#include <fdmbackwardsolver.hpp>

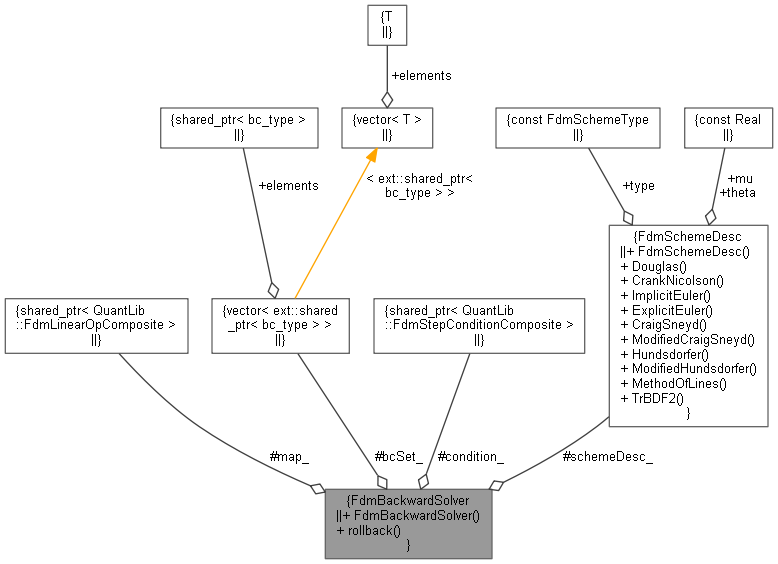

Collaboration diagram for FdmBackwardSolver:

Collaboration diagram for FdmBackwardSolver:

Public Types | |

| typedef FdmLinearOp::array_type | array_type |

Public Member Functions | |

| FdmBackwardSolver (ext::shared_ptr< FdmLinearOpComposite > map, FdmBoundaryConditionSet bcSet, const ext::shared_ptr< FdmStepConditionComposite > &condition, const FdmSchemeDesc &schemeDesc) | |

| void | rollback (array_type &a, Time from, Time to, Size steps, Size dampingSteps) |

Protected Attributes | |

| const ext::shared_ptr< FdmLinearOpComposite > | map_ |

| const FdmBoundaryConditionSet | bcSet_ |

| const ext::shared_ptr< FdmStepConditionComposite > | condition_ |

| const FdmSchemeDesc | schemeDesc_ |

Detailed Description

Definition at line 61 of file fdmbackwardsolver.hpp.

Member Typedef Documentation

◆ array_type

| typedef FdmLinearOp::array_type array_type |

Definition at line 63 of file fdmbackwardsolver.hpp.

Constructor & Destructor Documentation

◆ FdmBackwardSolver()

| FdmBackwardSolver | ( | ext::shared_ptr< FdmLinearOpComposite > | map, |

| FdmBoundaryConditionSet | bcSet, | ||

| const ext::shared_ptr< FdmStepConditionComposite > & | condition, | ||

| const FdmSchemeDesc & | schemeDesc | ||

| ) |

Definition at line 80 of file fdmbackwardsolver.cpp.

Member Function Documentation

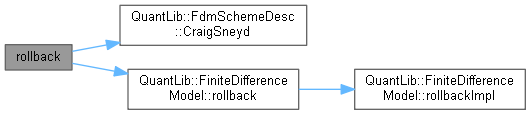

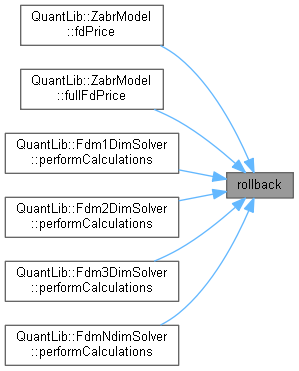

◆ rollback()

| void rollback | ( | FdmBackwardSolver::array_type & | rhs, |

| Time | from, | ||

| Time | to, | ||

| Size | steps, | ||

| Size | dampingSteps | ||

| ) |

Definition at line 92 of file fdmbackwardsolver.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ map_

|

protected |

Definition at line 75 of file fdmbackwardsolver.hpp.

◆ bcSet_

|

protected |

Definition at line 76 of file fdmbackwardsolver.hpp.

◆ condition_

|

protected |

Definition at line 77 of file fdmbackwardsolver.hpp.

◆ schemeDesc_

|

protected |

Definition at line 78 of file fdmbackwardsolver.hpp.