Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <qle/instruments/cashsettledeuropeanoption.hpp>

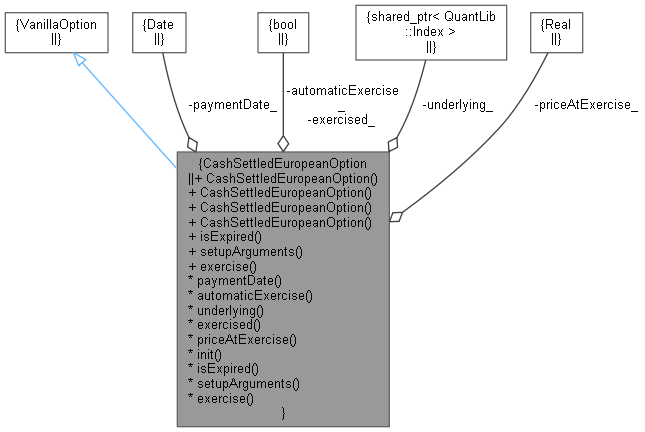

Inheritance diagram for CashSettledEuropeanOption: Collaboration diagram for CashSettledEuropeanOption:

Inheritance diagram for CashSettledEuropeanOption: Collaboration diagram for CashSettledEuropeanOption:Classes | |

| class | arguments |

| class | engine |

| Engine. More... | |

Public Member Functions | |

| CashSettledEuropeanOption (QuantLib::Option::Type type, QuantLib::Real strike, const QuantLib::Date &expiryDate, const QuantLib::Date &paymentDate, bool automaticExercise, const QuantLib::ext::shared_ptr< QuantLib::Index > &underlying=nullptr, bool exercised=false, QuantLib::Real priceAtExercise=QuantLib::Null< QuantLib::Real >()) | |

| Constructor for cash settled vanilla European option. More... | |

| CashSettledEuropeanOption (QuantLib::Option::Type type, QuantLib::Real strike, const QuantLib::Date &expiryDate, QuantLib::Natural paymentLag, const QuantLib::Calendar &paymentCalendar, QuantLib::BusinessDayConvention paymentConvention, bool automaticExercise, const QuantLib::ext::shared_ptr< QuantLib::Index > &underlying=nullptr, bool exercised=false, QuantLib::Real priceAtExercise=QuantLib::Null< QuantLib::Real >()) | |

| Constructor for cash settled vanilla European option. More... | |

| CashSettledEuropeanOption (QuantLib::Option::Type type, QuantLib::Real strike, QuantLib::Real cashPayoff, const QuantLib::Date &expiryDate, const QuantLib::Date &paymentDate, bool automaticExercise, const QuantLib::ext::shared_ptr< QuantLib::Index > &underlying=nullptr, bool exercised=false, QuantLib::Real priceAtExercise=QuantLib::Null< QuantLib::Real >()) | |

| Constructor for cash settled vanilla European option with digital payoff. More... | |

| CashSettledEuropeanOption (QuantLib::Option::Type type, QuantLib::Real strike, QuantLib::Real cashPayoff, const QuantLib::Date &expiryDate, QuantLib::Natural paymentLag, const QuantLib::Calendar &paymentCalendar, QuantLib::BusinessDayConvention paymentConvention, bool automaticExercise, const QuantLib::ext::shared_ptr< QuantLib::Index > &underlying=nullptr, bool exercised=false, QuantLib::Real priceAtExercise=QuantLib::Null< QuantLib::Real >()) | |

| Constructor for cash settled vanilla European option with digital payoff. More... | |

Instrument interface | |

| bool | isExpired () const override |

| Account for cash settled European options not being expired until payment is made. More... | |

| void | setupArguments (QuantLib::PricingEngine::arguments *args) const override |

| Set up the extra arguments. More... | |

| void | exercise (QuantLib::Real priceAtExercise) |

Mark option as manually exercised at the given priceAtExercise. More... | |

Inspectors | |

| QuantLib::Date | paymentDate_ |

| bool | automaticExercise_ |

| QuantLib::ext::shared_ptr< QuantLib::Index > | underlying_ |

| bool | exercised_ |

| QuantLib::Real | priceAtExercise_ |

| const QuantLib::Date & | paymentDate () const |

| bool | automaticExercise () const |

| const QuantLib::ext::shared_ptr< QuantLib::Index > & | underlying () const |

| bool | exercised () const |

| QuantLib::Real | priceAtExercise () const |

| void | init (bool exercised, QuantLib::Real priceAtExercise) |

| Shared initialisation. More... | |

Vanilla cash settled European options allowing for deferred payment and automatic exercise.

Definition at line 36 of file cashsettledeuropeanoption.hpp.

| CashSettledEuropeanOption | ( | QuantLib::Option::Type | type, |

| QuantLib::Real | strike, | ||

| const QuantLib::Date & | expiryDate, | ||

| const QuantLib::Date & | paymentDate, | ||

| bool | automaticExercise, | ||

| const QuantLib::ext::shared_ptr< QuantLib::Index > & | underlying = nullptr, |

||

| bool | exercised = false, |

||

| QuantLib::Real | priceAtExercise = QuantLib::Null< QuantLib::Real >() |

||

| ) |

Constructor for cash settled vanilla European option.

| CashSettledEuropeanOption | ( | QuantLib::Option::Type | type, |

| QuantLib::Real | strike, | ||

| const QuantLib::Date & | expiryDate, | ||

| QuantLib::Natural | paymentLag, | ||

| const QuantLib::Calendar & | paymentCalendar, | ||

| QuantLib::BusinessDayConvention | paymentConvention, | ||

| bool | automaticExercise, | ||

| const QuantLib::ext::shared_ptr< QuantLib::Index > & | underlying = nullptr, |

||

| bool | exercised = false, |

||

| QuantLib::Real | priceAtExercise = QuantLib::Null< QuantLib::Real >() |

||

| ) |

Constructor for cash settled vanilla European option.

| CashSettledEuropeanOption | ( | QuantLib::Option::Type | type, |

| QuantLib::Real | strike, | ||

| QuantLib::Real | cashPayoff, | ||

| const QuantLib::Date & | expiryDate, | ||

| const QuantLib::Date & | paymentDate, | ||

| bool | automaticExercise, | ||

| const QuantLib::ext::shared_ptr< QuantLib::Index > & | underlying = nullptr, |

||

| bool | exercised = false, |

||

| QuantLib::Real | priceAtExercise = QuantLib::Null< QuantLib::Real >() |

||

| ) |

Constructor for cash settled vanilla European option with digital payoff.

| CashSettledEuropeanOption | ( | QuantLib::Option::Type | type, |

| QuantLib::Real | strike, | ||

| QuantLib::Real | cashPayoff, | ||

| const QuantLib::Date & | expiryDate, | ||

| QuantLib::Natural | paymentLag, | ||

| const QuantLib::Calendar & | paymentCalendar, | ||

| QuantLib::BusinessDayConvention | paymentConvention, | ||

| bool | automaticExercise, | ||

| const QuantLib::ext::shared_ptr< QuantLib::Index > & | underlying = nullptr, |

||

| bool | exercised = false, |

||

| QuantLib::Real | priceAtExercise = QuantLib::Null< QuantLib::Real >() |

||

| ) |

Constructor for cash settled vanilla European option with digital payoff.

|

override |

Account for cash settled European options not being expired until payment is made.

Definition at line 141 of file cashsettledeuropeanoption.cpp.

|

override |

Set up the extra arguments.

Definition at line 143 of file cashsettledeuropeanoption.cpp.

| void exercise | ( | QuantLib::Real | priceAtExercise | ) |

Mark option as manually exercised at the given priceAtExercise.

Definition at line 161 of file cashsettledeuropeanoption.cpp.

Here is the caller graph for this function:| const Date & paymentDate | ( | ) | const |

Definition at line 172 of file cashsettledeuropeanoption.cpp.

| bool automaticExercise | ( | ) | const |

Definition at line 174 of file cashsettledeuropeanoption.cpp.

| const QuantLib::ext::shared_ptr< Index > & underlying | ( | ) | const |

Definition at line 176 of file cashsettledeuropeanoption.cpp.

| bool exercised | ( | ) | const |

Definition at line 178 of file cashsettledeuropeanoption.cpp.

| Real priceAtExercise | ( | ) | const |

Definition at line 180 of file cashsettledeuropeanoption.cpp.

|

private |

Shared initialisation.

Definition at line 133 of file cashsettledeuropeanoption.cpp.

|

private |

Definition at line 91 of file cashsettledeuropeanoption.hpp.

|

private |

Definition at line 92 of file cashsettledeuropeanoption.hpp.

|

private |

Definition at line 93 of file cashsettledeuropeanoption.hpp.

|

private |

Definition at line 94 of file cashsettledeuropeanoption.hpp.

|

private |

Definition at line 95 of file cashsettledeuropeanoption.hpp.