Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Pricing engine for cash settled European vanilla options using analytical formulae. More...

#include <qle/pricingengines/analyticcashsettledeuropeanengine.hpp>

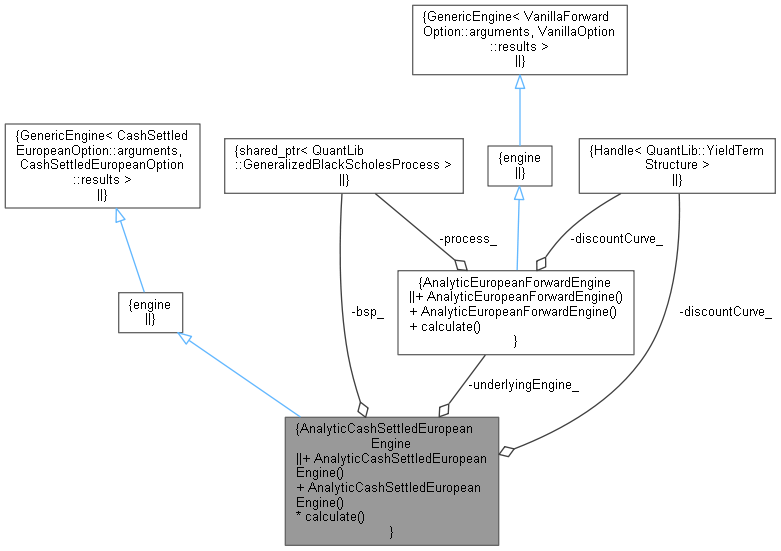

Inheritance diagram for AnalyticCashSettledEuropeanEngine: Collaboration diagram for AnalyticCashSettledEuropeanEngine:

Inheritance diagram for AnalyticCashSettledEuropeanEngine: Collaboration diagram for AnalyticCashSettledEuropeanEngine:Public Member Functions | |

| AnalyticCashSettledEuropeanEngine (const QuantLib::ext::shared_ptr< QuantLib::GeneralizedBlackScholesProcess > &bsp) | |

| AnalyticCashSettledEuropeanEngine (const QuantLib::ext::shared_ptr< QuantLib::GeneralizedBlackScholesProcess > &bsp, const QuantLib::Handle< QuantLib::YieldTermStructure > &discountCurve) | |

PricingEngine interface | |

| QuantExt::AnalyticEuropeanForwardEngine | underlyingEngine_ |

| Underlying engine that does the work. More... | |

| QuantLib::ext::shared_ptr< QuantLib::GeneralizedBlackScholesProcess > | bsp_ |

| Underlying process. More... | |

| QuantLib::Handle< QuantLib::YieldTermStructure > | discountCurve_ |

| Curve for discounting cashflows. More... | |

| void | calculate () const override |

Pricing engine for cash settled European vanilla options using analytical formulae.

Definition at line 36 of file analyticcashsettledeuropeanengine.hpp.

| AnalyticCashSettledEuropeanEngine | ( | const QuantLib::ext::shared_ptr< QuantLib::GeneralizedBlackScholesProcess > & | bsp | ) |

The risk-free rate in the given process bsp is used for both forecasting and discounting.

| AnalyticCashSettledEuropeanEngine | ( | const QuantLib::ext::shared_ptr< QuantLib::GeneralizedBlackScholesProcess > & | bsp, |

| const QuantLib::Handle< QuantLib::YieldTermStructure > & | discountCurve | ||

| ) |

As usual, the risk-free rate from the given process bsp is used for forecasting the forward price. The discountCurve is used for discounting.

|

override |

Definition at line 54 of file analyticcashsettledeuropeanengine.cpp.

|

mutableprivate |

Underlying engine that does the work.

Definition at line 55 of file analyticcashsettledeuropeanengine.hpp.

|

private |

Underlying process.

Definition at line 57 of file analyticcashsettledeuropeanengine.hpp.

|

private |

Curve for discounting cashflows.

Definition at line 59 of file analyticcashsettledeuropeanengine.hpp.