Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Single currency tenor basis swap. More...

#include <qle/instruments/tenorbasisswap.hpp>

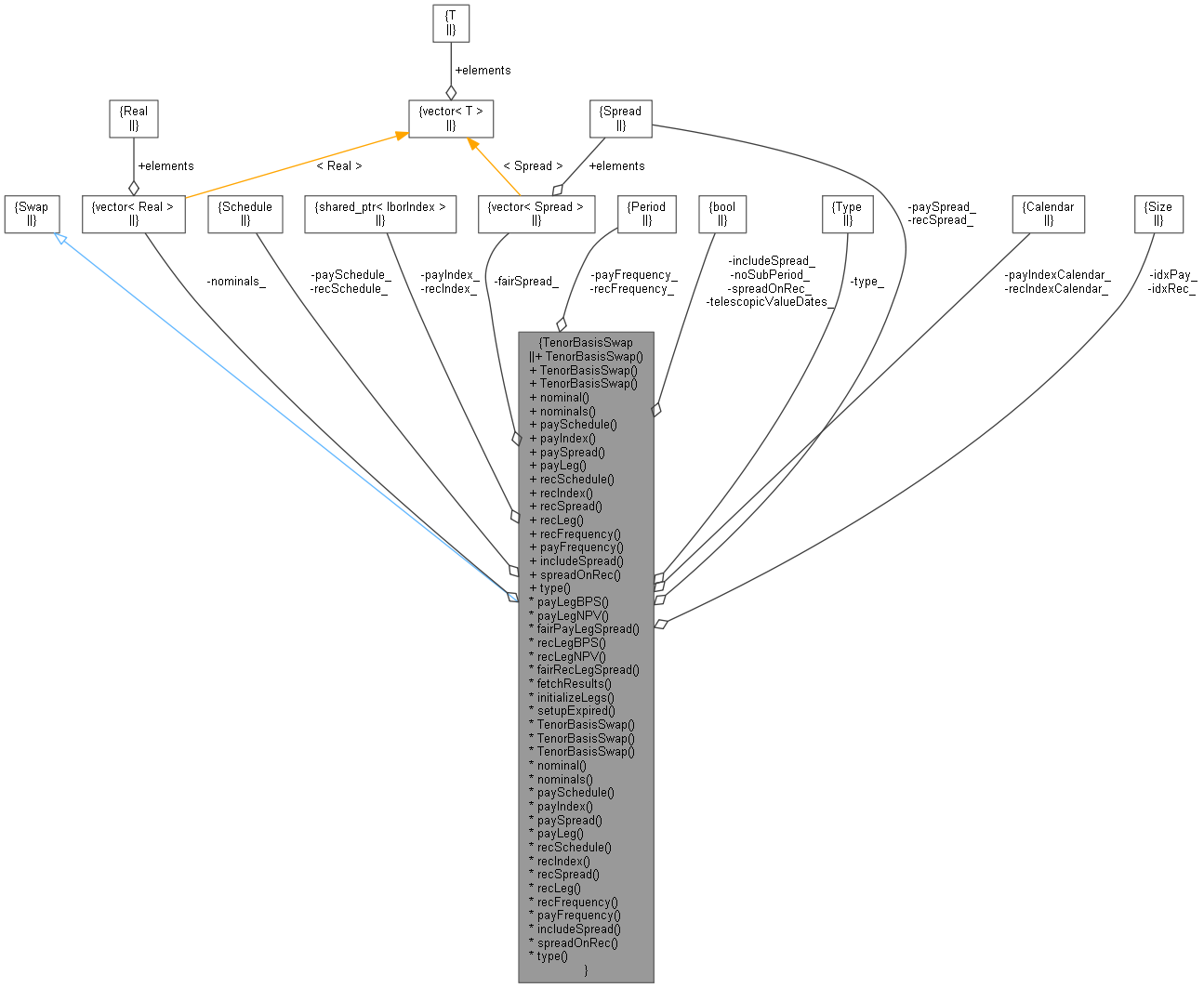

Inheritance diagram for TenorBasisSwap: Collaboration diagram for TenorBasisSwap:

Inheritance diagram for TenorBasisSwap: Collaboration diagram for TenorBasisSwap:Classes | |

| class | engine |

| class | results |

Public Member Functions | |

Constructors | |

| TenorBasisSwap (const Date &effectiveDate, Real nominal, const Period &swapTenor, const QuantLib::ext::shared_ptr< IborIndex > &payIndex, Spread paySpread, const Period &payFrequency, const QuantLib::ext::shared_ptr< IborIndex > &recIndex, Spread recSpread, const Period &recFrequency, DateGeneration::Rule rule=DateGeneration::Backward, bool includeSpread=false, bool spreadOnRec=true, QuantExt::SubPeriodsCoupon1::Type type=QuantExt::SubPeriodsCoupon1::Compounding, const bool telescopicValueDates=false) | |

| Constructor with conventions deduced from the indices. More... | |

| TenorBasisSwap (Real nominal, const Schedule &paySchedule, const QuantLib::ext::shared_ptr< IborIndex > &payIndex, Spread paySpread, const Schedule &recSchedule, const QuantLib::ext::shared_ptr< IborIndex > &recIndex, Spread recSpread, bool includeSpread=false, bool spreadOnRec=true, QuantExt::SubPeriodsCoupon1::Type type=QuantExt::SubPeriodsCoupon1::Compounding, const bool telescopicValueDates=false) | |

| Constructor using Schedules with a full interface. More... | |

| TenorBasisSwap (const std::vector< Real > &nominals, const Schedule &paySchedule, const QuantLib::ext::shared_ptr< IborIndex > &payIndex, Spread paySpread, const Schedule &recSchedule, const QuantLib::ext::shared_ptr< IborIndex > &recIndex, Spread recSpread, bool includeSpread=false, bool spreadOnRec=true, QuantExt::SubPeriodsCoupon1::Type type=QuantExt::SubPeriodsCoupon1::Compounding, const bool telescopicValueDates=false) | |

Inspectors | |

| Real | nominal () const |

| const std::vector< Real > & | nominals () const |

| const Schedule & | paySchedule () const |

| const QuantLib::ext::shared_ptr< IborIndex > & | payIndex () const |

| Spread | paySpread () const |

| const Leg & | payLeg () const |

| const Schedule & | recSchedule () const |

| const QuantLib::ext::shared_ptr< IborIndex > & | recIndex () const |

| Spread | recSpread () const |

| const Leg & | recLeg () const |

| const Period & | recFrequency () const |

| const Period & | payFrequency () const |

| bool | includeSpread () const |

| bool | spreadOnRec () const |

| QuantExt::SubPeriodsCoupon1::Type | type () const |

Results | |

| std::vector< Real > | nominals_ |

| Schedule | paySchedule_ |

| QuantLib::ext::shared_ptr< IborIndex > | payIndex_ |

| Spread | paySpread_ |

| Period | payFrequency_ |

| Schedule | recSchedule_ |

| QuantLib::ext::shared_ptr< IborIndex > | recIndex_ |

| Spread | recSpread_ |

| Period | recFrequency_ |

| bool | includeSpread_ |

| bool | spreadOnRec_ |

| QuantExt::SubPeriodsCoupon1::Type | type_ |

| bool | telescopicValueDates_ |

| bool | noSubPeriod_ |

| std::vector< Spread > | fairSpread_ |

| Calendar | recIndexCalendar_ |

| Calendar | payIndexCalendar_ |

| Size | idxRec_ |

| Size | idxPay_ |

| Real | payLegBPS () const |

| Real | payLegNPV () const |

| Rate | fairPayLegSpread () const |

| Real | recLegBPS () const |

| Real | recLegNPV () const |

| Spread | fairRecLegSpread () const |

| void | fetchResults (const PricingEngine::results *) const override |

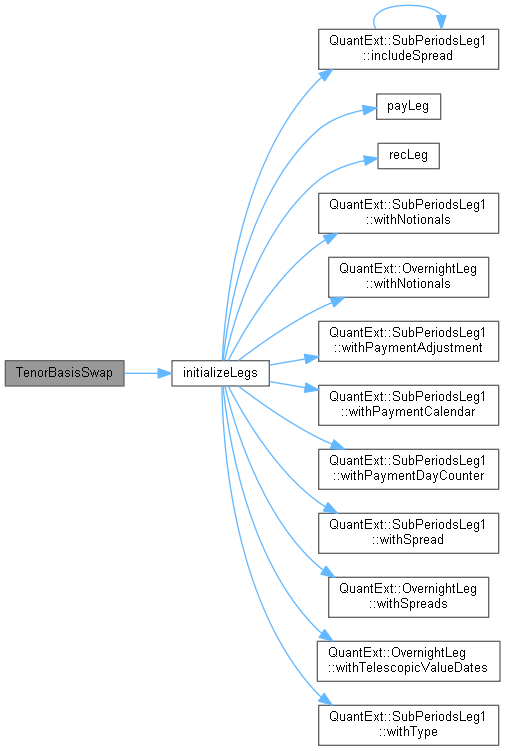

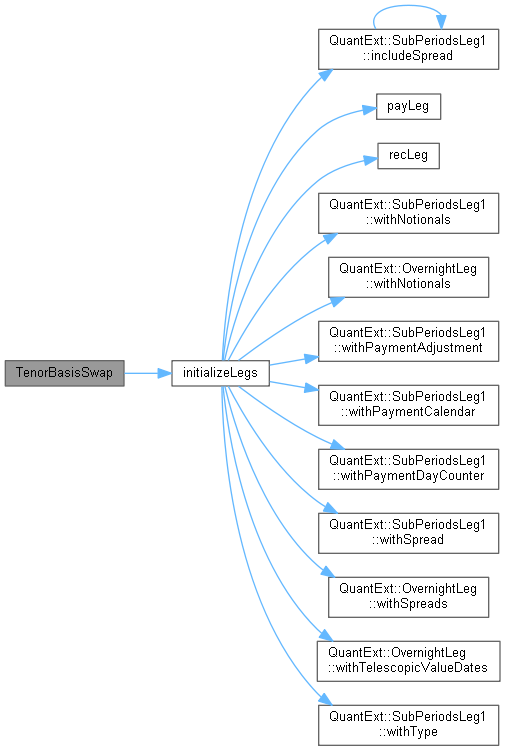

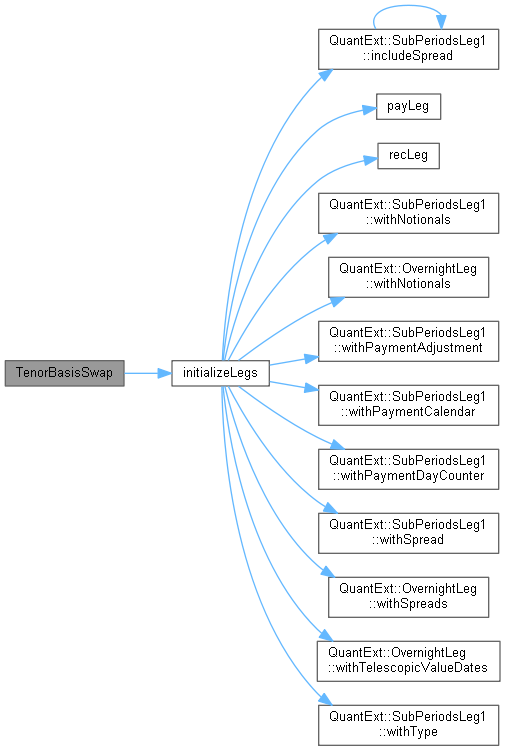

| void | initializeLegs () |

| void | setupExpired () const override |

Single currency tenor basis swap.

Definition at line 38 of file tenorbasisswap.hpp.

| TenorBasisSwap | ( | const Date & | effectiveDate, |

| Real | nominal, | ||

| const Period & | swapTenor, | ||

| const QuantLib::ext::shared_ptr< IborIndex > & | payIndex, | ||

| Spread | paySpread, | ||

| const Period & | payFrequency, | ||

| const QuantLib::ext::shared_ptr< IborIndex > & | recIndex, | ||

| Spread | recSpread, | ||

| const Period & | recFrequency, | ||

| DateGeneration::Rule | rule = DateGeneration::Backward, |

||

| bool | includeSpread = false, |

||

| bool | spreadOnRec = true, |

||

| QuantExt::SubPeriodsCoupon1::Type | type = QuantExt::SubPeriodsCoupon1::Compounding, |

||

| const bool | telescopicValueDates = false |

||

| ) |

Constructor with conventions deduced from the indices.

Definition at line 64 of file tenorbasisswap.cpp.

Here is the call graph for this function:| TenorBasisSwap | ( | Real | nominal, |

| const Schedule & | paySchedule, | ||

| const QuantLib::ext::shared_ptr< IborIndex > & | payIndex, | ||

| Spread | paySpread, | ||

| const Schedule & | recSchedule, | ||

| const QuantLib::ext::shared_ptr< IborIndex > & | recIndex, | ||

| Spread | recSpread, | ||

| bool | includeSpread = false, |

||

| bool | spreadOnRec = true, |

||

| QuantExt::SubPeriodsCoupon1::Type | type = QuantExt::SubPeriodsCoupon1::Compounding, |

||

| const bool | telescopicValueDates = false |

||

| ) |

Constructor using Schedules with a full interface.

Definition at line 108 of file tenorbasisswap.cpp.

Here is the call graph for this function:| TenorBasisSwap | ( | const std::vector< Real > & | nominals, |

| const Schedule & | paySchedule, | ||

| const QuantLib::ext::shared_ptr< IborIndex > & | payIndex, | ||

| Spread | paySpread, | ||

| const Schedule & | recSchedule, | ||

| const QuantLib::ext::shared_ptr< IborIndex > & | recIndex, | ||

| Spread | recSpread, | ||

| bool | includeSpread = false, |

||

| bool | spreadOnRec = true, |

||

| QuantExt::SubPeriodsCoupon1::Type | type = QuantExt::SubPeriodsCoupon1::Compounding, |

||

| const bool | telescopicValueDates = false |

||

| ) |

Definition at line 121 of file tenorbasisswap.cpp.

Here is the call graph for this function:| Real nominal | ( | ) | const |

Definition at line 139 of file tenorbasisswap.hpp.

| const std::vector< Real > & nominals | ( | ) | const |

Definition at line 68 of file tenorbasisswap.hpp.

| const Schedule & paySchedule | ( | ) | const |

Definition at line 143 of file tenorbasisswap.hpp.

| const QuantLib::ext::shared_ptr< IborIndex > & payIndex | ( | ) | const |

Definition at line 145 of file tenorbasisswap.hpp.

| Spread paySpread | ( | ) | const |

Definition at line 147 of file tenorbasisswap.hpp.

| const Leg & payLeg | ( | ) | const |

| const Schedule & recSchedule | ( | ) | const |

Definition at line 151 of file tenorbasisswap.hpp.

| const QuantLib::ext::shared_ptr< IborIndex > & recIndex | ( | ) | const |

Definition at line 153 of file tenorbasisswap.hpp.

| Spread recSpread | ( | ) | const |

Definition at line 155 of file tenorbasisswap.hpp.

| const Leg & recLeg | ( | ) | const |

| const Period & recFrequency | ( | ) | const |

Definition at line 157 of file tenorbasisswap.hpp.

| const Period & payFrequency | ( | ) | const |

Definition at line 159 of file tenorbasisswap.hpp.

| bool includeSpread | ( | ) | const |

Definition at line 161 of file tenorbasisswap.hpp.

| bool spreadOnRec | ( | ) | const |

Definition at line 83 of file tenorbasisswap.hpp.

| QuantExt::SubPeriodsCoupon1::Type type | ( | ) | const |

Definition at line 163 of file tenorbasisswap.hpp.

| Real payLegBPS | ( | ) | const |

Definition at line 237 of file tenorbasisswap.cpp.

| Real payLegNPV | ( | ) | const |

Definition at line 243 of file tenorbasisswap.cpp.

| Rate fairPayLegSpread | ( | ) | const |

Definition at line 249 of file tenorbasisswap.cpp.

| Real recLegBPS | ( | ) | const |

Definition at line 255 of file tenorbasisswap.cpp.

| Real recLegNPV | ( | ) | const |

Definition at line 261 of file tenorbasisswap.cpp.

| Spread fairRecLegSpread | ( | ) | const |

Definition at line 267 of file tenorbasisswap.cpp.

|

override |

Definition at line 278 of file tenorbasisswap.cpp.

|

private |

Definition at line 134 of file tenorbasisswap.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

overrideprivate |

Definition at line 273 of file tenorbasisswap.cpp.

|

private |

Definition at line 102 of file tenorbasisswap.hpp.

|

private |

Definition at line 104 of file tenorbasisswap.hpp.

|

private |

Definition at line 105 of file tenorbasisswap.hpp.

|

private |

Definition at line 106 of file tenorbasisswap.hpp.

|

private |

Definition at line 107 of file tenorbasisswap.hpp.

|

private |

Definition at line 109 of file tenorbasisswap.hpp.

|

private |

Definition at line 110 of file tenorbasisswap.hpp.

|

private |

Definition at line 111 of file tenorbasisswap.hpp.

|

private |

Definition at line 112 of file tenorbasisswap.hpp.

|

private |

Definition at line 114 of file tenorbasisswap.hpp.

|

private |

Definition at line 115 of file tenorbasisswap.hpp.

|

private |

Definition at line 116 of file tenorbasisswap.hpp.

|

private |

Definition at line 117 of file tenorbasisswap.hpp.

|

private |

Definition at line 119 of file tenorbasisswap.hpp.

|

mutableprivate |

Definition at line 121 of file tenorbasisswap.hpp.

|

private |

Definition at line 123 of file tenorbasisswap.hpp.

|

private |

Definition at line 123 of file tenorbasisswap.hpp.

|

private |

Definition at line 124 of file tenorbasisswap.hpp.

|

private |

Definition at line 124 of file tenorbasisswap.hpp.