Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

COM Schwartz parametrization. More...

#include <qle/models/commodityschwartzparametrization.hpp>

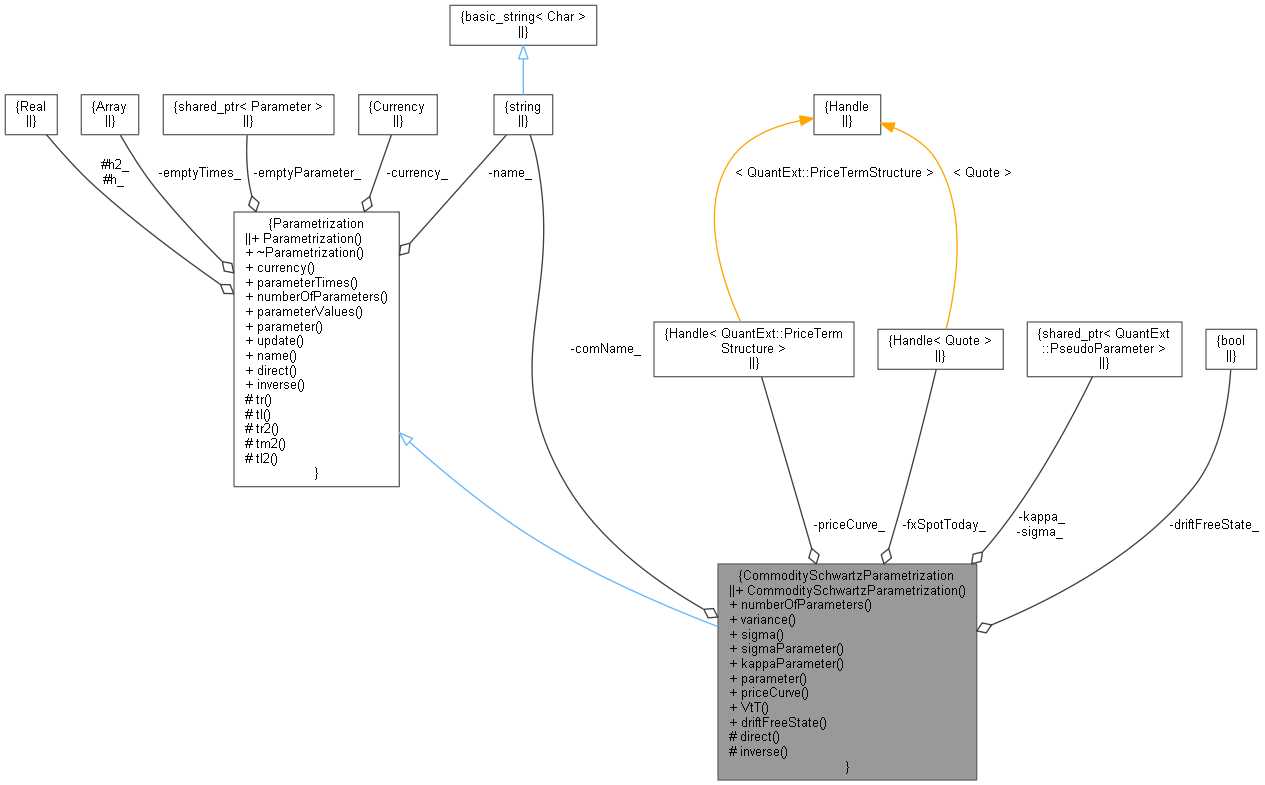

Inheritance diagram for CommoditySchwartzParametrization: Collaboration diagram for CommoditySchwartzParametrization:

Inheritance diagram for CommoditySchwartzParametrization: Collaboration diagram for CommoditySchwartzParametrization:Public Member Functions | |

| CommoditySchwartzParametrization (const Currency ¤cy, const std::string &name, const Handle< QuantExt::PriceTermStructure > &priceCurve, const Handle< Quote > &fxSpotToday, const Real sigma, const Real kappa, bool driftFreeState=false) | |

| Size | numberOfParameters () const override |

| Real | variance (const Time t) const |

| State variable variance on [0, t]. More... | |

| Real | sigma (const Time t) const |

| State variable Y's diffusion at time t: sigma * exp(kappa * t) More... | |

| Real | sigmaParameter () const |

| Inspector for the current value of model parameter sigma (direct) More... | |

| Real | kappaParameter () const |

| Inspector for the current value of model parameter kappa (direct) More... | |

| const QuantLib::ext::shared_ptr< Parameter > | parameter (const Size) const override |

| Inspector for current value of the model parameter vector (inverse values) More... | |

| Handle< QuantExt::PriceTermStructure > | priceCurve () |

| Inspector for today's price curve. More... | |

| Real | VtT (Real t, Real T) |

| Variance V(t,T) used in the computation of F(t,T) More... | |

| bool | driftFreeState () const |

| Public Member Functions inherited from Parametrization | |

| Parametrization (const Currency ¤cy, const std::string &name="") | |

| virtual | ~Parametrization () |

| virtual const Currency & | currency () const |

| virtual const Array & | parameterTimes (const Size) const |

| virtual Size | numberOfParameters () const |

| virtual Array | parameterValues (const Size) const |

| virtual const QuantLib::ext::shared_ptr< Parameter > | parameter (const Size) const |

| virtual void | update () const |

| const std::string & | name () const |

| virtual Real | direct (const Size, const Real x) const |

| virtual Real | inverse (const Size, const Real y) const |

Protected Member Functions | |

| Real | direct (const Size i, const Real x) const override |

| Real | inverse (const Size i, const Real y) const override |

| Protected Member Functions inherited from Parametrization | |

| Time | tr (const Time t) const |

| Time | tl (const Time t) const |

| Time | tr2 (const Time t) const |

| Time | tm2 (const Time t) const |

| Time | tl2 (const Time t) const |

Private Attributes | |

| const Handle< QuantExt::PriceTermStructure > | priceCurve_ |

| const Handle< Quote > | fxSpotToday_ |

| std::string | comName_ |

| const QuantLib::ext::shared_ptr< PseudoParameter > | sigma_ |

| const QuantLib::ext::shared_ptr< PseudoParameter > | kappa_ |

| bool | driftFreeState_ |

Additional Inherited Members | |

| Protected Attributes inherited from Parametrization | |

| const Real | h_ |

| const Real | h2_ |

COM Schwartz parametrization.

COM parametrization for the Schwartz (1997) mean-reverting one-factor model with log-normal forward price dynamics and forward volatility sigma * exp(-kappa*(T-t)): dF(t,T) / F(t,T) = sigma * exp(-kappa * (T-t)) * dW

The model can be propagated in terms of an artificial spot price process of the form S(t) = A(t) * exp(B(t) * X(t)) where

dX(t) = -kappa * X(t) * dt + sigma * dW(t) X(t) - X(s) = -X(s) * (1 - exp(-kappa*(t-s)) + int_s^t sigma * exp(-kappa*(t-u)) dW(u) E[X(t)|s] = X(s) * exp(-kappa*(t-s)) Var[X(t)-X(s)|s] = sigma^2 * (1 - exp(-2*kappa*(t-s))) / (2*kappa)

The stochastic future price curve in terms of X(t) is F(t,T) = F(0,T) * exp( X(t) * exp(-kappa*(T-t) - 1/2 * (V(0,T) - V(t,T)) with V(t,T) = sigma^2 * (1 - exp(-2*kappa*(T-t))) / (2*kappa) and Var[ln F(T,T)] = VaR[X(T)]

Instead of state variable X we can use Y(t) = exp(kappa * t) * X(t) with drift-free dY(t) = sigma * exp(kappa * t) * dW Y(t) = int_0^t sigma * exp(kappa * s) * dW(s) Var[Y(t)] = sigma^2 * (exp(2*kappa*t) - 1) / (2*kappa) Var[Y(t)-Y(s)|s] = int_s^t sigma * exp(kappa * u) * dW(u) = Var[Y(t)] - Var[Y(s)] The stochastic future price curve in terms of Y(t) is F(t,T) = F(0,t) * exp( Y(t) * exp(-kappa*T) - 1/2 * (V(0,T) - V(t,T))

Definition at line 64 of file commodityschwartzparametrization.hpp.

| CommoditySchwartzParametrization | ( | const Currency & | currency, |

| const std::string & | name, | ||

| const Handle< QuantExt::PriceTermStructure > & | priceCurve, | ||

| const Handle< Quote > & | fxSpotToday, | ||

| const Real | sigma, | ||

| const Real | kappa, | ||

| bool | driftFreeState = false |

||

| ) |

The currency refers to the commodity currency, the fx spot is as of today (i.e. the discounted spot)

Definition at line 24 of file commodityschwartzparametrization.cpp.

Here is the call graph for this function:

|

overridevirtual |

the number of parameters in this parametrization

Reimplemented from Parametrization.

Definition at line 73 of file commodityschwartzparametrization.hpp.

| Real variance | ( | const Time | t | ) | const |

State variable variance on [0, t].

Definition at line 111 of file commodityschwartzparametrization.hpp.

Here is the call graph for this function:| Real sigma | ( | const Time | t | ) | const |

State variable Y's diffusion at time t: sigma * exp(kappa * t)

Definition at line 122 of file commodityschwartzparametrization.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| Real sigmaParameter | ( | ) | const |

Inspector for the current value of model parameter sigma (direct)

Definition at line 131 of file commodityschwartzparametrization.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| Real kappaParameter | ( | ) | const |

Inspector for the current value of model parameter kappa (direct)

Definition at line 135 of file commodityschwartzparametrization.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

overridevirtual |

Inspector for current value of the model parameter vector (inverse values)

Reimplemented from Parametrization.

Definition at line 139 of file commodityschwartzparametrization.hpp.

| Handle< QuantExt::PriceTermStructure > priceCurve | ( | ) |

Inspector for today's price curve.

Definition at line 85 of file commodityschwartzparametrization.hpp.

| Real VtT | ( | Real | t, |

| Real | T | ||

| ) |

Variance V(t,T) used in the computation of F(t,T)

Definition at line 36 of file commodityschwartzparametrization.cpp.

Here is the call graph for this function:| bool driftFreeState | ( | ) | const |

Definition at line 89 of file commodityschwartzparametrization.hpp.

|

overrideprotectedvirtual |

transformations between raw and actual parameters

Reimplemented from Parametrization.

Definition at line 107 of file commodityschwartzparametrization.hpp.

Here is the caller graph for this function:

|

overrideprotectedvirtual |

Reimplemented from Parametrization.

Definition at line 109 of file commodityschwartzparametrization.hpp.

Here is the caller graph for this function:

|

private |

Definition at line 97 of file commodityschwartzparametrization.hpp.

|

private |

Definition at line 98 of file commodityschwartzparametrization.hpp.

|

private |

Definition at line 99 of file commodityschwartzparametrization.hpp.

|

private |

Definition at line 100 of file commodityschwartzparametrization.hpp.

|

private |

Definition at line 101 of file commodityschwartzparametrization.hpp.

|

private |

Definition at line 102 of file commodityschwartzparametrization.hpp.