Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Base class for FX Linked cashflows. More...

#include <qle/cashflows/fxlinkedcashflow.hpp>

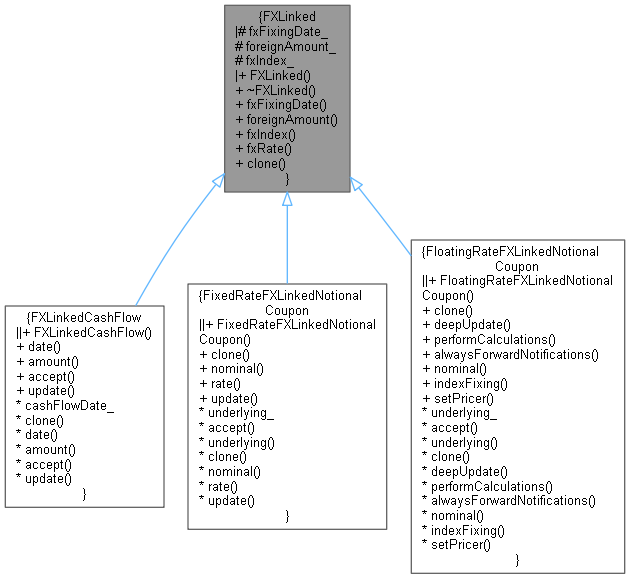

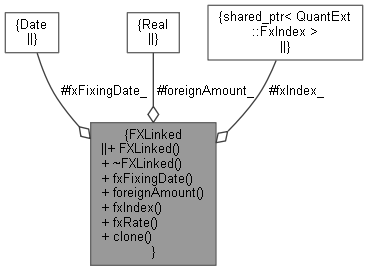

Inheritance diagram for FXLinked: Collaboration diagram for FXLinked:

Inheritance diagram for FXLinked: Collaboration diagram for FXLinked:Public Member Functions | |

| FXLinked (const Date &fixingDate, Real foreignAmount, QuantLib::ext::shared_ptr< FxIndex > fxIndex) | |

| virtual | ~FXLinked () |

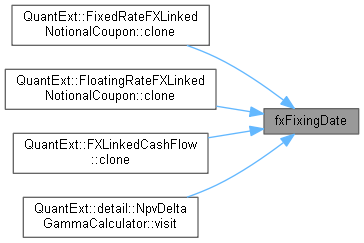

| Date | fxFixingDate () const |

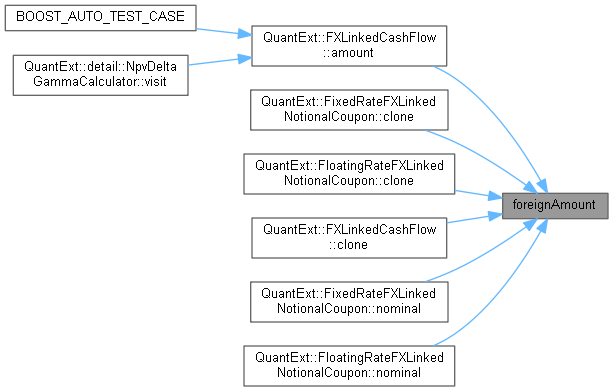

| Real | foreignAmount () const |

| const QuantLib::ext::shared_ptr< FxIndex > & | fxIndex () const |

| Real | fxRate () const |

| virtual QuantLib::ext::shared_ptr< FXLinked > | clone (QuantLib::ext::shared_ptr< FxIndex > fxIndex)=0 |

Protected Attributes | |

| Date | fxFixingDate_ |

| Real | foreignAmount_ |

| QuantLib::ext::shared_ptr< FxIndex > | fxIndex_ |

Base class for FX Linked cashflows.

Definition at line 39 of file fxlinkedcashflow.hpp.

| FXLinked | ( | const Date & | fixingDate, |

| Real | foreignAmount, | ||

| QuantLib::ext::shared_ptr< FxIndex > | fxIndex | ||

| ) |

Definition at line 24 of file fxlinkedcashflow.cpp.

|

virtual |

Definition at line 42 of file fxlinkedcashflow.hpp.

| Date fxFixingDate | ( | ) | const |

| Real foreignAmount | ( | ) | const |

| const QuantLib::ext::shared_ptr< FxIndex > & fxIndex | ( | ) | const |

| Real fxRate | ( | ) | const |

|

pure virtual |

Implemented in FixedRateFXLinkedNotionalCoupon, FloatingRateFXLinkedNotionalCoupon, and FXLinkedCashFlow.

|

protected |

Definition at line 51 of file fxlinkedcashflow.hpp.

|

protected |

Definition at line 52 of file fxlinkedcashflow.hpp.

|

protected |

Definition at line 53 of file fxlinkedcashflow.hpp.