Coupon paying a YoY-inflation type index

More...

#include <qle/cashflows/nonstandardyoyinflationcoupon.hpp>

|

| | NonStandardYoYInflationCoupon (const Date &paymentDate, Real nominal, const Date &startDate, const Date &endDate, Natural fixingDays, const ext::shared_ptr< ZeroInflationIndex > &index, const Period &observationLag, const DayCounter &dayCounter, Real gearing=1.0, Spread spread=0.0, const Date &refPeriodStart=Date(), const Date &refPeriodEnd=Date(), bool addInflationNotional=false, QuantLib::CPI::InterpolationType interpolation=QuantLib::CPI::InterpolationType::Flat) |

| |

|

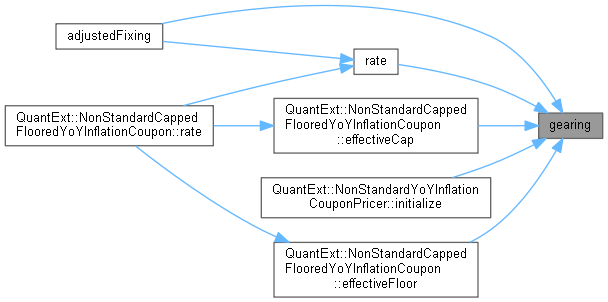

| Real | gearing () const |

| | index gearing, i.e. multiplicative coefficient for the index More...

|

| |

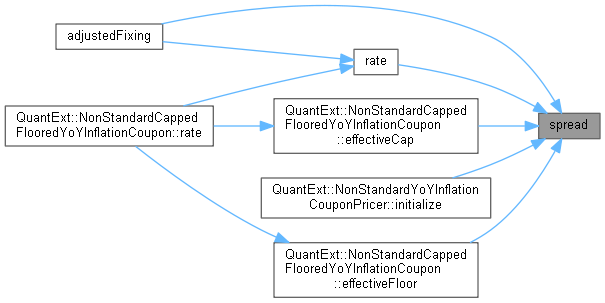

| Spread | spread () const |

| | spread paid over the fixing of the underlying index More...

|

| |

| Rate | adjustedFixing () const |

| |

Coupon paying a YoY-inflation type index

Definition at line 39 of file nonstandardyoyinflationcoupon.hpp.

◆ NonStandardYoYInflationCoupon()

| NonStandardYoYInflationCoupon |

( |

const Date & |

paymentDate, |

|

|

Real |

nominal, |

|

|

const Date & |

startDate, |

|

|

const Date & |

endDate, |

|

|

Natural |

fixingDays, |

|

|

const ext::shared_ptr< ZeroInflationIndex > & |

index, |

|

|

const Period & |

observationLag, |

|

|

const DayCounter & |

dayCounter, |

|

|

Real |

gearing = 1.0, |

|

|

Spread |

spread = 0.0, |

|

|

const Date & |

refPeriodStart = Date(), |

|

|

const Date & |

refPeriodEnd = Date(), |

|

|

bool |

addInflationNotional = false, |

|

|

QuantLib::CPI::InterpolationType |

interpolation = QuantLib::CPI::InterpolationType::Flat |

|

) |

| |

Definition at line 54 of file nonstandardyoyinflationcoupon.cpp.

58 : QuantLib::InflationCoupon(paymentDate, nominal, startDate, endDate, fixingDays, index, observationLag, dayCounter,

59 refPeriodStart, refPeriodEnd),

63}

bool addInflationNotional_

QuantLib::CPI::InterpolationType interpolationType_

void setFixingDates(const Date &denumatorDate, const Date &numeratorDate, const Period &observationLag)

Real gearing() const

index gearing, i.e. multiplicative coefficient for the index

bool addInflationNotional() const

Spread spread() const

spread paid over the fixing of the underlying index

◆ gearing()

◆ spread()

◆ adjustedFixing()

| Rate adjustedFixing |

( |

| ) |

const |

◆ accept()

| void accept |

( |

AcyclicVisitor & |

v | ) |

|

|

overridevirtual |

◆ fixingDateNumerator()

| Date fixingDateNumerator |

( |

| ) |

const |

|

virtual |

◆ fixingDateDenumerator()

| Date fixingDateDenumerator |

( |

| ) |

const |

|

virtual |

◆ cpiIndex()

| ext::shared_ptr< ZeroInflationIndex > cpiIndex |

( |

| ) |

const |

|

virtual |

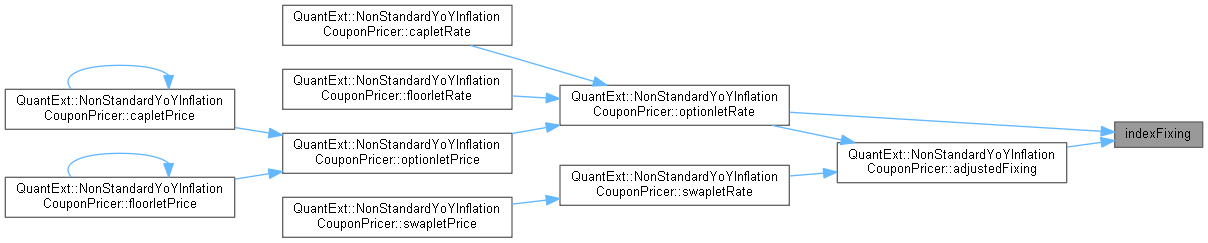

◆ indexFixing()

| Rate indexFixing |

( |

| ) |

const |

|

overridevirtual |

Definition at line 80 of file nonstandardyoyinflationcoupon.cpp.

80 {

81 auto zii = QuantLib::ext::dynamic_pointer_cast<QuantLib::ZeroInflationIndex>(index_);

84 return I_t / I_s - 1.0;

85}

virtual Date fixingDateNumerator() const

virtual Date fixingDateDenumerator() const

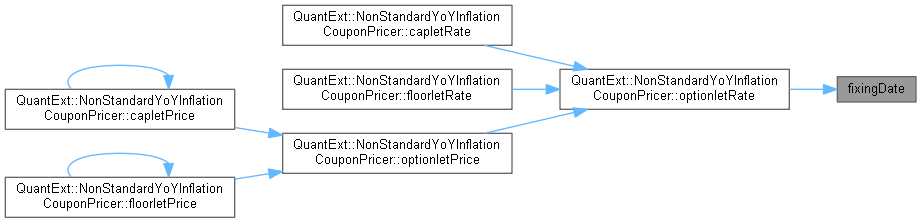

◆ fixingDate()

| Date fixingDate |

( |

| ) |

const |

|

overridevirtual |

◆ rate()

◆ addInflationNotional()

| bool addInflationNotional |

( |

| ) |

const |

◆ isInterpolated()

| bool isInterpolated |

( |

| ) |

const |

◆ interpolationType()

| QuantLib::CPI::InterpolationType interpolationType |

( |

| ) |

const |

◆ checkPricerImpl()

| bool checkPricerImpl |

( |

const ext::shared_ptr< InflationCouponPricer > & |

pricer | ) |

const |

|

overrideprotected |

◆ setFixingDates()

| void setFixingDates |

( |

const Date & |

denumatorDate, |

|

|

const Date & |

numeratorDate, |

|

|

const Period & |

observationLag |

|

) |

| |

|

private |

Definition at line 44 of file nonstandardyoyinflationcoupon.cpp.

45 {

46

48 denumatorDate - observationLag_, -static_cast<Integer>(fixingDays_), Days, ModifiedPreceding);

49

51 numeratorDate - observationLag_, -static_cast<Integer>(fixingDays_), Days, ModifiedPreceding);

52}

◆ fixingDateNumerator_

| Date fixingDateNumerator_ |

|

protected |

◆ fixingDateDenumerator_

| Date fixingDateDenumerator_ |

|

protected |

◆ gearing_

◆ spread_

◆ addInflationNotional_

| bool addInflationNotional_ |

|

protected |

◆ interpolationType_

| QuantLib::CPI::InterpolationType interpolationType_ |

|

protected |

Inheritance diagram for NonStandardYoYInflationCoupon:

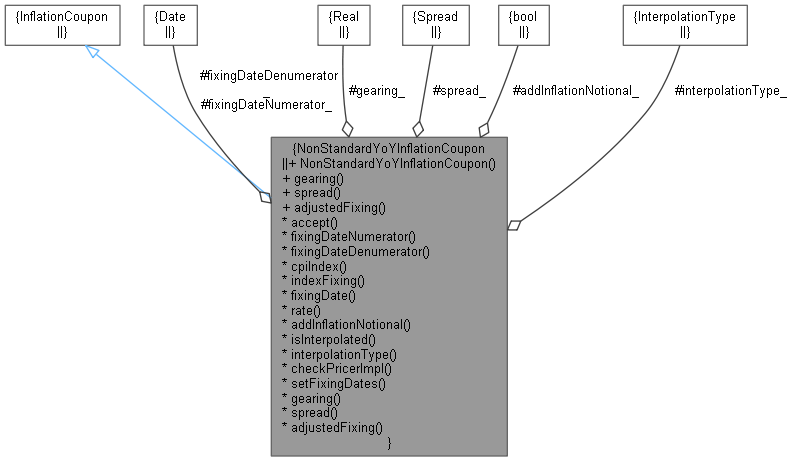

Inheritance diagram for NonStandardYoYInflationCoupon: