Bond option class.

More...

#include <qle/instruments/bondoption.hpp>

|

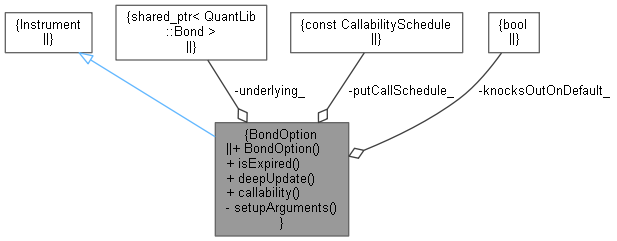

| | BondOption (const QuantLib::ext::shared_ptr< QuantLib::Bond > &underlying, const CallabilitySchedule &putCallSchedule, const bool knocksOutOnDefault=false) |

| |

| bool | isExpired () const override |

| |

| void | deepUpdate () override |

| |

| const CallabilitySchedule & | callability () const |

| |

Bond option class.

Definition at line 34 of file bondoption.hpp.

◆ BondOption()

| BondOption |

( |

const QuantLib::ext::shared_ptr< QuantLib::Bond > & |

underlying, |

|

|

const CallabilitySchedule & |

putCallSchedule, |

|

|

const bool |

knocksOutOnDefault = false |

|

) |

| |

Definition at line 36 of file bondoption.hpp.

const CallabilitySchedule putCallSchedule_

const bool knocksOutOnDefault_

const QuantLib::ext::shared_ptr< QuantLib::Bond > underlying_

◆ isExpired()

◆ deepUpdate()

◆ callability()

| const CallabilitySchedule & callability |

( |

| ) |

const |

◆ setupArguments()

| void setupArguments |

( |

PricingEngine::arguments * |

args | ) |

const |

|

overrideprivate |

Definition at line 25 of file bondoption.cpp.

25 {

26 BondOption::arguments* arguments = dynamic_cast<BondOption::arguments*>(args);

27 QL_REQUIRE(arguments != 0, "wrong argument type");

31}

◆ underlying_

| const QuantLib::ext::shared_ptr<QuantLib::Bond> underlying_ |

|

private |

◆ putCallSchedule_

| const CallabilitySchedule putCallSchedule_ |

|

private |

◆ knocksOutOnDefault_

| const bool knocksOutOnDefault_ |

|

private |

Inheritance diagram for BondOption:

Inheritance diagram for BondOption: