Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Cross currency price term structure. More...

#include <qle/termstructures/crosscurrencypricetermstructure.hpp>

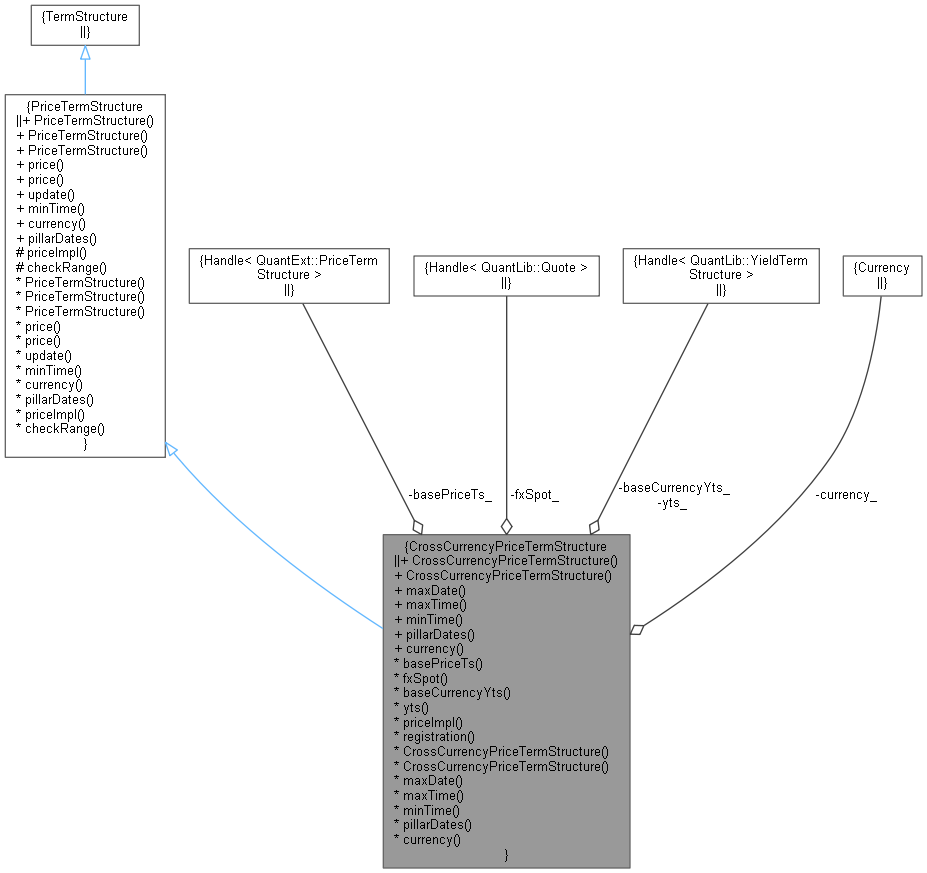

Inheritance diagram for CrossCurrencyPriceTermStructure: Collaboration diagram for CrossCurrencyPriceTermStructure:

Inheritance diagram for CrossCurrencyPriceTermStructure: Collaboration diagram for CrossCurrencyPriceTermStructure:Public Member Functions | |

Constructors | |

| CrossCurrencyPriceTermStructure (const QuantLib::Date &referenceDate, const QuantLib::Handle< PriceTermStructure > &basePriceTs, const QuantLib::Handle< QuantLib::Quote > &fxSpot, const QuantLib::Handle< QuantLib::YieldTermStructure > &baseCurrencyYts, const QuantLib::Handle< QuantLib::YieldTermStructure > &yts, const QuantLib::Currency ¤cy) | |

| CrossCurrencyPriceTermStructure (QuantLib::Natural settlementDays, const QuantLib::Handle< PriceTermStructure > &basePriceTs, const QuantLib::Handle< QuantLib::Quote > &fxSpot, const QuantLib::Handle< QuantLib::YieldTermStructure > &baseCurrencyYts, const QuantLib::Handle< QuantLib::YieldTermStructure > &yts, const QuantLib::Currency ¤cy) | |

TermStructure interface | |

| QuantLib::Date | maxDate () const override |

| QuantLib::Time | maxTime () const override |

PriceTermStructure interface | |

| QuantLib::Time | minTime () const override |

| The minimum time for which the curve can return values. More... | |

| std::vector< QuantLib::Date > | pillarDates () const override |

| The pillar dates for the PriceTermStructure. More... | |

| const QuantLib::Currency & | currency () const override |

| The currency in which prices are expressed. More... | |

| Public Member Functions inherited from PriceTermStructure | |

| PriceTermStructure (const QuantLib::DayCounter &dc=QuantLib::DayCounter()) | |

| PriceTermStructure (const QuantLib::Date &referenceDate, const QuantLib::Calendar &cal=QuantLib::Calendar(), const QuantLib::DayCounter &dc=QuantLib::DayCounter()) | |

| PriceTermStructure (QuantLib::Natural settlementDays, const QuantLib::Calendar &cal, const QuantLib::DayCounter &dc=QuantLib::DayCounter()) | |

| QuantLib::Real | price (QuantLib::Time t, bool extrapolate=false) const |

| QuantLib::Real | price (const QuantLib::Date &d, bool extrapolate=false) const |

| void | update () override |

Inspectors | |

| QuantLib::Handle< PriceTermStructure > | basePriceTs_ |

| QuantLib::Handle< QuantLib::Quote > | fxSpot_ |

| QuantLib::Handle< QuantLib::YieldTermStructure > | baseCurrencyYts_ |

| QuantLib::Handle< QuantLib::YieldTermStructure > | yts_ |

| QuantLib::Currency | currency_ |

| const QuantLib::Handle< PriceTermStructure > & | basePriceTs () const |

| The price term structure in base currency. More... | |

| const QuantLib::Handle< QuantLib::Quote > & | fxSpot () const |

| The FX spot rate, number of units of this price term structure's currency per unit of the base currency. More... | |

| const QuantLib::Handle< QuantLib::YieldTermStructure > & | baseCurrencyYts () const |

| The yield term structure for the base currency. More... | |

| const QuantLib::Handle< QuantLib::YieldTermStructure > & | yts () const |

| The yield term structure for this price term structure's currency. More... | |

| QuantLib::Real | priceImpl (QuantLib::Time t) const override |

| Price calculation. More... | |

| void | registration () |

| Register with underlying market data. More... | |

Additional Inherited Members | |

| Protected Member Functions inherited from PriceTermStructure | |

| void | checkRange (QuantLib::Time t, bool extrapolate) const |

| Extra time range check for minimum time, then calls TermStructure::checkRange. More... | |

Cross currency price term structure.

This class creates a price term structure in a given currency using an already constructed price term structure in a different currency.

Definition at line 37 of file crosscurrencypricetermstructure.hpp.

| CrossCurrencyPriceTermStructure | ( | const QuantLib::Date & | referenceDate, |

| const QuantLib::Handle< PriceTermStructure > & | basePriceTs, | ||

| const QuantLib::Handle< QuantLib::Quote > & | fxSpot, | ||

| const QuantLib::Handle< QuantLib::YieldTermStructure > & | baseCurrencyYts, | ||

| const QuantLib::Handle< QuantLib::YieldTermStructure > & | yts, | ||

| const QuantLib::Currency & | currency | ||

| ) |

Fixed reference date based price term structure.

| referenceDate | This price term structure's reference date. |

| basePriceTs | The price term structure in base currency units. |

| fxSpot | The number of units of this price term structure's currency per unit of the base price term structure's currency. |

| baseCurrencyYts | The yield term structure for the base currency. |

| yts | The yield term structure for this price term structure's currency. |

| currency | The price term structure's currency. |

Definition at line 34 of file crosscurrencypricetermstructure.cpp.

Here is the call graph for this function:| CrossCurrencyPriceTermStructure | ( | QuantLib::Natural | settlementDays, |

| const QuantLib::Handle< PriceTermStructure > & | basePriceTs, | ||

| const QuantLib::Handle< QuantLib::Quote > & | fxSpot, | ||

| const QuantLib::Handle< QuantLib::YieldTermStructure > & | baseCurrencyYts, | ||

| const QuantLib::Handle< QuantLib::YieldTermStructure > & | yts, | ||

| const QuantLib::Currency & | currency | ||

| ) |

Floating reference date based price term structure.

| settlementDays | This price term structure's settlement days. |

| basePriceTs | The price term structure in base currency units. |

| fxSpot | The number of units of this price term structure's currency per unit of the base price term structure's currency. |

| baseCurrencyYts | The yield term structure for the base currency. |

| yts | The yield term structure for this price term structure's currency. |

| currency | The price term structure's currency. |

|

override |

Definition at line 54 of file crosscurrencypricetermstructure.cpp.

Here is the call graph for this function:

|

override |

Definition at line 58 of file crosscurrencypricetermstructure.cpp.

Here is the call graph for this function:

|

overridevirtual |

The minimum time for which the curve can return values.

Reimplemented from PriceTermStructure.

Definition at line 62 of file crosscurrencypricetermstructure.cpp.

|

overridevirtual |

The pillar dates for the PriceTermStructure.

Implements PriceTermStructure.

Definition at line 64 of file crosscurrencypricetermstructure.cpp.

|

overridevirtual |

The currency in which prices are expressed.

Implements PriceTermStructure.

Definition at line 84 of file crosscurrencypricetermstructure.hpp.

| const QuantLib::Handle< PriceTermStructure > & basePriceTs | ( | ) | const |

The price term structure in base currency.

Definition at line 90 of file crosscurrencypricetermstructure.hpp.

| const QuantLib::Handle< QuantLib::Quote > & fxSpot | ( | ) | const |

The FX spot rate, number of units of this price term structure's currency per unit of the base currency.

Definition at line 93 of file crosscurrencypricetermstructure.hpp.

| const QuantLib::Handle< QuantLib::YieldTermStructure > & baseCurrencyYts | ( | ) | const |

The yield term structure for the base currency.

Definition at line 96 of file crosscurrencypricetermstructure.hpp.

| const QuantLib::Handle< QuantLib::YieldTermStructure > & yts | ( | ) | const |

The yield term structure for this price term structure's currency.

Definition at line 99 of file crosscurrencypricetermstructure.hpp.

|

overrideprotectedvirtual |

Price calculation.

Implements PriceTermStructure.

Definition at line 66 of file crosscurrencypricetermstructure.cpp.

|

private |

Register with underlying market data.

Definition at line 72 of file crosscurrencypricetermstructure.cpp.

Here is the caller graph for this function:

|

private |

Definition at line 110 of file crosscurrencypricetermstructure.hpp.

|

private |

Definition at line 111 of file crosscurrencypricetermstructure.hpp.

|

private |

Definition at line 112 of file crosscurrencypricetermstructure.hpp.

|

private |

Definition at line 113 of file crosscurrencypricetermstructure.hpp.

|

private |

Definition at line 114 of file crosscurrencypricetermstructure.hpp.