Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

CDS option. More...

#include <qle/instruments/cdsoption.hpp>

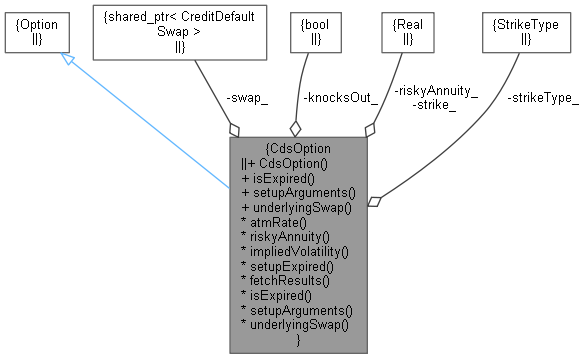

Inheritance diagram for CdsOption: Collaboration diagram for CdsOption:

Inheritance diagram for CdsOption: Collaboration diagram for CdsOption:Classes | |

| class | arguments |

| Arguments for CDS-option calculation More... | |

| class | engine |

| base class for swaption engines More... | |

| class | results |

Public Types | |

| enum | StrikeType { Price , Spread } |

Public Member Functions | |

| CdsOption (const QuantLib::ext::shared_ptr< CreditDefaultSwap > &swap, const QuantLib::ext::shared_ptr< Exercise > &exercise, bool knocksOut=true, const Real strike=Null< Real >(), const StrikeType strikeType=StrikeType::Spread) | |

Instrument interface | |

| bool | isExpired () const override |

| void | setupArguments (PricingEngine::arguments *) const override |

Inspectors | |

| const QuantLib::ext::shared_ptr< CreditDefaultSwap > & | underlyingSwap () const |

Calculations | |

| QuantLib::ext::shared_ptr< CreditDefaultSwap > | swap_ |

| bool | knocksOut_ |

| Real | strike_ |

| StrikeType | strikeType_ |

| Real | riskyAnnuity_ |

| Rate | atmRate () const |

| Real | riskyAnnuity () const |

| Volatility | impliedVolatility (Real price, const Handle< QuantLib::YieldTermStructure > &termStructure, const Handle< DefaultProbabilityTermStructure > &, Real recoveryRate, Real accuracy=1.e-4, Size maxEvaluations=100, Volatility minVol=1.0e-7, Volatility maxVol=4.0) const |

| void | setupExpired () const override |

| void | fetchResults (const PricingEngine::results *) const override |

CDS option.

The side of the swaption is set by choosing the side of the CDS. A receiver CDS option is a right to buy an underlying CDS selling protection and receiving a coupon. A payer CDS option is a right to buy an underlying CDS buying protection and paying coupon.

Definition at line 67 of file cdsoption.hpp.

| enum StrikeType |

| CdsOption | ( | const QuantLib::ext::shared_ptr< CreditDefaultSwap > & | swap, |

| const QuantLib::ext::shared_ptr< Exercise > & | exercise, | ||

| bool | knocksOut = true, |

||

| const Real | strike = Null<Real>(), |

||

| const StrikeType | strikeType = StrikeType::Spread |

||

| ) |

Definition at line 85 of file cdsoption.cpp.

|

override |

Definition at line 92 of file cdsoption.cpp.

Here is the caller graph for this function:

|

override |

Definition at line 99 of file cdsoption.cpp.

| const QuantLib::ext::shared_ptr< CreditDefaultSwap > & underlyingSwap | ( | ) | const |

Definition at line 86 of file cdsoption.hpp.

| Rate atmRate | ( | ) | const |

Definition at line 120 of file cdsoption.cpp.

| Real riskyAnnuity | ( | ) | const |

Definition at line 122 of file cdsoption.cpp.

Here is the caller graph for this function:| Volatility impliedVolatility | ( | Real | price, |

| const Handle< QuantLib::YieldTermStructure > & | termStructure, | ||

| const Handle< DefaultProbabilityTermStructure > & | , | ||

| Real | recoveryRate, | ||

| Real | accuracy = 1.e-4, |

||

| Size | maxEvaluations = 100, |

||

| Volatility | minVol = 1.0e-7, |

||

| Volatility | maxVol = 4.0 |

||

| ) | const |

Definition at line 128 of file cdsoption.cpp.

Here is the call graph for this function:

|

overrideprivate |

Definition at line 94 of file cdsoption.cpp.

|

overrideprivate |

Definition at line 113 of file cdsoption.cpp.

|

private |

Definition at line 99 of file cdsoption.hpp.

|

private |

Definition at line 100 of file cdsoption.hpp.

|

private |

Definition at line 101 of file cdsoption.hpp.

|

private |

Definition at line 102 of file cdsoption.hpp.

|

mutableprivate |

Definition at line 104 of file cdsoption.hpp.