Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Interpolated cap floor term volatility curve. More...

#include <qle/termstructures/capfloortermvolcurve.hpp>

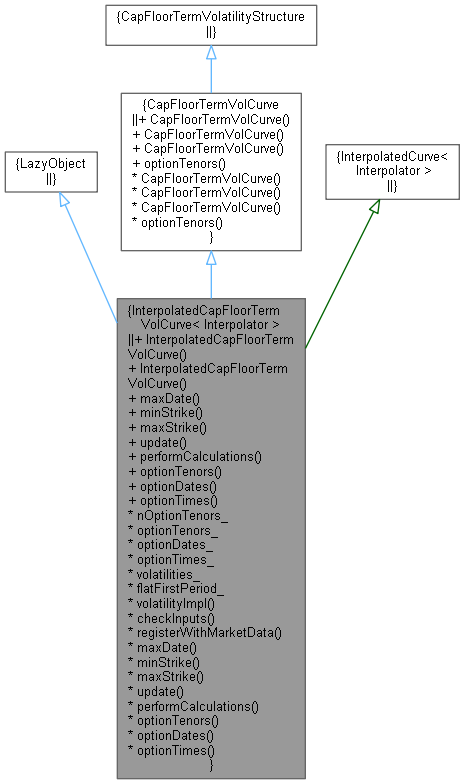

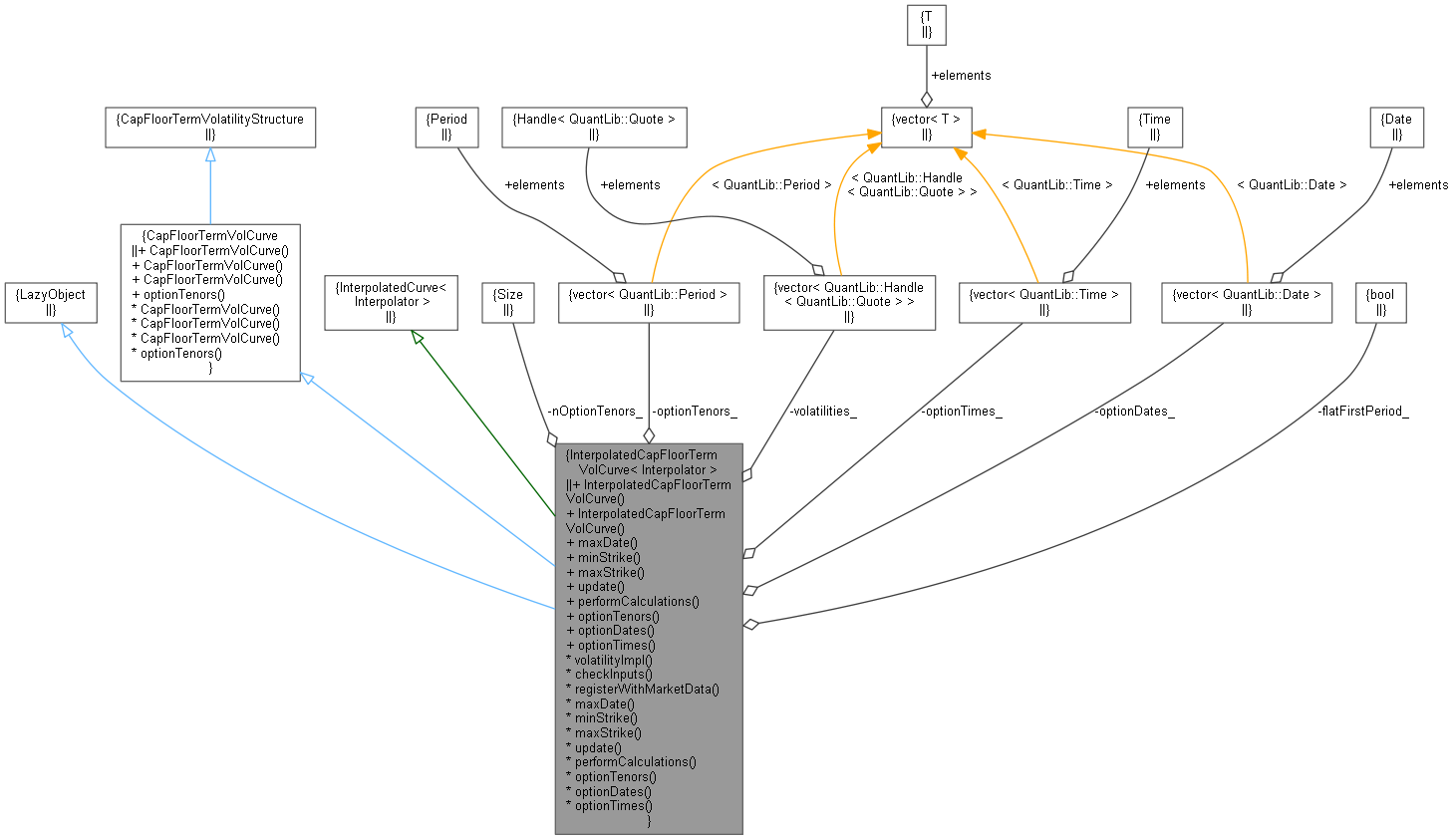

Inheritance diagram for InterpolatedCapFloorTermVolCurve< Interpolator >: Collaboration diagram for InterpolatedCapFloorTermVolCurve< Interpolator >:

Inheritance diagram for InterpolatedCapFloorTermVolCurve< Interpolator >: Collaboration diagram for InterpolatedCapFloorTermVolCurve< Interpolator >:Public Member Functions | |

| InterpolatedCapFloorTermVolCurve (QuantLib::Natural settlementDays, const QuantLib::Calendar &calendar, QuantLib::BusinessDayConvention bdc, const std::vector< QuantLib::Period > &optionTenors, const std::vector< QuantLib::Handle< QuantLib::Quote > > &volatilities, const QuantLib::DayCounter &dayCounter=QuantLib::Actual365Fixed(), bool flatFirstPeriod=true, const Interpolator &interpolator=Interpolator()) | |

| InterpolatedCapFloorTermVolCurve (const QuantLib::Date &settlementDate, const QuantLib::Calendar &calendar, QuantLib::BusinessDayConvention bdc, const std::vector< QuantLib::Period > &optionTenors, const std::vector< QuantLib::Handle< QuantLib::Quote > > &volatilities, const QuantLib::DayCounter &dayCounter=QuantLib::Actual365Fixed(), bool flatFirstPeriod=true, const Interpolator &interpolator=Interpolator()) | |

TermStructure interface | |

| QuantLib::Date | maxDate () const override |

VolatilityTermStructure interface | |

| QuantLib::Rate | minStrike () const override |

| QuantLib::Rate | maxStrike () const override |

LazyObject interface | |

| void | update () override |

| void | performCalculations () const override |

CapFloorTermVolCurve interface | |

| std::vector< QuantLib::Period > | optionTenors () const override |

| Return the tenors used in the CapFloorTermVolCurve. More... | |

Inspectors | |

| const std::vector< QuantLib::Date > & | optionDates () const |

| const std::vector< QuantLib::Time > & | optionTimes () const |

| Public Member Functions inherited from CapFloorTermVolCurve | |

| CapFloorTermVolCurve (QuantLib::BusinessDayConvention bdc, const QuantLib::DayCounter &dc=QuantLib::DayCounter()) | |

| CapFloorTermVolCurve (const QuantLib::Date &referenceDate, const QuantLib::Calendar &cal, QuantLib::BusinessDayConvention bdc, const QuantLib::DayCounter &dc=QuantLib::DayCounter()) | |

| CapFloorTermVolCurve (QuantLib::Natural settlementDays, const QuantLib::Calendar &cal, QuantLib::BusinessDayConvention bdc, const QuantLib::DayCounter &dc=QuantLib::DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

CapFloorTermVolatilityStructure interface | |

| QuantLib::Size | nOptionTenors_ |

| Number of underlying cap floor instruments. More... | |

| std::vector< QuantLib::Period > | optionTenors_ |

| Underlying cap floor tenors. More... | |

| std::vector< QuantLib::Date > | optionDates_ |

| std::vector< QuantLib::Time > | optionTimes_ |

| std::vector< QuantLib::Handle< QuantLib::Quote > > | volatilities_ |

| Cap floor term volatility quotes. More... | |

| bool | flatFirstPeriod_ |

| True for flat volatility from time zero to the first cap floor date. More... | |

| QuantLib::Volatility | volatilityImpl (QuantLib::Time length, QuantLib::Rate) const override |

| void | checkInputs () const |

| Check the constructor arguments for consistency. More... | |

| void | registerWithMarketData () |

| Register this curve with the volatility quotes. More... | |

Interpolated cap floor term volatility curve.

Class that interpolates a vector of cap floor volatilities.

Based on the class QuantLib::CapFloorTermVolCurve with changes:

Definition at line 70 of file capfloortermvolcurve.hpp.

| InterpolatedCapFloorTermVolCurve | ( | QuantLib::Natural | settlementDays, |

| const QuantLib::Calendar & | calendar, | ||

| QuantLib::BusinessDayConvention | bdc, | ||

| const std::vector< QuantLib::Period > & | optionTenors, | ||

| const std::vector< QuantLib::Handle< QuantLib::Quote > > & | volatilities, | ||

| const QuantLib::DayCounter & | dayCounter = QuantLib::Actual365Fixed(), |

||

| bool | flatFirstPeriod = true, |

||

| const Interpolator & | interpolator = Interpolator() |

||

| ) |

Constructor with floating reference date

| settlementDays | Number of days from evaluation date to curve reference date. |

| calendar | The calendar used to derive cap floor maturity dates from optionTenors. Also used to advance from today to reference date if necessary. |

| bdc | The business day convention used to derive cap floor maturity dates from optionTenors. |

| optionTenors | The cap floor tenors. The first tenor must be positive. |

| volatilities | The cap floor volatility quotes. |

| dayCounter | The day counter used to convert from dates to times. |

| flatFirstPeriod | Set to true to use the first element of volatilities between time zero and the first element of optionTenors. If this is false, the volatility at time zero is set to zero and interpolation between time and the first element of optionTenors is used. |

| interpolator | An instance of the interpolator to use. Allows for specification of Interpolator instances that use a constructor that takes arguments. |

Definition at line 184 of file capfloortermvolcurve.hpp.

Here is the call graph for this function:| InterpolatedCapFloorTermVolCurve | ( | const QuantLib::Date & | settlementDate, |

| const QuantLib::Calendar & | calendar, | ||

| QuantLib::BusinessDayConvention | bdc, | ||

| const std::vector< QuantLib::Period > & | optionTenors, | ||

| const std::vector< QuantLib::Handle< QuantLib::Quote > > & | volatilities, | ||

| const QuantLib::DayCounter & | dayCounter = QuantLib::Actual365Fixed(), |

||

| bool | flatFirstPeriod = true, |

||

| const Interpolator & | interpolator = Interpolator() |

||

| ) |

Constructor with fixed reference date

| settlementDate | The curve reference date. |

| calendar | The calendar used to derive cap floor maturity dates from optionTenors. Also used to advance from today to reference date if necessary. |

| bdc | The business day convention used to derive cap floor maturity dates from optionTenors. |

| optionTenors | The cap floor tenors. The first tenor must be positive. |

| volatilities | The cap floor volatility quotes. |

| dayCounter | The day counter used to convert from dates to times. |

| flatFirstPeriod | Set to true to use the first element of volatilities between time zero and the first element of optionTenors. If this is false, the volatility at time zero is set to zero and interpolation between time and the first element of optionTenors is used. |

| interpolator | An instance of the interpolator to use. Allows for specification of Interpolator instances that use a constructor that takes arguments. |

Definition at line 199 of file capfloortermvolcurve.hpp.

Here is the call graph for this function:

|

override |

Definition at line 213 of file capfloortermvolcurve.hpp.

|

override |

Definition at line 218 of file capfloortermvolcurve.hpp.

|

override |

Definition at line 222 of file capfloortermvolcurve.hpp.

|

override |

Definition at line 226 of file capfloortermvolcurve.hpp.

|

override |

Definition at line 231 of file capfloortermvolcurve.hpp.

|

overridevirtual |

Return the tenors used in the CapFloorTermVolCurve.

Implements CapFloorTermVolCurve.

Definition at line 251 of file capfloortermvolcurve.hpp.

| const std::vector< QuantLib::Date > & optionDates |

Definition at line 257 of file capfloortermvolcurve.hpp.

| const std::vector< QuantLib::Time > & optionTimes |

Definition at line 263 of file capfloortermvolcurve.hpp.

|

overrideprotected |

Definition at line 269 of file capfloortermvolcurve.hpp.

|

private |

Check the constructor arguments for consistency.

Definition at line 280 of file capfloortermvolcurve.hpp.

Here is the caller graph for this function:

|

private |

Register this curve with the volatility quotes.

Definition at line 294 of file capfloortermvolcurve.hpp.

Here is the caller graph for this function:

|

private |

Number of underlying cap floor instruments.

Definition at line 161 of file capfloortermvolcurve.hpp.

|

private |

Underlying cap floor tenors.

Definition at line 164 of file capfloortermvolcurve.hpp.

|

mutableprivate |

Underlying cap floor maturity dates. Mutable since if the curve is moving, the dates need to be updated from const method.

Definition at line 169 of file capfloortermvolcurve.hpp.

|

mutableprivate |

Time to maturity of underlying cap floor instruments. Mutable since if the curve is moving, the times need to be updated from const method.

Definition at line 174 of file capfloortermvolcurve.hpp.

|

private |

Cap floor term volatility quotes.

Definition at line 177 of file capfloortermvolcurve.hpp.

|

private |

True for flat volatility from time zero to the first cap floor date.

Definition at line 180 of file capfloortermvolcurve.hpp.