Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Cox-Ingersoll-Ross ++ credit model class. More...

#include <qle/models/crcirpp.hpp>

Inheritance diagram for CrCirpp: Collaboration diagram for CrCirpp:

Inheritance diagram for CrCirpp: Collaboration diagram for CrCirpp:Public Member Functions | |

| CrCirpp (const QuantLib::ext::shared_ptr< CrCirppParametrization > ¶metrization) | |

| Real | zeroBond (Real t, Real T, Real y) const |

| Real | survivalProbability (Real t, Real T, Real y) const |

| Real | densityForwardMeasure (Real x, Real t) |

| Real | cumulativeForwardMeasure (Real x, Real t) |

| Real | density (Real x, Real t) |

| Real | cumulative (Real x, Real t) |

| Real | zeroBondOption (Real eval_t, Real expiry_T, Real maturity_tau, Real strike_k, Real y_t, Real w) |

| Handle< DefaultProbabilityTermStructure > | defaultCurve (std::vector< Date > dateGrid=std::vector< Date >()) const |

| const QuantLib::ext::shared_ptr< CrCirppParametrization > | parametrization () const |

| const QuantLib::ext::shared_ptr< StochasticProcess > | stateProcess () const |

| Real | A (Real t, Real T) const |

| Real | B (Real t, Real T) const |

| void | update () override |

| void | generateArguments () override |

| Public Member Functions inherited from LinkableCalibratedModel | |

| LinkableCalibratedModel () | |

| void | update () override |

| virtual void | calibrate (const std::vector< QuantLib::ext::shared_ptr< CalibrationHelper > > &, OptimizationMethod &method, const EndCriteria &endCriteria, const Constraint &constraint=Constraint(), const std::vector< Real > &weights=std::vector< Real >(), const std::vector< bool > &fixParameters=std::vector< bool >()) |

| Calibrate to a set of market instruments (usually caps/swaptions) More... | |

| virtual void | calibrate (const std::vector< QuantLib::ext::shared_ptr< BlackCalibrationHelper > > &, OptimizationMethod &method, const EndCriteria &endCriteria, const Constraint &constraint=Constraint(), const std::vector< Real > &weights=std::vector< Real >(), const std::vector< bool > &fixParameters=std::vector< bool >()) |

| for backward compatibility More... | |

| Real | value (const Array ¶ms, const std::vector< QuantLib::ext::shared_ptr< CalibrationHelper > > &) |

| Real | value (const Array ¶ms, const std::vector< QuantLib::ext::shared_ptr< BlackCalibrationHelper > > &) |

| for backward compatibility More... | |

| const QuantLib::ext::shared_ptr< Constraint > & | constraint () const |

| EndCriteria::Type | endCriteria () const |

| Returns end criteria result. More... | |

| const Array & | problemValues () const |

| Returns the problem values. More... | |

| Array | params () const |

| Returns array of arguments on which calibration is done. More... | |

| virtual void | setParams (const Array ¶ms) |

| virtual void | setParam (Size idx, const Real value) |

Private Attributes | |

| QuantLib::ext::shared_ptr< CrCirppParametrization > | parametrization_ |

| QuantLib::ext::shared_ptr< CrCirppStateProcess > | stateProcess_ |

Additional Inherited Members | |

| virtual void | generateArguments () |

| Protected Attributes inherited from LinkableCalibratedModel | |

| std::vector< QuantLib::ext::shared_ptr< Parameter > > | arguments_ |

| QuantLib::ext::shared_ptr< Constraint > | constraint_ |

| EndCriteria::Type | endCriteria_ |

| Array | problemValues_ |

Cox-Ingersoll-Ross ++ credit model class.

This class implements the Cox-Ingersoll-Ross model defined by

\[ \lambda(t) = y(t) + \psi (t) \\ dy(t) = a(\theta - y(t)) dt + \sigma \, \sqrt{y(t)} \, dW \]

Definition at line 48 of file crcirpp.hpp.

| CrCirpp | ( | const QuantLib::ext::shared_ptr< CrCirppParametrization > & | parametrization | ) |

Definition at line 42 of file crcirpp.cpp.

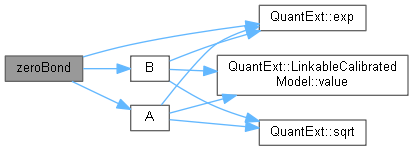

| Real zeroBond | ( | Real | t, |

| Real | T, | ||

| Real | y | ||

| ) | const |

Definition at line 124 of file crcirpp.cpp.

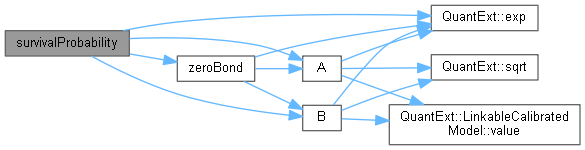

Here is the call graph for this function: Here is the caller graph for this function:| Real survivalProbability | ( | Real | t, |

| Real | T, | ||

| Real | y | ||

| ) | const |

Definition at line 126 of file crcirpp.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| Real densityForwardMeasure | ( | Real | x, |

| Real | t | ||

| ) |

Definition at line 176 of file crcirpp.cpp.

Here is the call graph for this function:| Real cumulativeForwardMeasure | ( | Real | x, |

| Real | t | ||

| ) |

Definition at line 198 of file crcirpp.cpp.

Here is the call graph for this function:| Real density | ( | Real | x, |

| Real | t | ||

| ) |

Definition at line 142 of file crcirpp.cpp.

Here is the call graph for this function:| Real cumulative | ( | Real | x, |

| Real | t | ||

| ) |

Definition at line 159 of file crcirpp.cpp.

Here is the call graph for this function:| Real zeroBondOption | ( | Real | eval_t, |

| Real | expiry_T, | ||

| Real | maturity_tau, | ||

| Real | strike_k, | ||

| Real | y_t, | ||

| Real | w | ||

| ) |

Definition at line 220 of file crcirpp.cpp.

Here is the call graph for this function:| Handle< DefaultProbabilityTermStructure > defaultCurve | ( | std::vector< Date > | dateGrid = std::vector<Date>() | ) | const |

Definition at line 59 of file crcirpp.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| const QuantLib::ext::shared_ptr< CrCirppParametrization > parametrization | ( | ) | const |

| const QuantLib::ext::shared_ptr< StochasticProcess > stateProcess | ( | ) | const |

Definition at line 92 of file crcirpp.hpp.

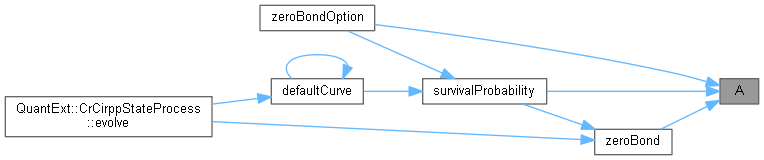

| Real A | ( | Real | t, |

| Real | T | ||

| ) | const |

Definition at line 93 of file crcirpp.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| Real B | ( | Real | t, |

| Real | T | ||

| ) | const |

Definition at line 109 of file crcirpp.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

override |

observer and linked calibrated model interface

Definition at line 81 of file crcirpp.hpp.

Here is the caller graph for this function:

|

overridevirtual |

Reimplemented from LinkableCalibratedModel.

Definition at line 86 of file crcirpp.hpp.

Here is the call graph for this function:

|

private |

Definition at line 77 of file crcirpp.hpp.

|

private |

Definition at line 78 of file crcirpp.hpp.