Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Cap/floor smile volatility surface sparse. More...

#include <qle/termstructures/capfloortermvolsurfacesparse.hpp>

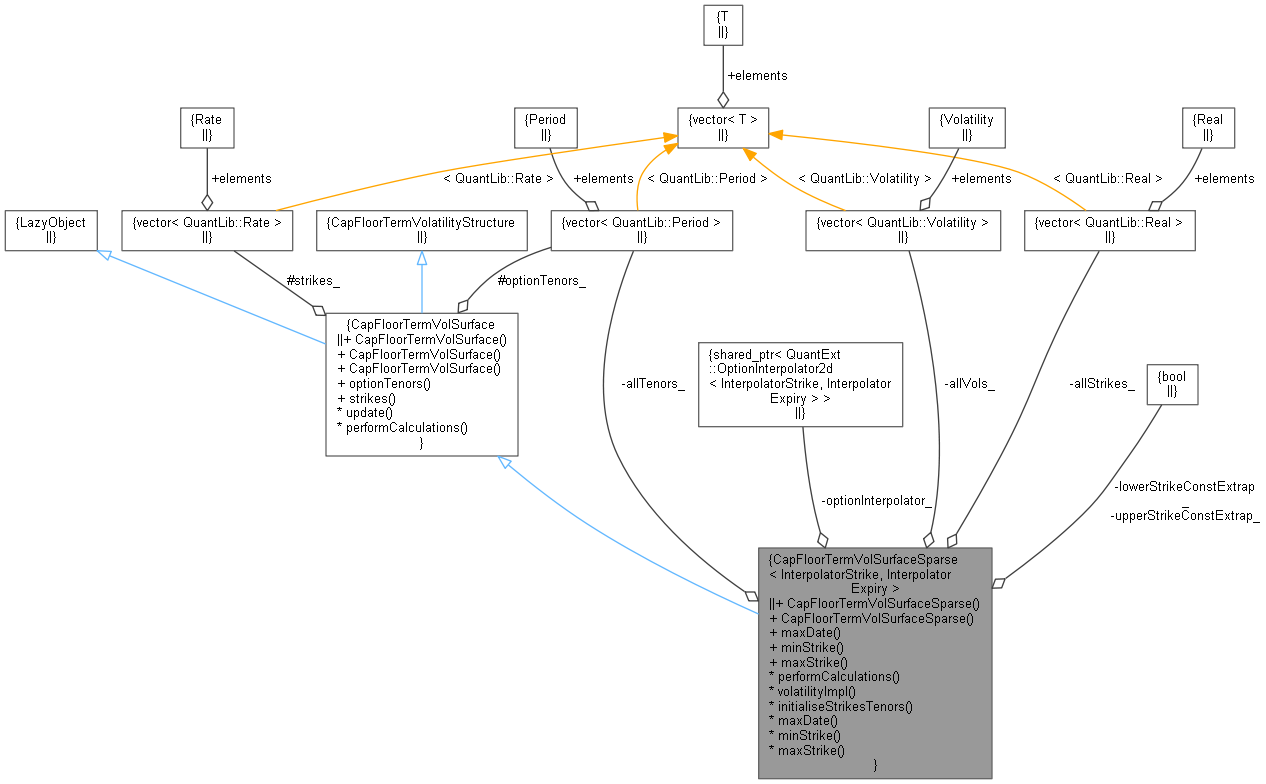

Inheritance diagram for CapFloorTermVolSurfaceSparse< InterpolatorStrike, InterpolatorExpiry >: Collaboration diagram for CapFloorTermVolSurfaceSparse< InterpolatorStrike, InterpolatorExpiry >:

Inheritance diagram for CapFloorTermVolSurfaceSparse< InterpolatorStrike, InterpolatorExpiry >: Collaboration diagram for CapFloorTermVolSurfaceSparse< InterpolatorStrike, InterpolatorExpiry >:Public Member Functions | |

| CapFloorTermVolSurfaceSparse (const QuantLib::Date &referenceDate, const QuantLib::Calendar &calendar, const QuantLib::BusinessDayConvention &bdc, const QuantLib::DayCounter &dc, const std::vector< QuantLib::Period > &tenors, const std::vector< QuantLib::Real > &strikes, const std::vector< QuantLib::Volatility > &volatilities, bool lowerStrikeConstExtrap=true, bool upperStrikeConstExtrap=true, bool timeFlatExtrapolation=false) | |

| fixed reference date, fixed market data More... | |

| CapFloorTermVolSurfaceSparse (QuantLib::Natural settlementDays, const QuantLib::Calendar &calendar, const QuantLib::BusinessDayConvention &bdc, const QuantLib::DayCounter &dc, const std::vector< QuantLib::Period > &tenors, const std::vector< QuantLib::Real > &strikes, const std::vector< QuantLib::Volatility > &volatilities, bool lowerStrikeConstExtrap=true, bool upperStrikeConstExtrap=true, bool timeFlatExtrapolation=false) | |

| floating reference date, fixed market data More... | |

TermStructure interface | |

| QuantLib::Date | maxDate () const override |

VolatilityTermStructure interface | |

| QuantLib::Real | minStrike () const override |

| QuantLib::Real | maxStrike () const override |

| Public Member Functions inherited from CapFloorTermVolSurface | |

| CapFloorTermVolSurface (QuantLib::BusinessDayConvention bdc, const QuantLib::DayCounter &dc=QuantLib::DayCounter(), std::vector< QuantLib::Period > optionTenors={}, std::vector< QuantLib::Rate > strikes={}) | |

| default constructor More... | |

| CapFloorTermVolSurface (const QuantLib::Date &referenceDate, const QuantLib::Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc=QuantLib::DayCounter(), std::vector< QuantLib::Period > optionTenors={}, std::vector< QuantLib::Rate > strikes={}) | |

| initialize with a fixed reference date More... | |

| CapFloorTermVolSurface (QuantLib::Natural settlementDays, const QuantLib::Calendar &cal, QuantLib::BusinessDayConvention bdc, const QuantLib::DayCounter &dc=QuantLib::DayCounter(), std::vector< QuantLib::Period > optionTenors={}, std::vector< QuantLib::Rate > strikes={}) | |

| calculate the reference date based on the global evaluation date More... | |

| const std::vector< QuantLib::Period > & | optionTenors () const |

| const std::vector< QuantLib::Rate > & | strikes () const |

| void | update () override |

| void | performCalculations () const override |

LazyObject interface | |

| QuantLib::ext::shared_ptr< OptionInterpolator2d< InterpolatorStrike, InterpolatorExpiry > > | optionInterpolator_ |

| std::vector< QuantLib::Period > | allTenors_ |

| std::vector< QuantLib::Real > | allStrikes_ |

| std::vector< QuantLib::Volatility > | allVols_ |

| bool | lowerStrikeConstExtrap_ |

| bool | upperStrikeConstExtrap_ |

| void | performCalculations () const override |

| QuantLib::Volatility | volatilityImpl (Time t, Rate strike) const override |

| void | initialiseStrikesTenors () |

Additional Inherited Members | |

| Protected Attributes inherited from CapFloorTermVolSurface | |

| std::vector< QuantLib::Period > | optionTenors_ |

| std::vector< QuantLib::Rate > | strikes_ |

Cap/floor smile volatility surface sparse.

This class provides the volatility for a given cap/floor interpolating a volatility surface whose elements are the market term volatilities of a set of caps/floors.

Definition at line 45 of file capfloortermvolsurfacesparse.hpp.

| CapFloorTermVolSurfaceSparse | ( | const QuantLib::Date & | referenceDate, |

| const QuantLib::Calendar & | calendar, | ||

| const QuantLib::BusinessDayConvention & | bdc, | ||

| const QuantLib::DayCounter & | dc, | ||

| const std::vector< QuantLib::Period > & | tenors, | ||

| const std::vector< QuantLib::Real > & | strikes, | ||

| const std::vector< QuantLib::Volatility > & | volatilities, | ||

| bool | lowerStrikeConstExtrap = true, |

||

| bool | upperStrikeConstExtrap = true, |

||

| bool | timeFlatExtrapolation = false |

||

| ) |

fixed reference date, fixed market data

Definition at line 90 of file capfloortermvolsurfacesparse.hpp.

Here is the call graph for this function:| CapFloorTermVolSurfaceSparse | ( | QuantLib::Natural | settlementDays, |

| const QuantLib::Calendar & | calendar, | ||

| const QuantLib::BusinessDayConvention & | bdc, | ||

| const QuantLib::DayCounter & | dc, | ||

| const std::vector< QuantLib::Period > & | tenors, | ||

| const std::vector< QuantLib::Real > & | strikes, | ||

| const std::vector< QuantLib::Volatility > & | volatilities, | ||

| bool | lowerStrikeConstExtrap = true, |

||

| bool | upperStrikeConstExtrap = true, |

||

| bool | timeFlatExtrapolation = false |

||

| ) |

floating reference date, fixed market data

Definition at line 101 of file capfloortermvolsurfacesparse.hpp.

Here is the call graph for this function:

|

override |

Definition at line 139 of file capfloortermvolsurfacesparse.hpp.

|

override |

Definition at line 144 of file capfloortermvolsurfacesparse.hpp.

|

override |

Definition at line 147 of file capfloortermvolsurfacesparse.hpp.

|

override |

Definition at line 155 of file capfloortermvolsurfacesparse.hpp.

|

overrideprotected |

Definition at line 150 of file capfloortermvolsurfacesparse.hpp.

|

private |

Definition at line 112 of file capfloortermvolsurfacesparse.hpp.

Here is the caller graph for this function:

|

mutableprivate |

Definition at line 79 of file capfloortermvolsurfacesparse.hpp.

|

private |

Definition at line 80 of file capfloortermvolsurfacesparse.hpp.

|

private |

Definition at line 81 of file capfloortermvolsurfacesparse.hpp.

|

private |

Definition at line 82 of file capfloortermvolsurfacesparse.hpp.

|

private |

Definition at line 83 of file capfloortermvolsurfacesparse.hpp.

|

private |

Definition at line 84 of file capfloortermvolsurfacesparse.hpp.