Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

helper class building a sequence of overnight coupons More...

#include <qle/cashflows/overnightindexedcoupon.hpp>

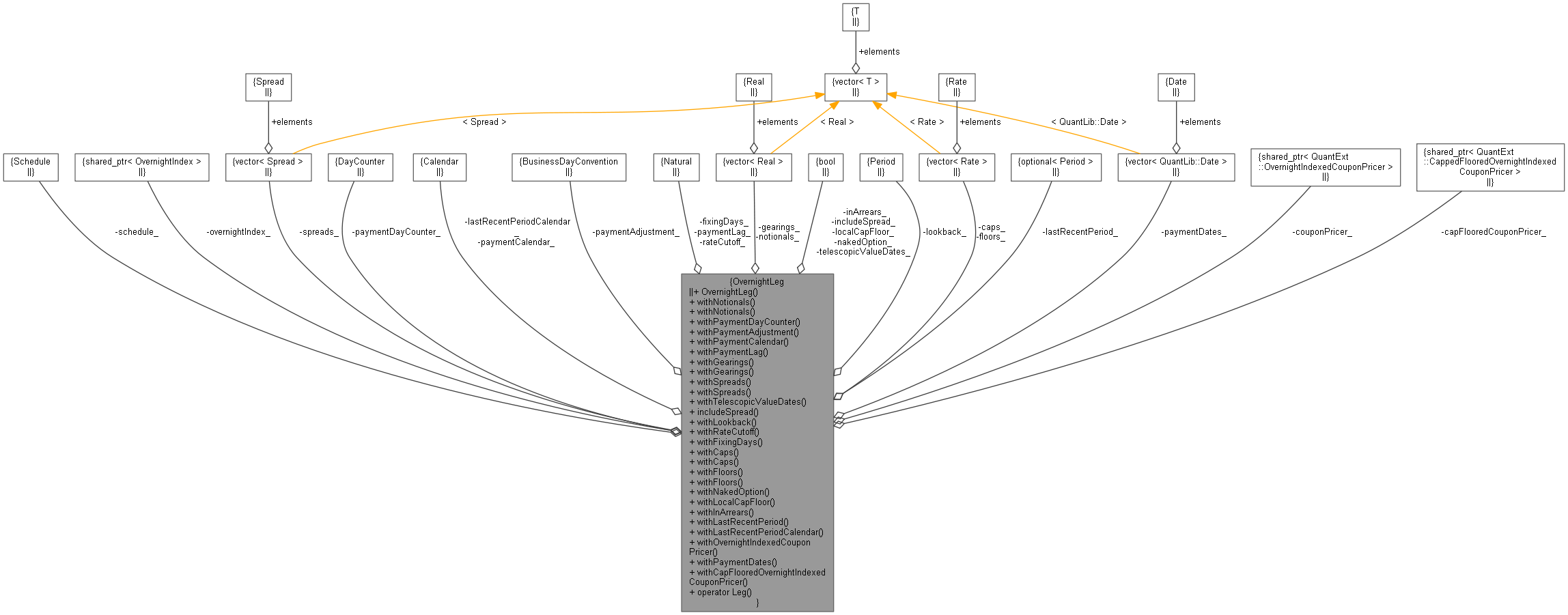

Collaboration diagram for OvernightLeg:

Collaboration diagram for OvernightLeg:Public Member Functions | |

| OvernightLeg (const Schedule &schedule, const ext::shared_ptr< OvernightIndex > &overnightIndex) | |

| OvernightLeg & | withNotionals (Real notional) |

| OvernightLeg & | withNotionals (const std::vector< Real > ¬ionals) |

| OvernightLeg & | withPaymentDayCounter (const DayCounter &) |

| OvernightLeg & | withPaymentAdjustment (BusinessDayConvention) |

| OvernightLeg & | withPaymentCalendar (const Calendar &) |

| OvernightLeg & | withPaymentLag (Natural lag) |

| OvernightLeg & | withGearings (Real gearing) |

| OvernightLeg & | withGearings (const std::vector< Real > &gearings) |

| OvernightLeg & | withSpreads (Spread spread) |

| OvernightLeg & | withSpreads (const std::vector< Spread > &spreads) |

| OvernightLeg & | withTelescopicValueDates (bool telescopicValueDates) |

| OvernightLeg & | includeSpread (bool includeSpread) |

| OvernightLeg & | withLookback (const Period &lookback) |

| OvernightLeg & | withRateCutoff (const Natural rateCutoff) |

| OvernightLeg & | withFixingDays (const Natural fixingDays) |

| OvernightLeg & | withCaps (Rate cap) |

| OvernightLeg & | withCaps (const std::vector< Rate > &caps) |

| OvernightLeg & | withFloors (Rate floor) |

| OvernightLeg & | withFloors (const std::vector< Rate > &floors) |

| OvernightLeg & | withNakedOption (const bool nakedOption) |

| OvernightLeg & | withLocalCapFloor (const bool localCapFloor) |

| OvernightLeg & | withInArrears (const bool inArrears) |

| OvernightLeg & | withLastRecentPeriod (const boost::optional< Period > &lastRecentPeriod) |

| OvernightLeg & | withLastRecentPeriodCalendar (const Calendar &lastRecentPeriodCalendar) |

| OvernightLeg & | withOvernightIndexedCouponPricer (const QuantLib::ext::shared_ptr< OvernightIndexedCouponPricer > &couponPricer) |

| OvernightLeg & | withPaymentDates (const std::vector< Date > &paymentDates) |

| OvernightLeg & | withCapFlooredOvernightIndexedCouponPricer (const QuantLib::ext::shared_ptr< CappedFlooredOvernightIndexedCouponPricer > &couponPricer) |

| operator Leg () const | |

Private Attributes | |

| Schedule | schedule_ |

| ext::shared_ptr< OvernightIndex > | overnightIndex_ |

| std::vector< Real > | notionals_ |

| DayCounter | paymentDayCounter_ |

| Calendar | paymentCalendar_ |

| BusinessDayConvention | paymentAdjustment_ |

| Natural | paymentLag_ |

| std::vector< Real > | gearings_ |

| std::vector< Spread > | spreads_ |

| bool | telescopicValueDates_ |

| bool | includeSpread_ |

| Period | lookback_ |

| Natural | rateCutoff_ |

| Natural | fixingDays_ |

| std::vector< Rate > | caps_ |

| std::vector< Rate > | floors_ |

| bool | nakedOption_ |

| bool | localCapFloor_ |

| bool | inArrears_ |

| boost::optional< Period > | lastRecentPeriod_ |

| Calendar | lastRecentPeriodCalendar_ |

| std::vector< QuantLib::Date > | paymentDates_ |

| QuantLib::ext::shared_ptr< OvernightIndexedCouponPricer > | couponPricer_ |

| QuantLib::ext::shared_ptr< CappedFlooredOvernightIndexedCouponPricer > | capFlooredCouponPricer_ |

helper class building a sequence of overnight coupons

Definition at line 229 of file overnightindexedcoupon.hpp.

| OvernightLeg | ( | const Schedule & | schedule, |

| const ext::shared_ptr< OvernightIndex > & | overnightIndex | ||

| ) |

Definition at line 469 of file overnightindexedcoupon.cpp.

| OvernightLeg & withNotionals | ( | Real | notional | ) |

Definition at line 474 of file overnightindexedcoupon.cpp.

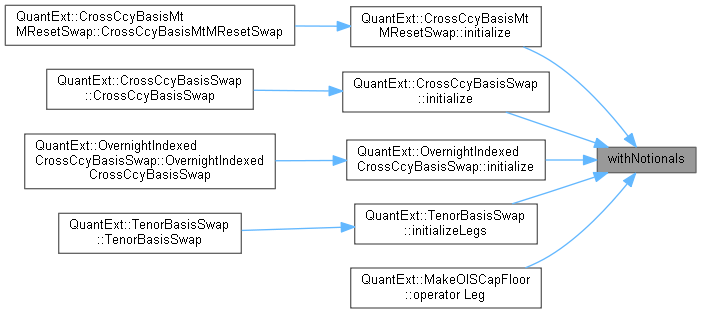

Here is the caller graph for this function:| OvernightLeg & withNotionals | ( | const std::vector< Real > & | notionals | ) |

Definition at line 479 of file overnightindexedcoupon.cpp.

| OvernightLeg & withPaymentDayCounter | ( | const DayCounter & | dc | ) |

Definition at line 484 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:| OvernightLeg & withPaymentAdjustment | ( | BusinessDayConvention | convention | ) |

Definition at line 489 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:| OvernightLeg & withPaymentCalendar | ( | const Calendar & | cal | ) |

Definition at line 494 of file overnightindexedcoupon.cpp.

| OvernightLeg & withPaymentLag | ( | Natural | lag | ) |

Definition at line 499 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:| OvernightLeg & withGearings | ( | Real | gearing | ) |

Definition at line 504 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:| OvernightLeg & withGearings | ( | const std::vector< Real > & | gearings | ) |

Definition at line 509 of file overnightindexedcoupon.cpp.

| OvernightLeg & withSpreads | ( | Spread | spread | ) |

Definition at line 514 of file overnightindexedcoupon.cpp.

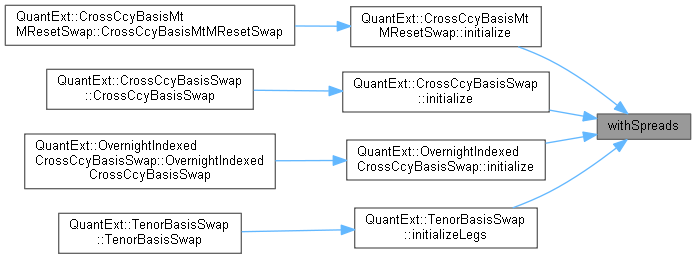

Here is the caller graph for this function:| OvernightLeg & withSpreads | ( | const std::vector< Spread > & | spreads | ) |

Definition at line 519 of file overnightindexedcoupon.cpp.

| OvernightLeg & withTelescopicValueDates | ( | bool | telescopicValueDates | ) |

Definition at line 524 of file overnightindexedcoupon.cpp.

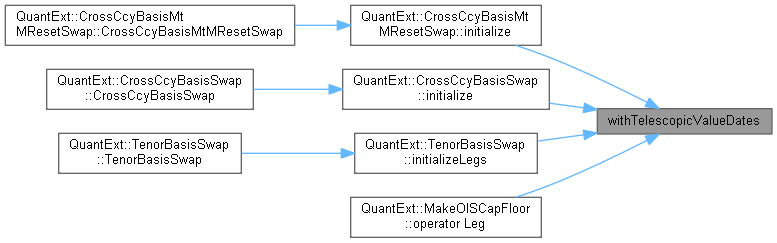

Here is the caller graph for this function:| OvernightLeg & includeSpread | ( | bool | includeSpread | ) |

Definition at line 529 of file overnightindexedcoupon.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| OvernightLeg & withLookback | ( | const Period & | lookback | ) |

Definition at line 534 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:| OvernightLeg & withRateCutoff | ( | const Natural | rateCutoff | ) |

Definition at line 539 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:| OvernightLeg & withFixingDays | ( | const Natural | fixingDays | ) |

Definition at line 544 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:| OvernightLeg & withCaps | ( | Rate | cap | ) |

Definition at line 549 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:| OvernightLeg & withCaps | ( | const std::vector< Rate > & | caps | ) |

Definition at line 554 of file overnightindexedcoupon.cpp.

| OvernightLeg & withFloors | ( | Rate | floor | ) |

Definition at line 559 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:| OvernightLeg & withFloors | ( | const std::vector< Rate > & | floors | ) |

Definition at line 564 of file overnightindexedcoupon.cpp.

| OvernightLeg & withNakedOption | ( | const bool | nakedOption | ) |

Definition at line 569 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:| OvernightLeg & withLocalCapFloor | ( | const bool | localCapFloor | ) |

Definition at line 574 of file overnightindexedcoupon.cpp.

| OvernightLeg & withInArrears | ( | const bool | inArrears | ) |

Definition at line 579 of file overnightindexedcoupon.cpp.

| OvernightLeg & withLastRecentPeriod | ( | const boost::optional< Period > & | lastRecentPeriod | ) |

Definition at line 584 of file overnightindexedcoupon.cpp.

| OvernightLeg & withLastRecentPeriodCalendar | ( | const Calendar & | lastRecentPeriodCalendar | ) |

Definition at line 589 of file overnightindexedcoupon.cpp.

| OvernightLeg & withOvernightIndexedCouponPricer | ( | const QuantLib::ext::shared_ptr< OvernightIndexedCouponPricer > & | couponPricer | ) |

Definition at line 600 of file overnightindexedcoupon.cpp.

| OvernightLeg & withPaymentDates | ( | const std::vector< Date > & | paymentDates | ) |

Definition at line 594 of file overnightindexedcoupon.cpp.

| OvernightLeg & withCapFlooredOvernightIndexedCouponPricer | ( | const QuantLib::ext::shared_ptr< CappedFlooredOvernightIndexedCouponPricer > & | couponPricer | ) |

Definition at line 605 of file overnightindexedcoupon.cpp.

| operator Leg | ( | ) | const |

Definition at line 611 of file overnightindexedcoupon.cpp.

Here is the call graph for this function:

|

private |

Definition at line 263 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 264 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 265 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 266 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 267 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 268 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 269 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 270 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 271 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 272 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 273 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 274 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 275 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 276 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 277 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 277 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 278 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 279 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 280 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 281 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 282 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 283 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 284 of file overnightindexedcoupon.hpp.

|

private |

Definition at line 285 of file overnightindexedcoupon.hpp.