Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <qle/pricingengines/discountingriskybondenginemultistate.hpp>

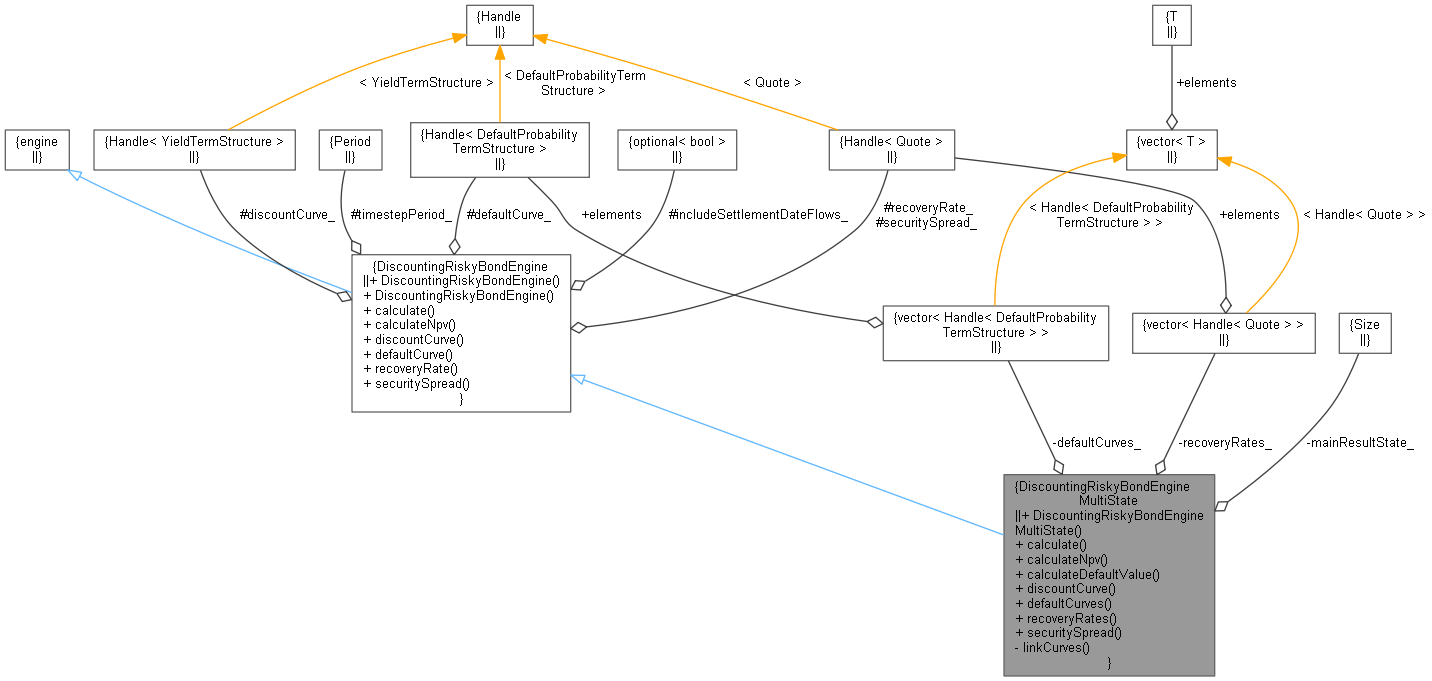

Inheritance diagram for DiscountingRiskyBondEngineMultiState: Collaboration diagram for DiscountingRiskyBondEngineMultiState:

Inheritance diagram for DiscountingRiskyBondEngineMultiState: Collaboration diagram for DiscountingRiskyBondEngineMultiState:Public Member Functions | |

| DiscountingRiskyBondEngineMultiState (const Handle< YieldTermStructure > &discountCurve, const std::vector< Handle< DefaultProbabilityTermStructure > > &defaultCurves, const std::vector< Handle< Quote > > &recoveryRates, const Size mainResultState, const Handle< Quote > &securitySpread, Period timestepPeriod, const boost::optional< bool > includeSettlementDateFlows=boost::none) | |

| void | calculate () const |

| Real | calculateNpv (const Size state) const |

| Real | calculateDefaultValue () const |

| Handle< YieldTermStructure > | discountCurve () const |

| const std::vector< Handle< DefaultProbabilityTermStructure > > & | defaultCurves () const |

| const std::vector< Handle< Quote > > & | recoveryRates () const |

| Handle< Quote > | securitySpread () const |

| Public Member Functions inherited from DiscountingRiskyBondEngine | |

| DiscountingRiskyBondEngine (const Handle< YieldTermStructure > &discountCurve, const Handle< DefaultProbabilityTermStructure > &defaultCurve, const Handle< Quote > &recoveryRate, const Handle< Quote > &securitySpread, Period timestepPeriod, boost::optional< bool > includeSettlementDateFlows=boost::none) | |

| DiscountingRiskyBondEngine (const Handle< YieldTermStructure > &discountCurve, const Handle< Quote > &securitySpread, Period timestepPeriod, boost::optional< bool > includeSettlementDateFlows=boost::none) | |

| alternative constructor (does not require default curve or recovery rate) More... | |

| void | calculate () const override |

| BondNPVCalculationResults | calculateNpv (const Date &npvDate, const Date &settlementDate, const Leg &cashflows, boost::optional< bool > includeSettlementDateFlows=boost::none, const Handle< YieldTermStructure > &incomeCurve=Handle< YieldTermStructure >(), const bool conditionalOnSurvival=true, const bool additionalResults=true) const |

| Handle< YieldTermStructure > | discountCurve () const |

| Handle< DefaultProbabilityTermStructure > | defaultCurve () const |

| Handle< Quote > | recoveryRate () const |

| Handle< Quote > | securitySpread () const |

Private Member Functions | |

| void | linkCurves (Size i) const |

Private Attributes | |

| const std::vector< Handle< DefaultProbabilityTermStructure > > | defaultCurves_ |

| const std::vector< Handle< Quote > > | recoveryRates_ |

| const Size | mainResultState_ |

Additional Inherited Members | |

| Protected Attributes inherited from DiscountingRiskyBondEngine | |

| Handle< YieldTermStructure > | discountCurve_ |

| Handle< DefaultProbabilityTermStructure > | defaultCurve_ |

| Handle< Quote > | recoveryRate_ |

| Handle< Quote > | securitySpread_ |

| Period | timestepPeriod_ |

| boost::optional< bool > | includeSettlementDateFlows_ |

The engine takes a vector of default curves and recovery rates. For the given main result state it will produce the same results as the MidPointCdsEngine. In addition a result with label "stateNPV" is produced containing the NPV for each given default curve / recovery rate and an additional entry with a default value w.r.t. the last given recovery rate in the vector.

Definition at line 36 of file discountingriskybondenginemultistate.hpp.

| DiscountingRiskyBondEngineMultiState | ( | const Handle< YieldTermStructure > & | discountCurve, |

| const std::vector< Handle< DefaultProbabilityTermStructure > > & | defaultCurves, | ||

| const std::vector< Handle< Quote > > & | recoveryRates, | ||

| const Size | mainResultState, | ||

| const Handle< Quote > & | securitySpread, | ||

| Period | timestepPeriod, | ||

| const boost::optional< bool > | includeSettlementDateFlows = boost::none |

||

| ) |

Definition at line 30 of file discountingriskybondenginemultistate.cpp.

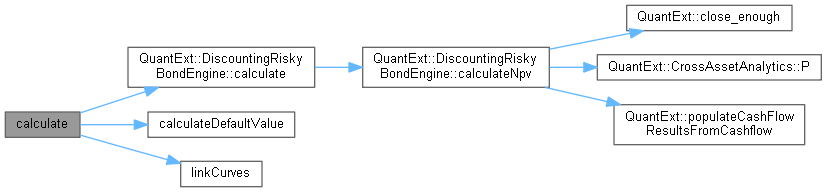

Here is the call graph for this function:| void calculate | ( | ) | const |

Definition at line 55 of file discountingriskybondenginemultistate.cpp.

Here is the call graph for this function:| Real calculateNpv | ( | const Size | state | ) | const |

| Real calculateDefaultValue | ( | ) | const |

Definition at line 83 of file discountingriskybondenginemultistate.cpp.

Here is the caller graph for this function:| Handle< YieldTermStructure > discountCurve | ( | ) | const |

Definition at line 47 of file discountingriskybondenginemultistate.hpp.

| const std::vector< Handle< DefaultProbabilityTermStructure > > & defaultCurves | ( | ) | const |

Definition at line 48 of file discountingriskybondenginemultistate.hpp.

Here is the caller graph for this function:| const std::vector< Handle< Quote > > & recoveryRates | ( | ) | const |

Definition at line 49 of file discountingriskybondenginemultistate.hpp.

| Handle< Quote > securitySpread | ( | ) | const |

Definition at line 50 of file discountingriskybondenginemultistate.hpp.

|

private |

Definition at line 50 of file discountingriskybondenginemultistate.cpp.

Here is the caller graph for this function:

|

private |

Definition at line 54 of file discountingriskybondenginemultistate.hpp.

|

private |

Definition at line 55 of file discountingriskybondenginemultistate.hpp.

|

private |

Definition at line 56 of file discountingriskybondenginemultistate.hpp.