Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <qle/termstructures/spreadedswaptionvolatility.hpp>

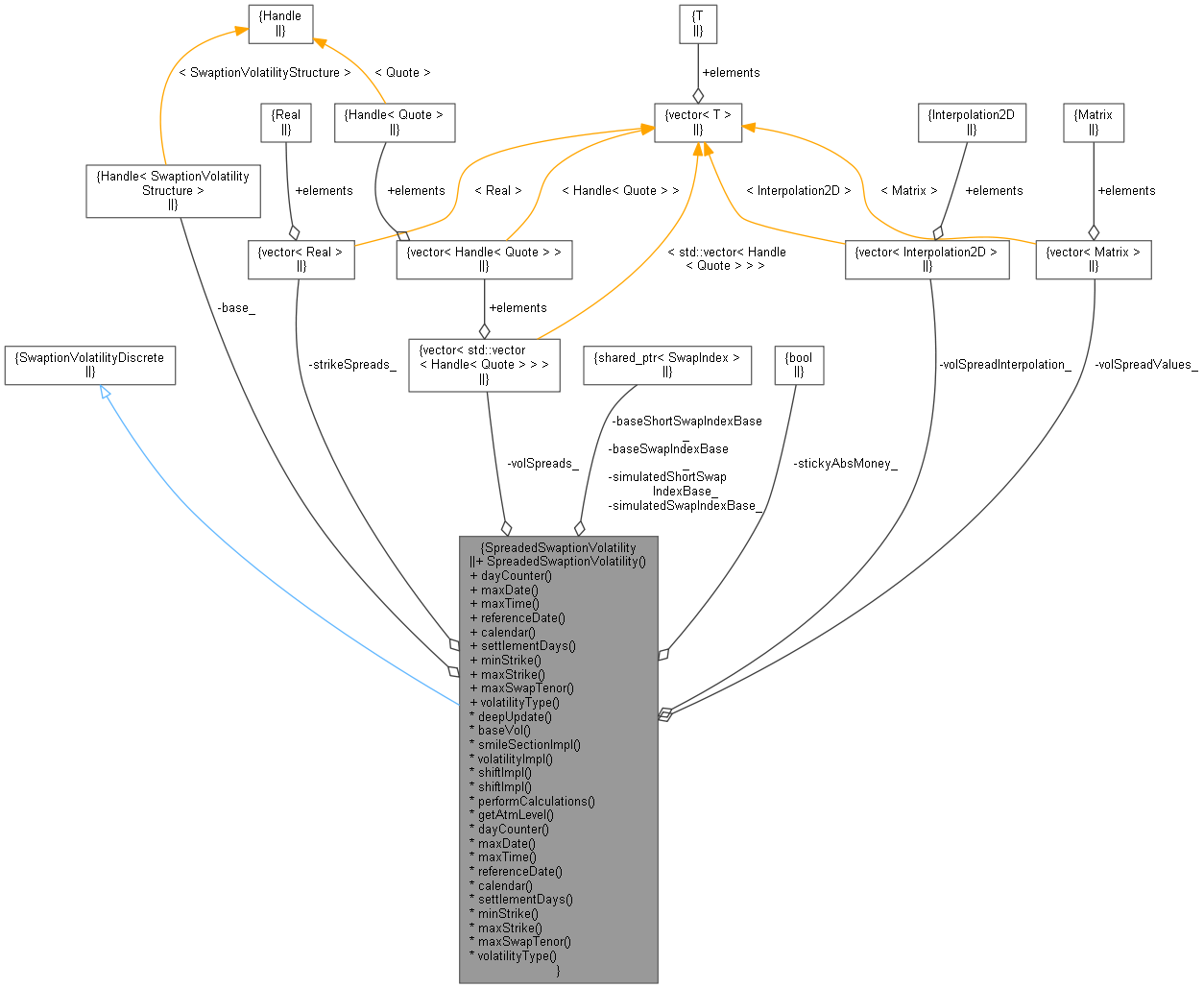

Inheritance diagram for SpreadedSwaptionVolatility: Collaboration diagram for SpreadedSwaptionVolatility:

Inheritance diagram for SpreadedSwaptionVolatility: Collaboration diagram for SpreadedSwaptionVolatility:Public Member Functions | |

| SpreadedSwaptionVolatility (const Handle< SwaptionVolatilityStructure > &base, const std::vector< Period > &optionTenors, const std::vector< Period > &swapTenors, const std::vector< Real > &strikeSpreads, const std::vector< std::vector< Handle< Quote > > > &volSpreads, const QuantLib::ext::shared_ptr< SwapIndex > &baseSwapIndexBase=nullptr, const QuantLib::ext::shared_ptr< SwapIndex > &baseShortSwapIndexBase=nullptr, const QuantLib::ext::shared_ptr< SwapIndex > &simulatedSwapIndexBase=nullptr, const QuantLib::ext::shared_ptr< SwapIndex > &simulatedShortSwapIndexBase=nullptr, const bool stickyAbsMoney=false) | |

TermStructure interface | |

| DayCounter | dayCounter () const override |

| Date | maxDate () const override |

| Time | maxTime () const override |

| const Date & | referenceDate () const override |

| Calendar | calendar () const override |

| Natural | settlementDays () const override |

VolatilityTermStructure interface | |

| Rate | minStrike () const override |

| Rate | maxStrike () const override |

SwaptionVolatilityStructure interface | |

| const Period & | maxSwapTenor () const override |

| VolatilityType | volatilityType () const override |

Observer interface | |

| Handle< SwaptionVolatilityStructure > | base_ |

| std::vector< Real > | strikeSpreads_ |

| std::vector< std::vector< Handle< Quote > > > | volSpreads_ |

| QuantLib::ext::shared_ptr< SwapIndex > | baseSwapIndexBase_ |

| QuantLib::ext::shared_ptr< SwapIndex > | baseShortSwapIndexBase_ |

| QuantLib::ext::shared_ptr< SwapIndex > | simulatedSwapIndexBase_ |

| QuantLib::ext::shared_ptr< SwapIndex > | simulatedShortSwapIndexBase_ |

| bool | stickyAbsMoney_ |

| std::vector< Matrix > | volSpreadValues_ |

| std::vector< Interpolation2D > | volSpreadInterpolation_ |

| void | deepUpdate () override |

| const Handle< SwaptionVolatilityStructure > & | baseVol () |

| QuantLib::ext::shared_ptr< SmileSection > | smileSectionImpl (Time optionTime, Time swapLength) const override |

| Volatility | volatilityImpl (Time optionTime, Time swapLength, Rate strike) const override |

| Real | shiftImpl (const Date &optionDate, const Period &swapTenor) const override |

| Real | shiftImpl (Time optionTime, Time swapLength) const override |

| void | performCalculations () const override |

| Real | getAtmLevel (const Real optionTime, const Real swapLength, const QuantLib::ext::shared_ptr< SwapIndex > swapIndexBase, const QuantLib::ext::shared_ptr< SwapIndex > shortSwapIndexBase) const |

Definition at line 37 of file spreadedswaptionvolatility.hpp.

| SpreadedSwaptionVolatility | ( | const Handle< SwaptionVolatilityStructure > & | base, |

| const std::vector< Period > & | optionTenors, | ||

| const std::vector< Period > & | swapTenors, | ||

| const std::vector< Real > & | strikeSpreads, | ||

| const std::vector< std::vector< Handle< Quote > > > & | volSpreads, | ||

| const QuantLib::ext::shared_ptr< SwapIndex > & | baseSwapIndexBase = nullptr, |

||

| const QuantLib::ext::shared_ptr< SwapIndex > & | baseShortSwapIndexBase = nullptr, |

||

| const QuantLib::ext::shared_ptr< SwapIndex > & | simulatedSwapIndexBase = nullptr, |

||

| const QuantLib::ext::shared_ptr< SwapIndex > & | simulatedShortSwapIndexBase = nullptr, |

||

| const bool | stickyAbsMoney = false |

||

| ) |

Definition at line 30 of file spreadedswaptionvolatility.cpp.

|

override |

Definition at line 78 of file spreadedswaptionvolatility.cpp.

|

override |

Definition at line 79 of file spreadedswaptionvolatility.cpp.

|

override |

Definition at line 80 of file spreadedswaptionvolatility.cpp.

|

override |

Definition at line 81 of file spreadedswaptionvolatility.cpp.

|

override |

Definition at line 82 of file spreadedswaptionvolatility.cpp.

|

override |

Definition at line 83 of file spreadedswaptionvolatility.cpp.

|

override |

Definition at line 84 of file spreadedswaptionvolatility.cpp.

|

override |

Definition at line 85 of file spreadedswaptionvolatility.cpp.

|

override |

Definition at line 86 of file spreadedswaptionvolatility.cpp.

|

override |

Definition at line 87 of file spreadedswaptionvolatility.cpp.

|

override |

Definition at line 88 of file spreadedswaptionvolatility.cpp.

| const Handle< SwaptionVolatilityStructure > & baseVol | ( | ) |

Definition at line 92 of file spreadedswaptionvolatility.cpp.

|

overrideprivate |

Definition at line 110 of file spreadedswaptionvolatility.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

overrideprivate |

Definition at line 137 of file spreadedswaptionvolatility.cpp.

Here is the call graph for this function:

|

overrideprivate |

Definition at line 160 of file spreadedswaptionvolatility.cpp.

|

overrideprivate |

Definition at line 164 of file spreadedswaptionvolatility.cpp.

|

overrideprivate |

Definition at line 168 of file spreadedswaptionvolatility.cpp.

|

private |

Definition at line 94 of file spreadedswaptionvolatility.cpp.

Here is the caller graph for this function:

|

private |

Definition at line 87 of file spreadedswaptionvolatility.hpp.

|

private |

Definition at line 88 of file spreadedswaptionvolatility.hpp.

|

private |

Definition at line 89 of file spreadedswaptionvolatility.hpp.

|

private |

Definition at line 90 of file spreadedswaptionvolatility.hpp.

|

private |

Definition at line 90 of file spreadedswaptionvolatility.hpp.

|

private |

Definition at line 91 of file spreadedswaptionvolatility.hpp.

|

private |

Definition at line 91 of file spreadedswaptionvolatility.hpp.

|

private |

Definition at line 92 of file spreadedswaptionvolatility.hpp.

|

mutableprivate |

Definition at line 93 of file spreadedswaptionvolatility.hpp.

|

mutableprivate |

Definition at line 94 of file spreadedswaptionvolatility.hpp.