Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Base class for CPI CashFLow and Coupon pricers. More...

#include <qle/cashflows/cpicouponpricer.hpp>

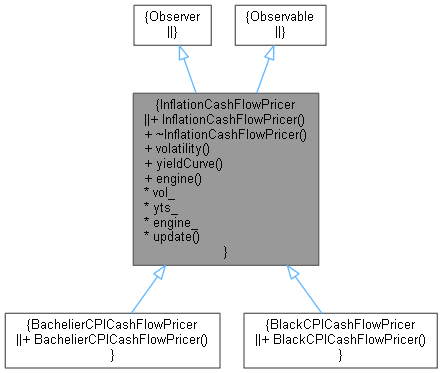

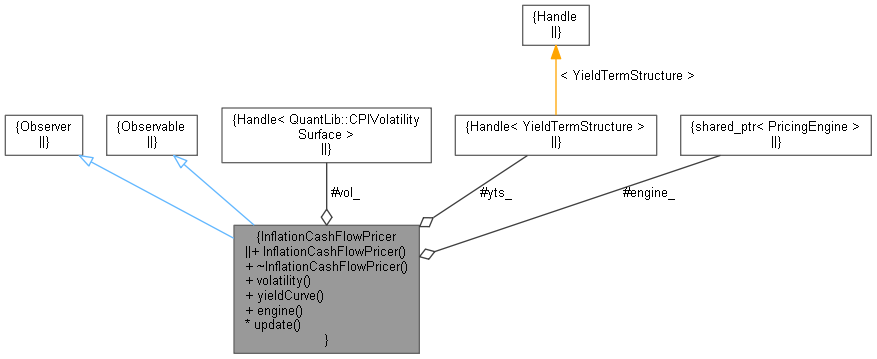

Inheritance diagram for InflationCashFlowPricer: Collaboration diagram for InflationCashFlowPricer:

Inheritance diagram for InflationCashFlowPricer: Collaboration diagram for InflationCashFlowPricer:Public Member Functions | |

| InflationCashFlowPricer (const Handle< QuantLib::CPIVolatilitySurface > &vol=Handle< QuantLib::CPIVolatilitySurface >(), const Handle< YieldTermStructure > &yts=Handle< YieldTermStructure >()) | |

| virtual | ~InflationCashFlowPricer () |

| Handle< QuantLib::CPIVolatilitySurface > | volatility () |

| Inspectors. More... | |

| Handle< YieldTermStructure > | yieldCurve () |

| QuantLib::ext::shared_ptr< PricingEngine > | engine () |

Observer interface | |

| Handle< QuantLib::CPIVolatilitySurface > | vol_ |

| Handle< YieldTermStructure > | yts_ |

| QuantLib::ext::shared_ptr< PricingEngine > | engine_ |

| virtual void | update () override |

Base class for CPI CashFLow and Coupon pricers.

Definition at line 39 of file cpicouponpricer.hpp.

| InflationCashFlowPricer | ( | const Handle< QuantLib::CPIVolatilitySurface > & | vol = Handle<QuantLib::CPIVolatilitySurface>(), |

| const Handle< YieldTermStructure > & | yts = Handle<YieldTermStructure>() |

||

| ) |

Definition at line 31 of file cpicouponpricer.cpp.

|

virtual |

Definition at line 43 of file cpicouponpricer.hpp.

| Handle< QuantLib::CPIVolatilitySurface > volatility | ( | ) |

Inspectors.

Definition at line 47 of file cpicouponpricer.hpp.

Here is the caller graph for this function:| Handle< YieldTermStructure > yieldCurve | ( | ) |

| QuantLib::ext::shared_ptr< PricingEngine > engine | ( | ) |

Definition at line 49 of file cpicouponpricer.hpp.

|

overridevirtual |

Definition at line 54 of file cpicouponpricer.hpp.

|

protected |

Definition at line 57 of file cpicouponpricer.hpp.

|

protected |

Definition at line 58 of file cpicouponpricer.hpp.

|

protected |

Definition at line 59 of file cpicouponpricer.hpp.