Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <qle/indexes/compoequityindex.hpp>

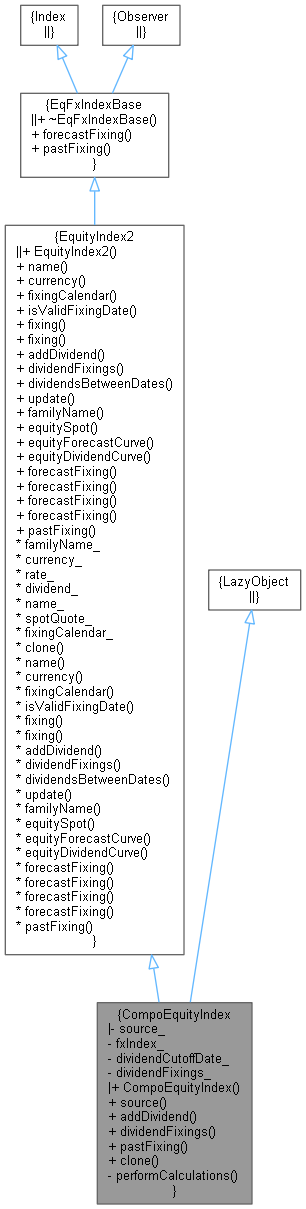

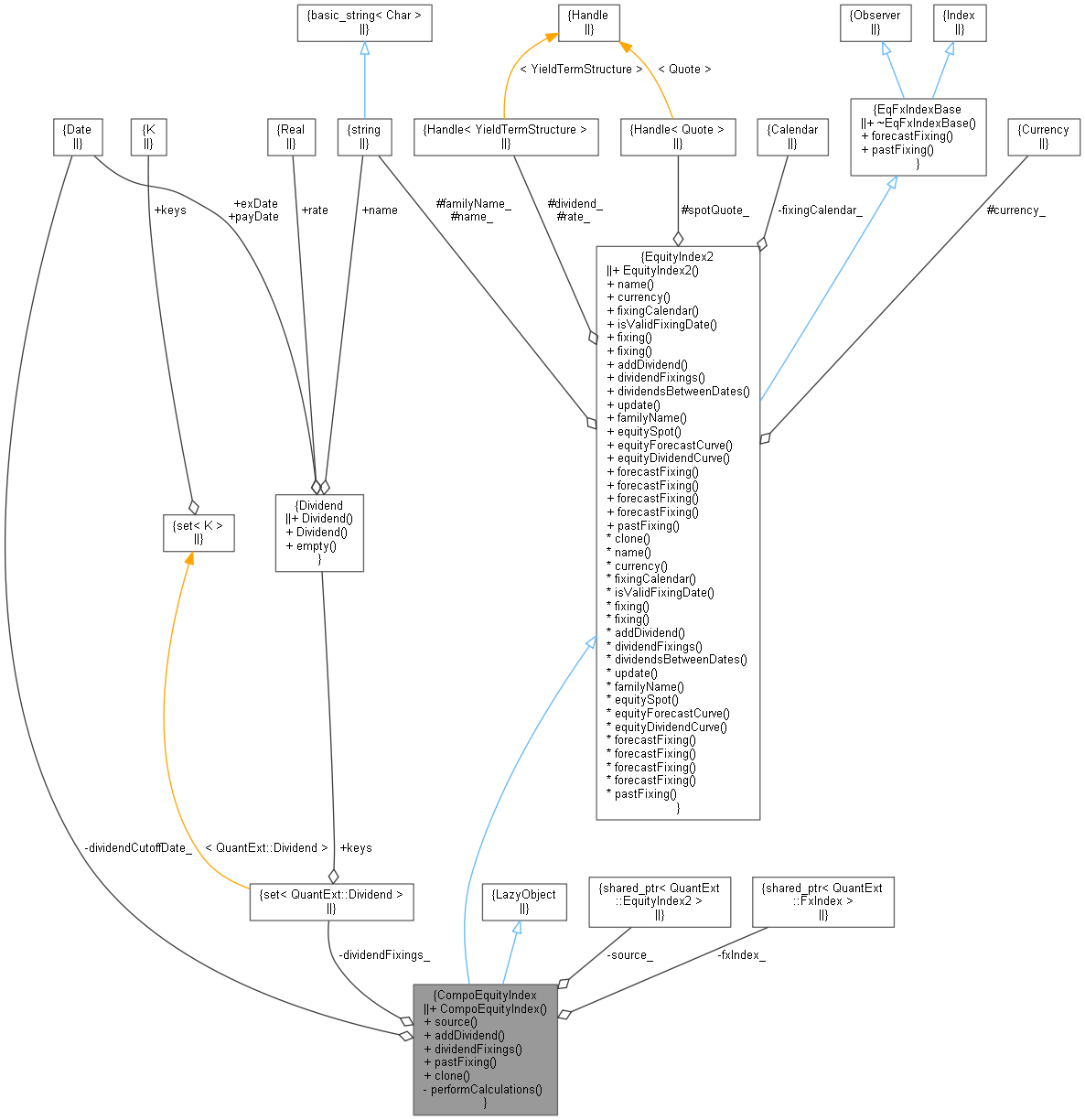

Inheritance diagram for CompoEquityIndex: Collaboration diagram for CompoEquityIndex:

Inheritance diagram for CompoEquityIndex: Collaboration diagram for CompoEquityIndex:Public Member Functions | |

| CompoEquityIndex (const QuantLib::ext::shared_ptr< QuantExt::EquityIndex2 > &source, const QuantLib::ext::shared_ptr< FxIndex > &fxIndex, const Date ÷ndCutoffDate=Date()) | |

| QuantLib::ext::shared_ptr< QuantExt::EquityIndex2 > | source () const |

| void | addDividend (const Dividend ÷nd, bool forceOverwrite=false) override |

| stores the historical dividend at the given date More... | |

| const std::set< Dividend > & | dividendFixings () const override |

| Real | pastFixing (const Date &fixingDate) const override |

| returns a past fixing at the given date More... | |

| QuantLib::ext::shared_ptr< QuantExt::EquityIndex2 > | clone (const Handle< Quote > spotQuote, const Handle< YieldTermStructure > &rate, const Handle< YieldTermStructure > ÷nd) const override |

| Public Member Functions inherited from EquityIndex2 | |

| EquityIndex2 (const std::string &familyName, const Calendar &fixingCalendar, const Currency ¤cy, const Handle< Quote > spotQuote=Handle< Quote >(), const Handle< YieldTermStructure > &rate=Handle< YieldTermStructure >(), const Handle< YieldTermStructure > ÷nd=Handle< YieldTermStructure >()) | |

| std::string | name () const override |

| Currency | currency () const |

| Calendar | fixingCalendar () const override |

| bool | isValidFixingDate (const Date &fixingDate) const override |

| Real | fixing (const Date &fixingDate, bool forecastTodaysFixing=false) const override |

| Real | fixing (const Date &fixingDate, bool forecastTodaysFixing, bool incDividend) const |

| Real | dividendsBetweenDates (const Date &startDate, const Date &endDate) const |

| void | update () override |

| std::string | familyName () const |

| const Handle< Quote > & | equitySpot () const |

| const Handle< YieldTermStructure > & | equityForecastCurve () const |

| const Handle< YieldTermStructure > & | equityDividendCurve () const |

| virtual Real | forecastFixing (const Date &fixingDate) const |

| virtual Real | forecastFixing (const Time &fixingTime) const override |

| returns the fixing at the given time More... | |

| virtual Real | forecastFixing (const Date &fixingDate, bool incDividend) const |

| virtual Real | forecastFixing (const Time &fixingTime, bool incDividend) const |

| Public Member Functions inherited from EqFxIndexBase | |

| virtual | ~EqFxIndexBase () |

| virtual Real | forecastFixing (const Time &fixingTime) const =0 |

| returns the fixing at the given time More... | |

| virtual Real | pastFixing (const Date &fixingDate) const =0 |

| returns a past fixing at the given date More... | |

Private Member Functions | |

| void | performCalculations () const override |

Private Attributes | |

| QuantLib::ext::shared_ptr< QuantExt::EquityIndex2 > | source_ |

| QuantLib::ext::shared_ptr< FxIndex > | fxIndex_ |

| Date | dividendCutoffDate_ |

| std::set< Dividend > | dividendFixings_ |

Additional Inherited Members | |

| Protected Attributes inherited from EquityIndex2 | |

| std::string | familyName_ |

| Currency | currency_ |

| const Handle< YieldTermStructure > | rate_ |

| const Handle< YieldTermStructure > | dividend_ |

| std::string | name_ |

| const Handle< Quote > | spotQuote_ |

Definition at line 34 of file compoequityindex.hpp.

| CompoEquityIndex | ( | const QuantLib::ext::shared_ptr< QuantExt::EquityIndex2 > & | source, |

| const QuantLib::ext::shared_ptr< FxIndex > & | fxIndex, | ||

| const Date & | dividendCutoffDate = Date() |

||

| ) |

Definition at line 27 of file compoequityindex.cpp.

| QuantLib::ext::shared_ptr< QuantExt::EquityIndex2 > source | ( | ) | const |

Definition at line 42 of file compoequityindex.cpp.

stores the historical dividend at the given date

the date passed as arguments must be the actual calendar date of the dividend.

Reimplemented from EquityIndex2.

Definition at line 44 of file compoequityindex.cpp.

|

overridevirtual |

Reimplemented from EquityIndex2.

Definition at line 64 of file compoequityindex.cpp.

|

overridevirtual |

returns a past fixing at the given date

the date passed as arguments must be the actual calendar date of the fixing; no settlement days must be used.

Reimplemented from EquityIndex2.

Definition at line 69 of file compoequityindex.cpp.

|

overridevirtual |

Reimplemented from EquityIndex2.

Definition at line 73 of file compoequityindex.cpp.

|

overrideprivate |

Definition at line 53 of file compoequityindex.cpp.

|

private |

Definition at line 53 of file compoequityindex.hpp.

|

private |

Definition at line 54 of file compoequityindex.hpp.

|

private |

Definition at line 55 of file compoequityindex.hpp.

|

mutableprivate |

Definition at line 57 of file compoequityindex.hpp.