Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <qle/instruments/riskparticipationagreement.hpp>

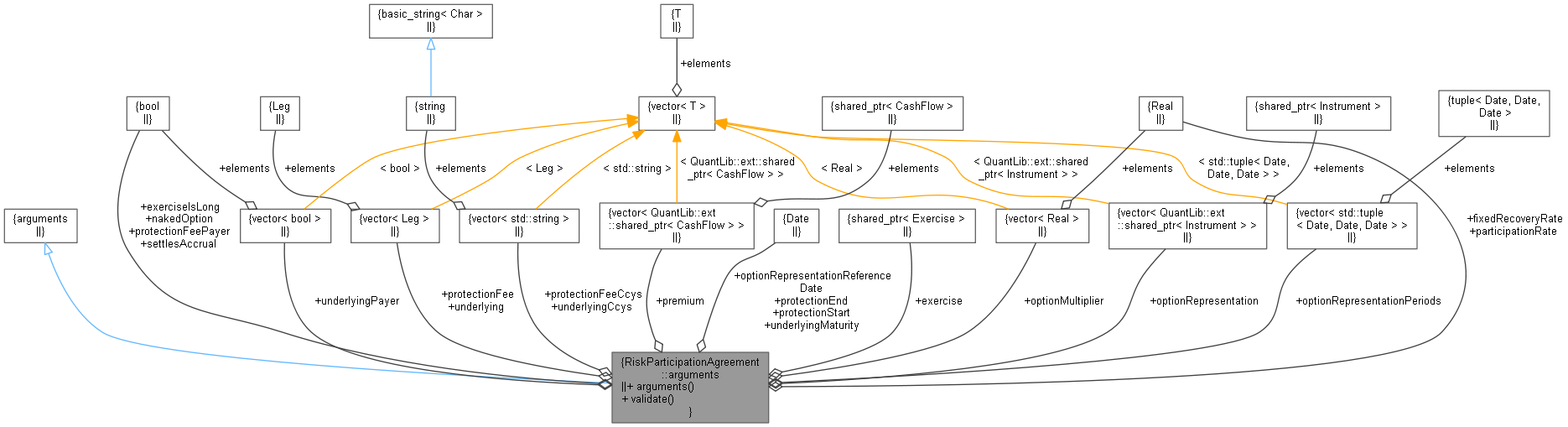

Inheritance diagram for RiskParticipationAgreement::arguments: Collaboration diagram for RiskParticipationAgreement::arguments:

Inheritance diagram for RiskParticipationAgreement::arguments: Collaboration diagram for RiskParticipationAgreement::arguments:Public Member Functions | |

| arguments () | |

| void | validate () const override |

Public Attributes | |

| std::vector< Leg > | underlying |

| std::vector< bool > | underlyingPayer |

| std::vector< std::string > | underlyingCcys |

| std::vector< Leg > | protectionFee |

| bool | protectionFeePayer |

| std::vector< std::string > | protectionFeeCcys |

| Real | participationRate |

| Date | protectionStart |

| Date | protectionEnd |

| Date | underlyingMaturity |

| bool | settlesAccrual |

| Real | fixedRecoveryRate |

| QuantLib::ext::shared_ptr< Exercise > | exercise |

| bool | exerciseIsLong |

| std::vector< QuantLib::ext::shared_ptr< CashFlow > > | premium |

| bool | nakedOption |

| std::vector< QuantLib::ext::shared_ptr< Instrument > > | optionRepresentation |

| std::vector< Real > | optionMultiplier |

| std::vector< std::tuple< Date, Date, Date > > | optionRepresentationPeriods |

| Date | optionRepresentationReferenceDate |

Definition at line 99 of file riskparticipationagreement.hpp.

| arguments | ( | ) |

Definition at line 101 of file riskparticipationagreement.hpp.

|

override |

Definition at line 102 of file riskparticipationagreement.hpp.

| std::vector<Leg> underlying |

Definition at line 103 of file riskparticipationagreement.hpp.

| std::vector<bool> underlyingPayer |

Definition at line 104 of file riskparticipationagreement.hpp.

| std::vector<std::string> underlyingCcys |

Definition at line 105 of file riskparticipationagreement.hpp.

| std::vector<Leg> protectionFee |

Definition at line 106 of file riskparticipationagreement.hpp.

| bool protectionFeePayer |

Definition at line 107 of file riskparticipationagreement.hpp.

| std::vector<std::string> protectionFeeCcys |

Definition at line 108 of file riskparticipationagreement.hpp.

| Real participationRate |

Definition at line 109 of file riskparticipationagreement.hpp.

| Date protectionStart |

Definition at line 110 of file riskparticipationagreement.hpp.

| Date protectionEnd |

Definition at line 110 of file riskparticipationagreement.hpp.

| Date underlyingMaturity |

Definition at line 110 of file riskparticipationagreement.hpp.

| bool settlesAccrual |

Definition at line 111 of file riskparticipationagreement.hpp.

| Real fixedRecoveryRate |

Definition at line 112 of file riskparticipationagreement.hpp.

| QuantLib::ext::shared_ptr<Exercise> exercise |

Definition at line 113 of file riskparticipationagreement.hpp.

| bool exerciseIsLong |

Definition at line 114 of file riskparticipationagreement.hpp.

| std::vector<QuantLib::ext::shared_ptr<CashFlow> > premium |

Definition at line 115 of file riskparticipationagreement.hpp.

| bool nakedOption |

Definition at line 116 of file riskparticipationagreement.hpp.

| std::vector<QuantLib::ext::shared_ptr<Instrument> > optionRepresentation |

Definition at line 117 of file riskparticipationagreement.hpp.

| std::vector<Real> optionMultiplier |

Definition at line 118 of file riskparticipationagreement.hpp.

| std::vector<std::tuple<Date, Date, Date> > optionRepresentationPeriods |

Definition at line 119 of file riskparticipationagreement.hpp.

| Date optionRepresentationReferenceDate |

Definition at line 120 of file riskparticipationagreement.hpp.