Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <qle/termstructures/proxyoptionletvolatility.hpp>

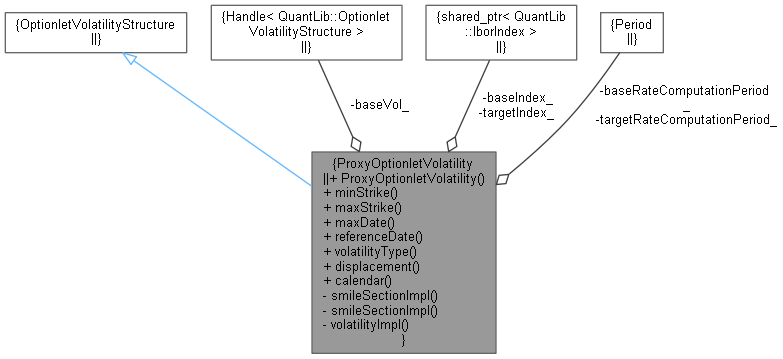

Inheritance diagram for ProxyOptionletVolatility: Collaboration diagram for ProxyOptionletVolatility:

Inheritance diagram for ProxyOptionletVolatility: Collaboration diagram for ProxyOptionletVolatility:Public Member Functions | |

| ProxyOptionletVolatility (const QuantLib::Handle< OptionletVolatilityStructure > &baseVol, const QuantLib::ext::shared_ptr< QuantLib::IborIndex > &baseIndex, const QuantLib::ext::shared_ptr< QuantLib::IborIndex > &targetIndex, const QuantLib::Period &baseRateComputationPeriod=0 *QuantLib::Days, const QuantLib::Period &targetRateComputationPeriod=0 *QuantLib::Days) | |

| QuantLib::Rate | minStrike () const override |

| QuantLib::Rate | maxStrike () const override |

| QuantLib::Date | maxDate () const override |

| const QuantLib::Date & | referenceDate () const override |

| VolatilityType | volatilityType () const override |

| Real | displacement () const override |

| Calendar | calendar () const override |

Private Member Functions | |

| QuantLib::ext::shared_ptr< QuantLib::SmileSection > | smileSectionImpl (const QuantLib::Date &optionDate) const override |

| QuantLib::ext::shared_ptr< QuantLib::SmileSection > | smileSectionImpl (QuantLib::Time optionTime) const override |

| QuantLib::Volatility | volatilityImpl (QuantLib::Time optionTime, QuantLib::Rate strike) const override |

Private Attributes | |

| QuantLib::Handle< QuantLib::OptionletVolatilityStructure > | baseVol_ |

| QuantLib::ext::shared_ptr< QuantLib::IborIndex > | baseIndex_ |

| QuantLib::ext::shared_ptr< QuantLib::IborIndex > | targetIndex_ |

| QuantLib::Period | baseRateComputationPeriod_ |

| QuantLib::Period | targetRateComputationPeriod_ |

Definition at line 30 of file proxyoptionletvolatility.hpp.

| ProxyOptionletVolatility | ( | const QuantLib::Handle< OptionletVolatilityStructure > & | baseVol, |

| const QuantLib::ext::shared_ptr< QuantLib::IborIndex > & | baseIndex, | ||

| const QuantLib::ext::shared_ptr< QuantLib::IborIndex > & | targetIndex, | ||

| const QuantLib::Period & | baseRateComputationPeriod = 0 * QuantLib::Days, |

||

| const QuantLib::Period & | targetRateComputationPeriod = 0 * QuantLib::Days |

||

| ) |

Definition at line 46 of file proxyoptionletvolatility.cpp.

|

override |

Definition at line 38 of file proxyoptionletvolatility.hpp.

|

override |

Definition at line 39 of file proxyoptionletvolatility.hpp.

|

override |

Definition at line 40 of file proxyoptionletvolatility.hpp.

|

override |

Definition at line 41 of file proxyoptionletvolatility.hpp.

Here is the caller graph for this function:

|

override |

Definition at line 42 of file proxyoptionletvolatility.hpp.

|

override |

Definition at line 43 of file proxyoptionletvolatility.hpp.

|

override |

Definition at line 44 of file proxyoptionletvolatility.hpp.

|

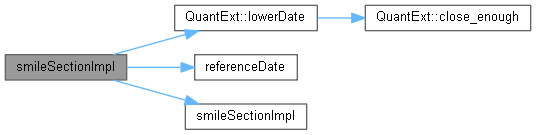

overrideprivate |

Here is the caller graph for this function:

|

overrideprivate |

Definition at line 69 of file proxyoptionletvolatility.cpp.

Here is the call graph for this function:

|

overrideprivate |

Definition at line 108 of file proxyoptionletvolatility.cpp.

|

private |

Definition at line 51 of file proxyoptionletvolatility.hpp.

|

private |

Definition at line 52 of file proxyoptionletvolatility.hpp.

|

private |

Definition at line 53 of file proxyoptionletvolatility.hpp.

|

private |

Definition at line 54 of file proxyoptionletvolatility.hpp.

|

private |

Definition at line 55 of file proxyoptionletvolatility.hpp.