#include <ored/configuration/conventions.hpp>

|

| enum class | PublicationRoll { None

, OnPublicationDate

, AfterPublicationDate

} |

| | Rule for determining when inflation swaps roll to observing latest inflation index release. More...

|

| |

| enum class | Type {

Zero

, Deposit

, Future

, FRA

,

OIS

, Swap

, AverageOIS

, TenorBasisSwap

,

TenorBasisTwoSwap

, BMABasisSwap

, FX

, CrossCcyBasis

,

CrossCcyFixFloat

, CDS

, IborIndex

, OvernightIndex

,

SwapIndex

, ZeroInflationIndex

, InflationSwap

, SecuritySpread

,

CMSSpreadOption

, CommodityForward

, CommodityFuture

, FxOption

,

BondYield

} |

| | Supported convention types. More...

|

| |

|

| | InflationSwapConvention () |

| |

| | InflationSwapConvention (const string &id, const string &strFixCalendar, const string &strFixConvention, const string &strDayCounter, const string &strIndex, const string &strInterpolated, const string &strObservationLag, const string &strAdjustInfObsDates, const string &strInfCalendar, const string &strInfConvention, PublicationRoll publicationRoll=PublicationRoll::None, const QuantLib::ext::shared_ptr< ScheduleData > &publicationScheduleData=nullptr) |

| |

| const Calendar & | fixCalendar () const |

| |

| BusinessDayConvention | fixConvention () const |

| |

| const DayCounter & | dayCounter () const |

| |

| QuantLib::ext::shared_ptr< ZeroInflationIndex > | index () const |

| |

| const string & | indexName () const |

| |

| bool | interpolated () const |

| |

| Period | observationLag () const |

| |

| bool | adjustInfObsDates () const |

| |

| const Calendar & | infCalendar () const |

| |

| BusinessDayConvention | infConvention () const |

| |

| PublicationRoll | publicationRoll () const |

| |

| const Schedule & | publicationSchedule () const |

| |

| virtual void | fromXML (XMLNode *node) override |

| |

| virtual XMLNode * | toXML (XMLDocument &doc) const override |

| |

| virtual void | build () override |

| |

| virtual | ~Convention () |

| | Default destructor. More...

|

| |

| const string & | id () const |

| |

| Type | type () const |

| |

| virtual | ~XMLSerializable () |

| |

| virtual void | fromXML (XMLNode *node)=0 |

| |

| virtual XMLNode * | toXML (XMLDocument &doc) const =0 |

| |

| void | fromFile (const std::string &filename) |

| |

| void | toFile (const std::string &filename) const |

| |

| void | fromXMLString (const std::string &xml) |

| | Parse from XML string. More...

|

| |

| std::string | toXMLString () const |

| | Parse from XML string. More...

|

| |

Definition at line 1083 of file conventions.hpp.

◆ PublicationRoll

Rule for determining when inflation swaps roll to observing latest inflation index release.

| Enumerator |

|---|

| None | |

| OnPublicationDate | |

| AfterPublicationDate | |

Definition at line 1086 of file conventions.hpp.

◆ InflationSwapConvention() [1/2]

Definition at line 1235 of file conventions.cpp.

BusinessDayConvention infConvention_

PublicationRoll publicationRoll_

BusinessDayConvention fixConvention_

◆ InflationSwapConvention() [2/2]

| InflationSwapConvention |

( |

const string & |

id, |

|

|

const string & |

strFixCalendar, |

|

|

const string & |

strFixConvention, |

|

|

const string & |

strDayCounter, |

|

|

const string & |

strIndex, |

|

|

const string & |

strInterpolated, |

|

|

const string & |

strObservationLag, |

|

|

const string & |

strAdjustInfObsDates, |

|

|

const string & |

strInfCalendar, |

|

|

const string & |

strInfConvention, |

|

|

PublicationRoll |

publicationRoll = PublicationRoll::None, |

|

|

const QuantLib::ext::shared_ptr< ScheduleData > & |

publicationScheduleData = nullptr |

|

) |

| |

Definition at line 1239 of file conventions.cpp.

1252}

QuantLib::ext::shared_ptr< ScheduleData > publicationScheduleData_

string strAdjustInfObsDates_

PublicationRoll publicationRoll() const

string strObservationLag_

virtual void build() override

◆ fixCalendar()

| const Calendar & fixCalendar |

( |

| ) |

const |

◆ fixConvention()

| BusinessDayConvention fixConvention |

( |

| ) |

const |

◆ dayCounter()

| const DayCounter & dayCounter |

( |

| ) |

const |

◆ index()

Definition at line 1333 of file conventions.cpp.

1333 {

1335}

QuantLib::ext::shared_ptr< ZeroInflationIndex > parseZeroInflationIndex(const string &s, const Handle< ZeroInflationTermStructure > &h)

Convert std::string to QuantLib::ZeroInflationIndex.

◆ indexName()

| const string & indexName |

( |

| ) |

const |

◆ interpolated()

| bool interpolated |

( |

| ) |

const |

◆ observationLag()

| Period observationLag |

( |

| ) |

const |

◆ adjustInfObsDates()

| bool adjustInfObsDates |

( |

| ) |

const |

◆ infCalendar()

| const Calendar & infCalendar |

( |

| ) |

const |

◆ infConvention()

| BusinessDayConvention infConvention |

( |

| ) |

const |

◆ publicationRoll()

◆ publicationSchedule()

| const Schedule & publicationSchedule |

( |

| ) |

const |

◆ fromXML()

Implements XMLSerializable.

Definition at line 1272 of file conventions.cpp.

1272 {

1273

1277

1278

1288

1292 }

1293

1296 QL_REQUIRE(n,

"PublicationRoll is " <<

publicationRoll_ <<

" for " <<

id() <<

1297 " so expect non-empty PublicationSchedule.");

1300 }

1301

1303}

static void checkNode(XMLNode *n, const string &expectedName)

static string getChildValue(XMLNode *node, const string &name, bool mandatory=false, const string &defaultValue=string())

static XMLNode * getChildNode(XMLNode *n, const string &name="")

static string getNodeValue(XMLNode *node)

Get a node's value.

rapidxml::xml_node< char > XMLNode

InflationSwapConvention::PublicationRoll parseInflationSwapPublicationRoll(const string &s)

Convert text to InflationSwapConvention::PublicationRoll.

◆ toXML()

Implements XMLSerializable.

Definition at line 1305 of file conventions.cpp.

1305 {

1306

1307 XMLNode* node = doc.allocNode(

"InflationSwap");

1318

1322 << id() << " so expect PublicationSchedule.");

1323

1324

1328 }

1329

1330 return node;

1331}

static void setNodeName(XMLDocument &doc, XMLNode *node, const string &name)

static XMLNode * addChild(XMLDocument &doc, XMLNode *n, const string &name)

static void appendNode(XMLNode *parent, XMLNode *child)

std::string to_string(const LocationInfo &l)

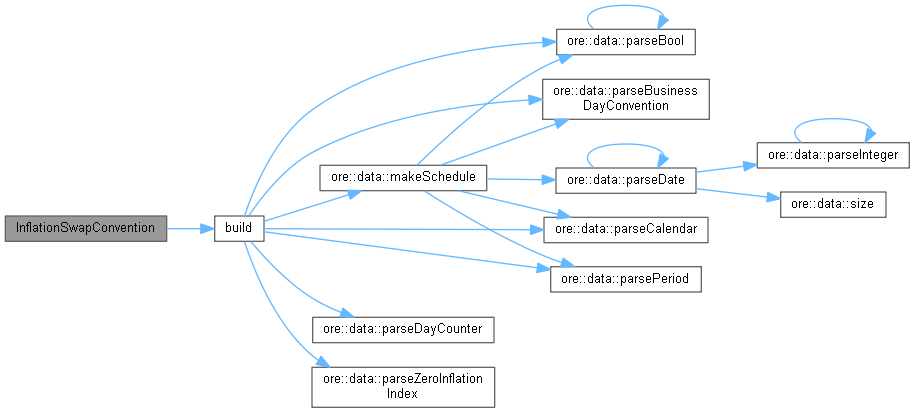

◆ build()

Implements Convention.

Definition at line 1254 of file conventions.cpp.

1254 {

1267 " so expect non-null publication schedule data.");

1269 }

1270}

QuantLib::ext::shared_ptr< ZeroInflationIndex > index_

Calendar parseCalendar(const string &s)

Convert text to QuantLib::Calendar.

BusinessDayConvention parseBusinessDayConvention(const string &s)

Convert text to QuantLib::BusinessDayConvention.

Period parsePeriod(const string &s)

Convert text to QuantLib::Period.

bool parseBool(const string &s)

Convert text to bool.

DayCounter parseDayCounter(const string &s)

Convert text to QuantLib::DayCounter.

Schedule makeSchedule(const ScheduleDates &data)

◆ fixCalendar_

◆ fixConvention_

| BusinessDayConvention fixConvention_ |

|

private |

◆ dayCounter_

◆ index_

◆ interpolated_

◆ observationLag_

◆ adjustInfObsDates_

◆ infCalendar_

◆ infConvention_

| BusinessDayConvention infConvention_ |

|

private |

◆ publicationSchedule_

| Schedule publicationSchedule_ |

|

private |

◆ strFixCalendar_

◆ strFixConvention_

◆ strDayCounter_

◆ strIndex_

◆ strInterpolated_

◆ strObservationLag_

| string strObservationLag_ |

|

private |

◆ strAdjustInfObsDates_

| string strAdjustInfObsDates_ |

|

private |

◆ strInfCalendar_

◆ strInfConvention_

◆ publicationRoll_

◆ publicationScheduleData_

| QuantLib::ext::shared_ptr<ScheduleData> publicationScheduleData_ |

|

private |

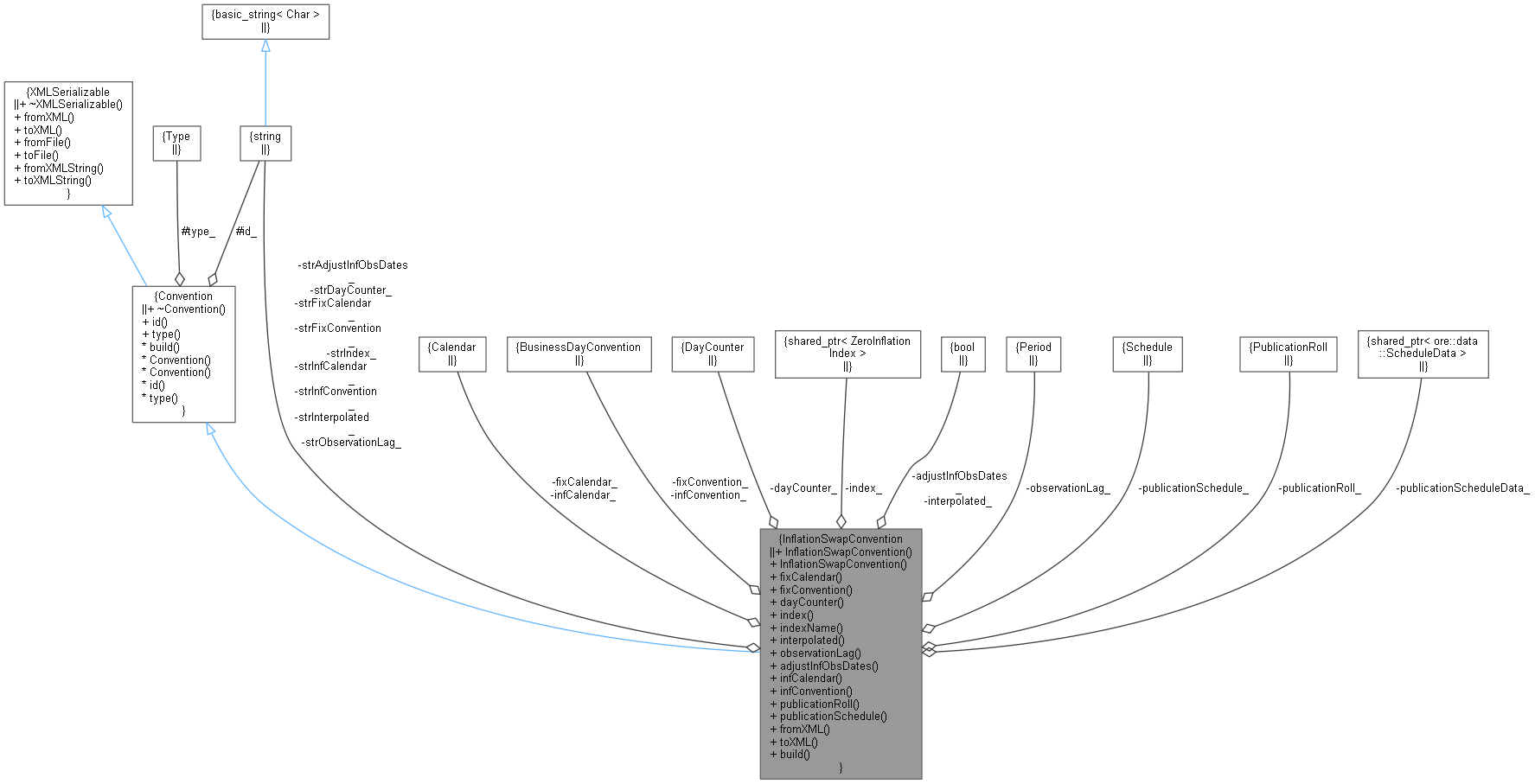

Inheritance diagram for InflationSwapConvention:

Inheritance diagram for InflationSwapConvention: