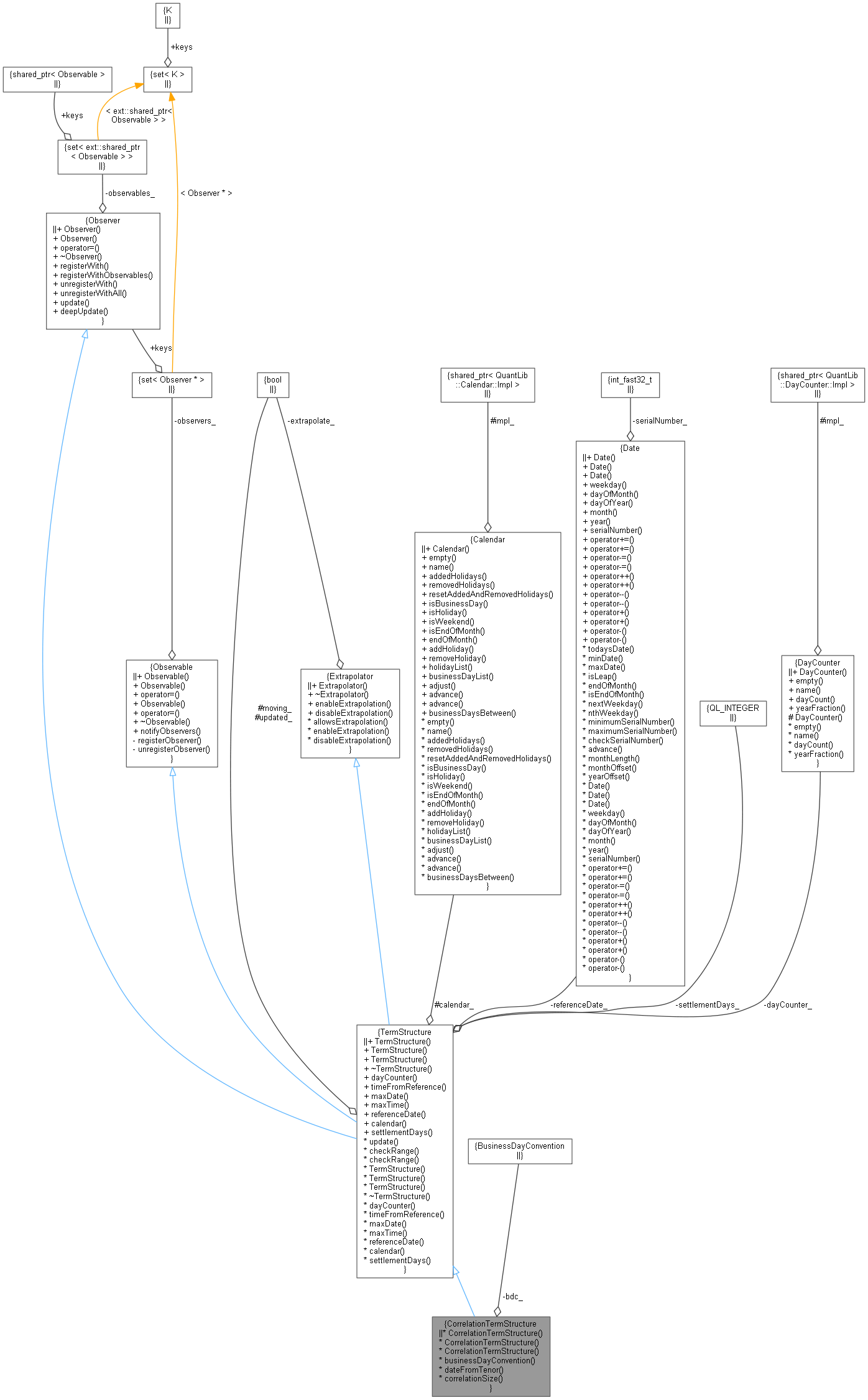

Inheritance diagram for CorrelationTermStructure: Collaboration diagram for CorrelationTermStructure:

Collaboration diagram for CorrelationTermStructure:

Constructors | |

See the TermStructure documentation for issues regarding constructors. | |

| BusinessDayConvention | bdc_ |

| CorrelationTermStructure (const Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| default constructor More... | |

| CorrelationTermStructure (const Date &referenceDate, const Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| CorrelationTermStructure (Natural settlementDays, const Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| BusinessDayConvention | businessDayConvention () const |

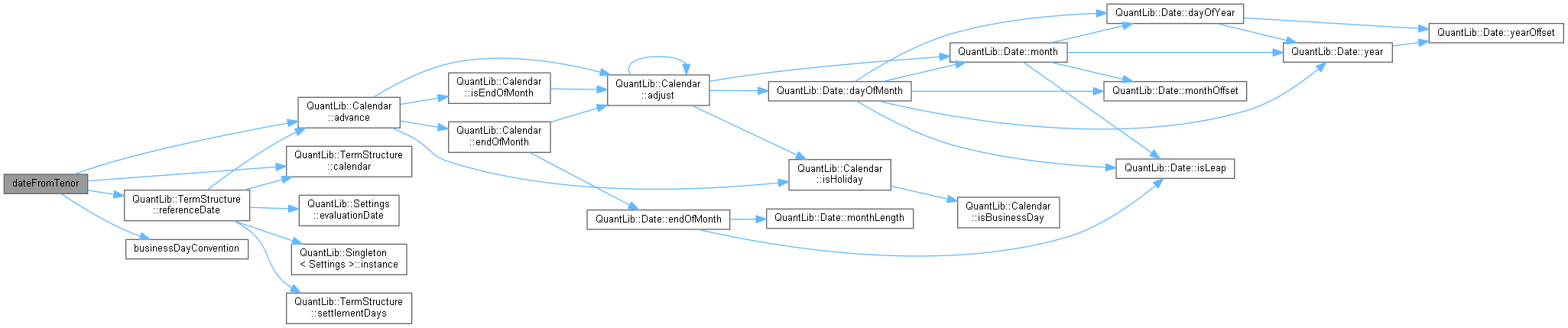

| Date | dateFromTenor (const Period &) const |

| period/date conversion More... | |

| virtual Size | correlationSize () const =0 |

| The size of the squared correlation. More... | |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Public Member Functions inherited from TermStructure | |

| TermStructure (DayCounter dc=DayCounter()) | |

| default constructor More... | |

| TermStructure (const Date &referenceDate, Calendar calendar=Calendar(), DayCounter dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| TermStructure (Natural settlementDays, Calendar, DayCounter dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| ~TermStructure () override=default | |

| virtual DayCounter | dayCounter () const |

| the day counter used for date/time conversion More... | |

| Time | timeFromReference (const Date &date) const |

| date/time conversion More... | |

| virtual Date | maxDate () const =0 |

| the latest date for which the curve can return values More... | |

| virtual Time | maxTime () const |

| the latest time for which the curve can return values More... | |

| virtual const Date & | referenceDate () const |

| the date at which discount = 1.0 and/or variance = 0.0 More... | |

| virtual Calendar | calendar () const |

| the calendar used for reference and/or option date calculation More... | |

| virtual Natural | settlementDays () const |

| the settlementDays used for reference date calculation More... | |

| void | update () override |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Extrapolator | |

| Extrapolator ()=default | |

| virtual | ~Extrapolator ()=default |

| void | enableExtrapolation (bool b=true) |

| enable extrapolation in subsequent calls More... | |

| void | disableExtrapolation (bool b=true) |

| disable extrapolation in subsequent calls More... | |

| bool | allowsExtrapolation () const |

| tells whether extrapolation is enabled More... | |

| Protected Member Functions inherited from TermStructure | |

| void | checkRange (const Date &d, bool extrapolate) const |

| date-range check More... | |

| void | checkRange (Time t, bool extrapolate) const |

| time-range check More... | |

| Protected Attributes inherited from TermStructure | |

| bool | moving_ = false |

| bool | updated_ = true |

| Calendar | calendar_ |

Detailed Description

Abstract interface, derived correlations TS might have elements with arbitrary dimensions.

- In principle there might be several extrapolation dimensions, at this level we do not know how many or the nature of those dimensions (time, strike...) Equally we ignore at this level if the correlation is a number, matrix. Rather than including an arbitrary size matrix this data structure is deferred in the hierarchy to enable potential optimizations on the data nature.

Definition at line 40 of file correlationstructure.hpp.

Constructor & Destructor Documentation

◆ CorrelationTermStructure() [1/3]

| CorrelationTermStructure | ( | const Calendar & | cal, |

| BusinessDayConvention | bdc, | ||

| const DayCounter & | dc = DayCounter() |

||

| ) |

default constructor

- Warning:

- term structures initialized by means of this constructor must manage their own reference date by overriding the referenceDate() method.

Definition at line 24 of file correlationstructure.cpp.

◆ CorrelationTermStructure() [2/3]

| CorrelationTermStructure | ( | const Date & | referenceDate, |

| const Calendar & | cal, | ||

| BusinessDayConvention | bdc, | ||

| const DayCounter & | dc = DayCounter() |

||

| ) |

initialize with a fixed reference date

◆ CorrelationTermStructure() [3/3]

| CorrelationTermStructure | ( | Natural | settlementDays, |

| const Calendar & | cal, | ||

| BusinessDayConvention | bdc, | ||

| const DayCounter & | dc = DayCounter() |

||

| ) |

calculate the reference date based on the global evaluation date

Definition at line 32 of file correlationstructure.cpp.

Member Function Documentation

◆ businessDayConvention()

| BusinessDayConvention businessDayConvention | ( | ) | const |

◆ dateFromTenor()

period/date conversion

Definition at line 82 of file correlationstructure.hpp.

Here is the call graph for this function:

◆ correlationSize()

|

pure virtual |

The size of the squared correlation.

Implemented in BaseCorrelationTermStructure< Interpolator2D_T >.

Member Data Documentation

◆ bdc_

|

private |

Definition at line 72 of file correlationstructure.hpp.