Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <ored/scripting/utilities.hpp>

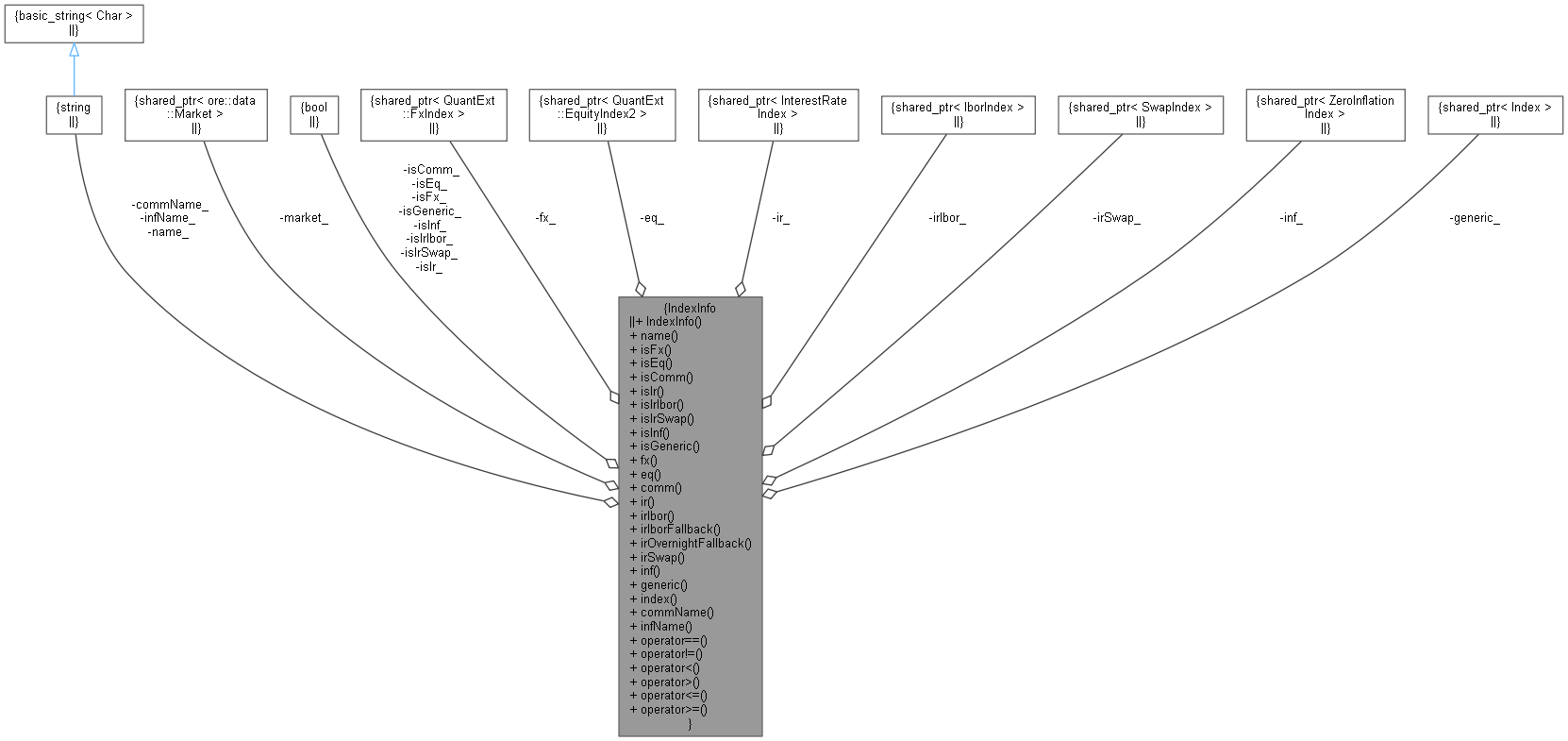

Collaboration diagram for IndexInfo:

Collaboration diagram for IndexInfo:Public Member Functions | |

| IndexInfo (const std::string &name, const QuantLib::ext::shared_ptr< Market > &market=nullptr) | |

| std::string | name () const |

| bool | isFx () const |

| bool | isEq () const |

| bool | isComm () const |

| bool | isIr () const |

| bool | isIrIbor () const |

| bool | isIrSwap () const |

| bool | isInf () const |

| bool | isGeneric () const |

| QuantLib::ext::shared_ptr< FxIndex > | fx () const |

| QuantLib::ext::shared_ptr< EquityIndex2 > | eq () const |

| QuantLib::ext::shared_ptr< QuantExt::CommodityIndex > | comm (const Date &obsDate=Date()) const |

| QuantLib::ext::shared_ptr< InterestRateIndex > | ir () const |

| QuantLib::ext::shared_ptr< IborIndex > | irIbor () const |

| QuantLib::ext::shared_ptr< FallbackIborIndex > | irIborFallback (const IborFallbackConfig &iborFallbackConfig, const Date &asof=QuantLib::Date::maxDate()) const |

| QuantLib::ext::shared_ptr< FallbackOvernightIndex > | irOvernightFallback (const IborFallbackConfig &iborFallbackConfig, const Date &asof=QuantLib::Date::maxDate()) const |

| QuantLib::ext::shared_ptr< SwapIndex > | irSwap () const |

| QuantLib::ext::shared_ptr< ZeroInflationIndex > | inf () const |

| QuantLib::ext::shared_ptr< Index > | generic () const |

| QuantLib::ext::shared_ptr< Index > | index (const Date &obsDate=Date()) const |

| std::string | commName () const |

| std::string | infName () const |

| bool | operator== (const IndexInfo &j) const |

| bool | operator!= (const IndexInfo &j) const |

| bool | operator< (const IndexInfo &j) const |

| bool | operator> (const IndexInfo &j) const |

| bool | operator<= (const IndexInfo &j) const |

| bool | operator>= (const IndexInfo &j) const |

Private Attributes | |

| std::string | name_ |

| QuantLib::ext::shared_ptr< Market > | market_ |

| bool | isFx_ |

| bool | isEq_ |

| bool | isComm_ |

| bool | isIr_ |

| bool | isInf_ |

| bool | isIrIbor_ |

| bool | isIrSwap_ |

| bool | isGeneric_ |

| QuantLib::ext::shared_ptr< FxIndex > | fx_ |

| QuantLib::ext::shared_ptr< EquityIndex2 > | eq_ |

| QuantLib::ext::shared_ptr< InterestRateIndex > | ir_ |

| QuantLib::ext::shared_ptr< IborIndex > | irIbor_ |

| QuantLib::ext::shared_ptr< SwapIndex > | irSwap_ |

| QuantLib::ext::shared_ptr< ZeroInflationIndex > | inf_ |

| QuantLib::ext::shared_ptr< Index > | generic_ |

| std::string | commName_ |

| std::string | infName_ |

Definition at line 93 of file utilities.hpp.

|

explicit |

Definition at line 388 of file utilities.cpp.

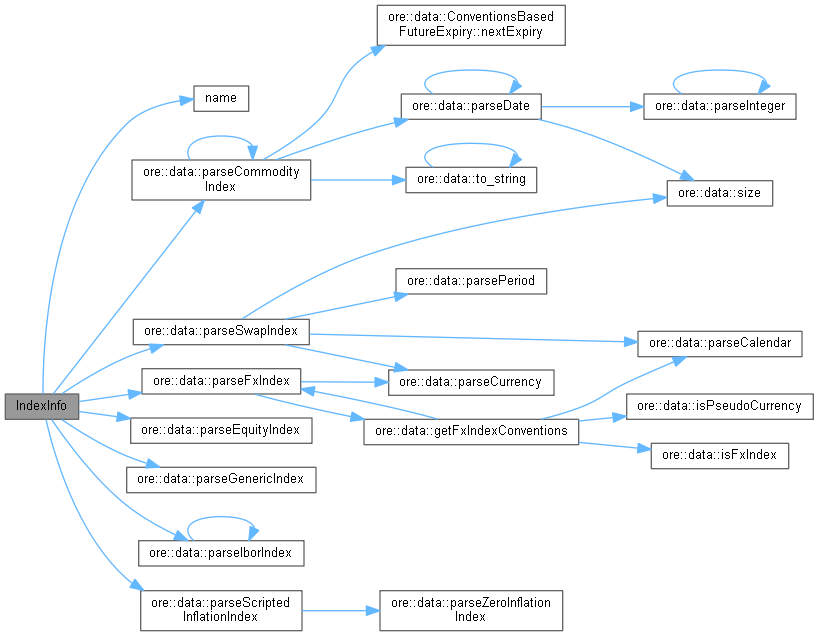

Here is the call graph for this function:| std::string name | ( | ) | const |

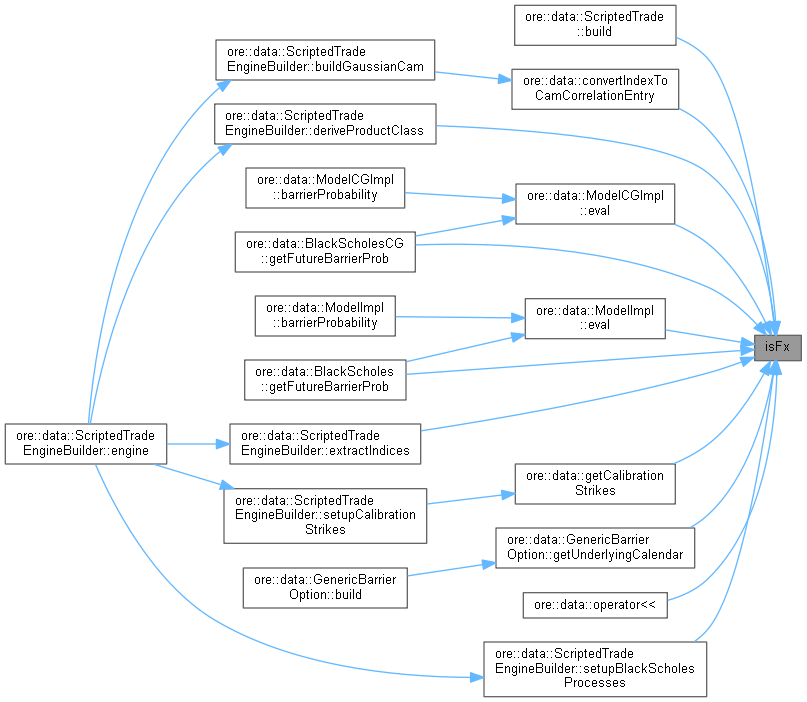

| bool isFx | ( | ) | const |

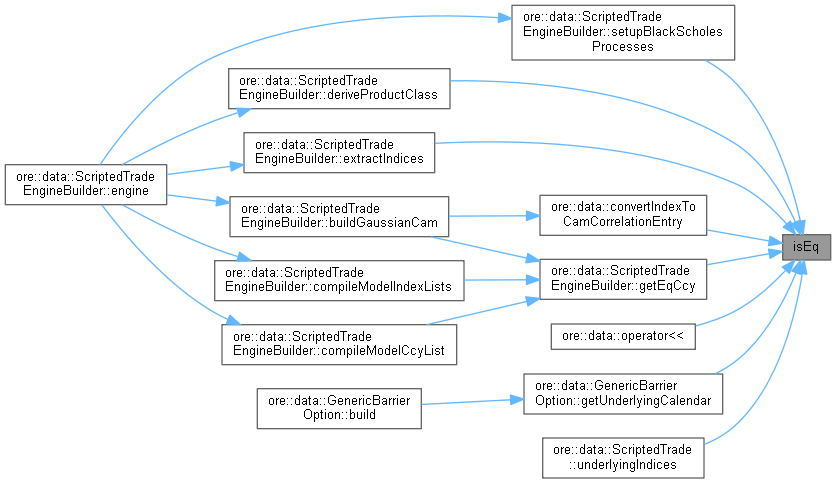

| bool isEq | ( | ) | const |

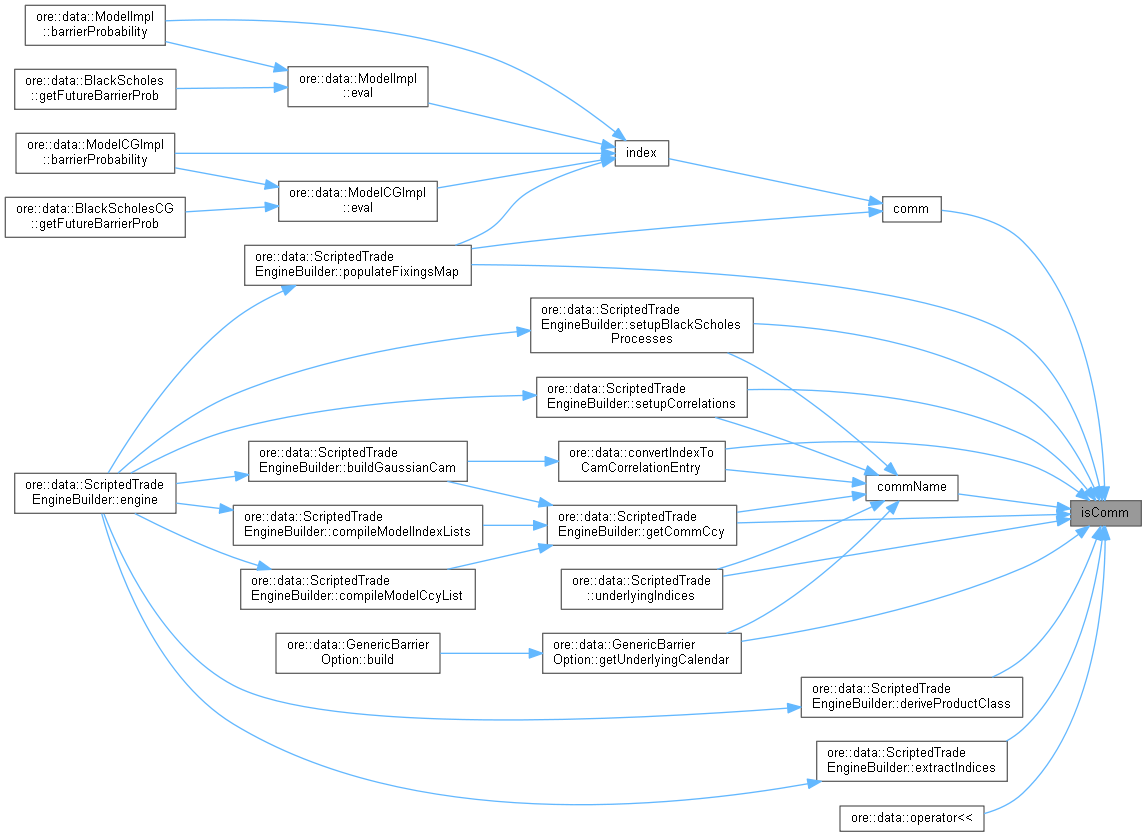

| bool isComm | ( | ) | const |

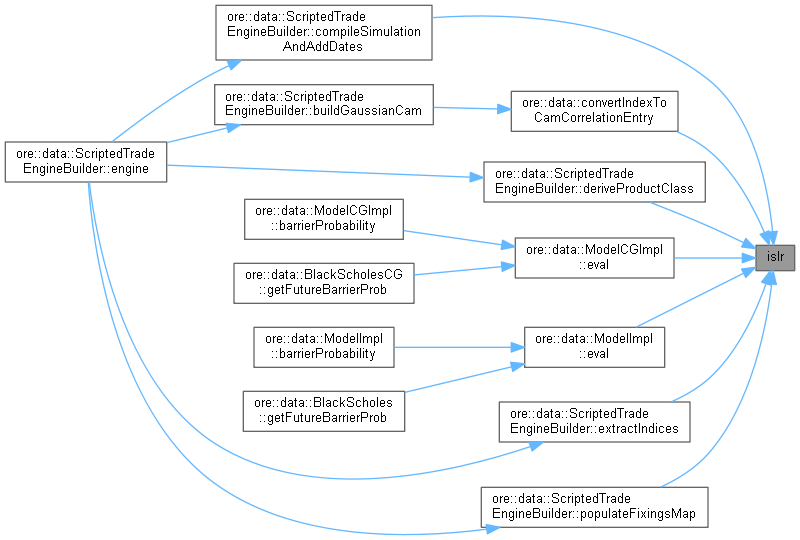

| bool isIr | ( | ) | const |

| bool isIrIbor | ( | ) | const |

| bool isIrSwap | ( | ) | const |

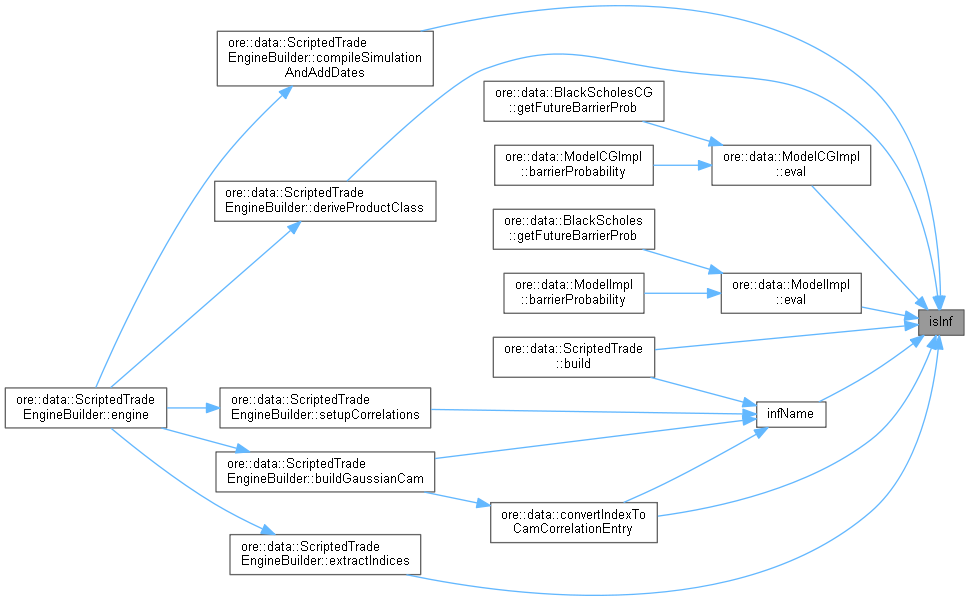

| bool isInf | ( | ) | const |

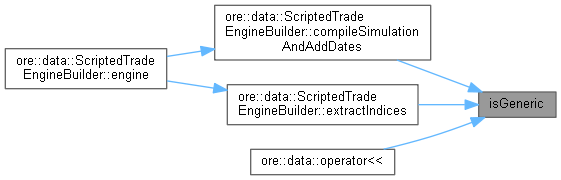

| bool isGeneric | ( | ) | const |

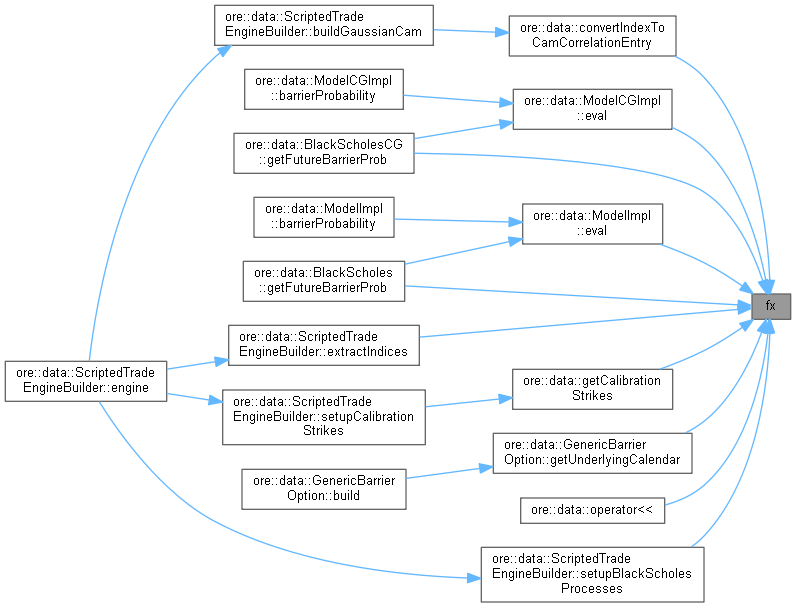

| QuantLib::ext::shared_ptr< FxIndex > fx | ( | ) | const |

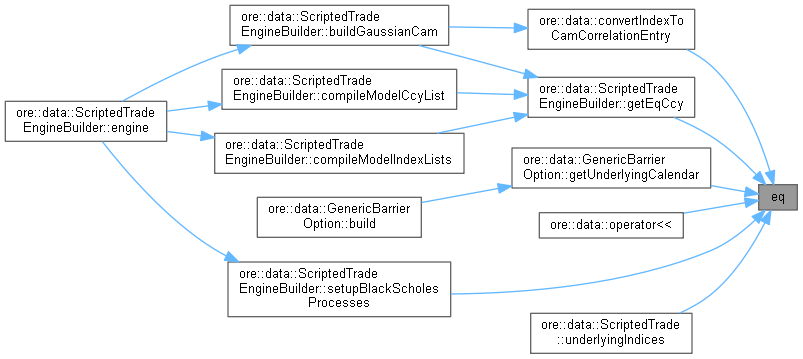

| QuantLib::ext::shared_ptr< EquityIndex2 > eq | ( | ) | const |

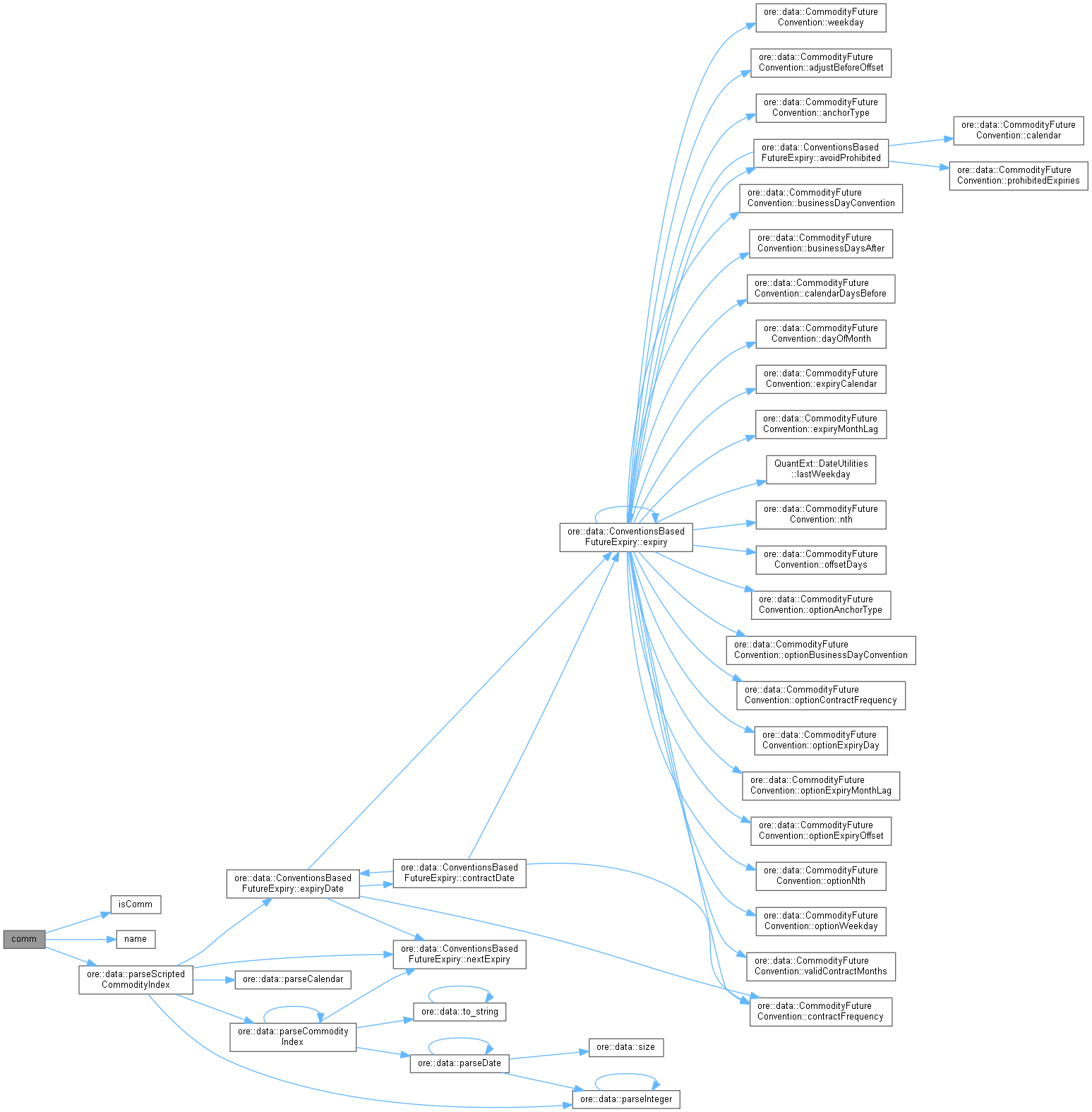

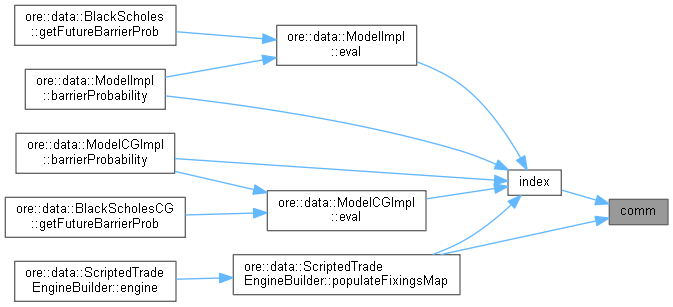

| QuantLib::ext::shared_ptr< CommodityIndex > comm | ( | const Date & | obsDate = Date() | ) | const |

Definition at line 467 of file utilities.cpp.

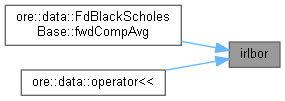

Here is the call graph for this function: Here is the caller graph for this function:| QuantLib::ext::shared_ptr< InterestRateIndex > ir | ( | ) | const |

| QuantLib::ext::shared_ptr< IborIndex > irIbor | ( | ) | const |

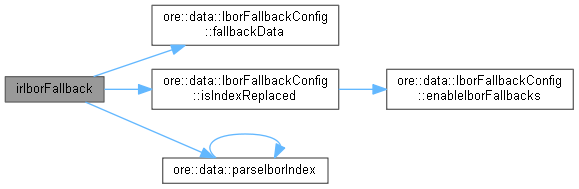

| QuantLib::ext::shared_ptr< FallbackIborIndex > irIborFallback | ( | const IborFallbackConfig & | iborFallbackConfig, |

| const Date & | asof = QuantLib::Date::maxDate() |

||

| ) | const |

Definition at line 501 of file utilities.cpp.

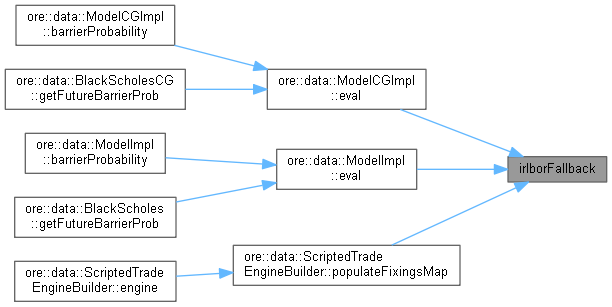

Here is the call graph for this function: Here is the caller graph for this function:| QuantLib::ext::shared_ptr< FallbackOvernightIndex > irOvernightFallback | ( | const IborFallbackConfig & | iborFallbackConfig, |

| const Date & | asof = QuantLib::Date::maxDate() |

||

| ) | const |

Definition at line 514 of file utilities.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| QuantLib::ext::shared_ptr< SwapIndex > irSwap | ( | ) | const |

| QuantLib::ext::shared_ptr< ZeroInflationIndex > inf | ( | ) | const |

| QuantLib::ext::shared_ptr< Index > generic | ( | ) | const |

| QuantLib::ext::shared_ptr< Index > index | ( | const Date & | obsDate = Date() | ) | const |

Definition at line 449 of file utilities.cpp.

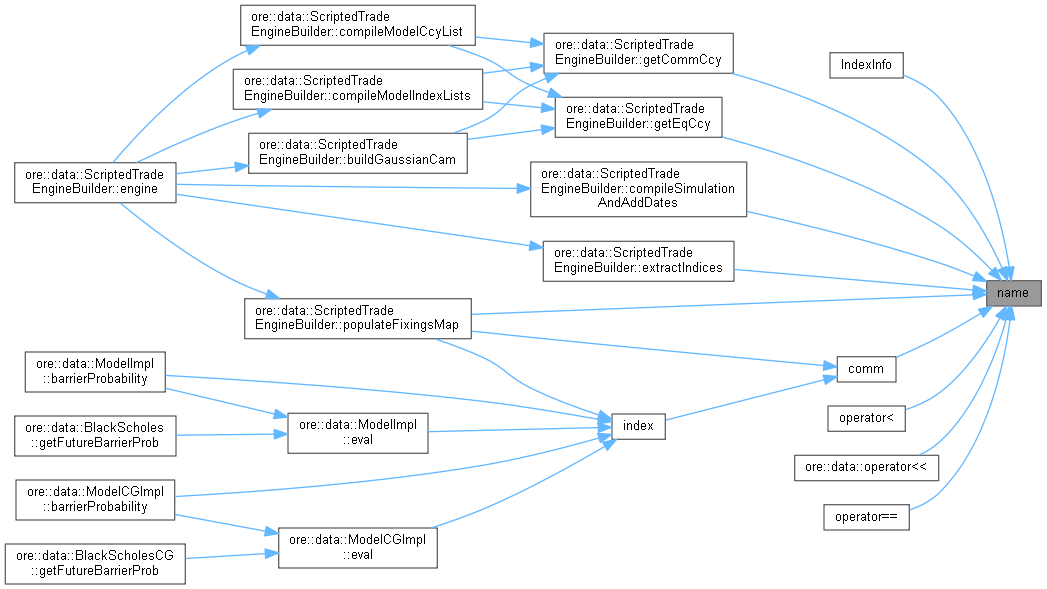

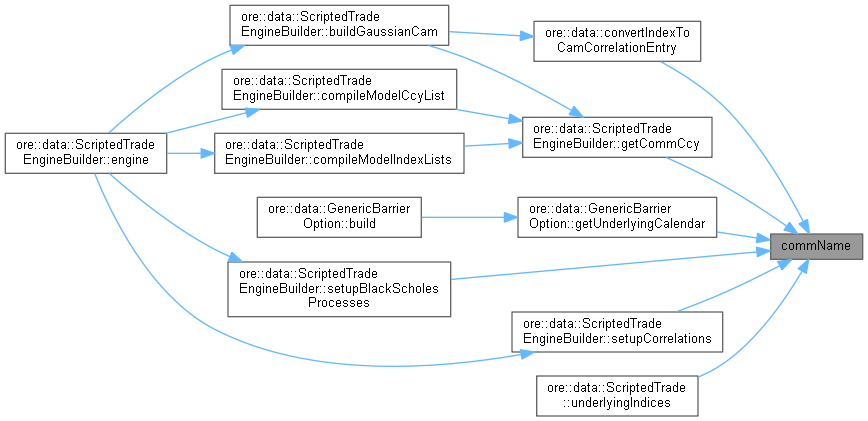

Here is the call graph for this function: Here is the caller graph for this function:| std::string commName | ( | ) | const |

Definition at line 474 of file utilities.cpp.

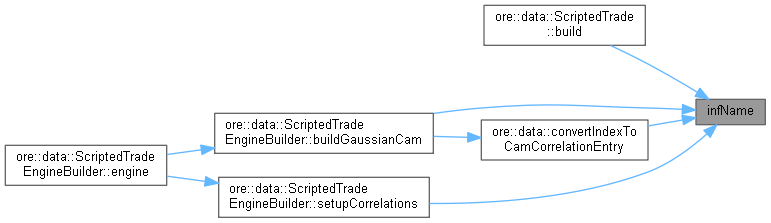

Here is the call graph for this function: Here is the caller graph for this function:| std::string infName | ( | ) | const |

Definition at line 479 of file utilities.cpp.

Here is the call graph for this function: Here is the caller graph for this function:Definition at line 134 of file utilities.hpp.

Definition at line 136 of file utilities.hpp.

Definition at line 137 of file utilities.hpp.

Definition at line 138 of file utilities.hpp.

|

private |

Definition at line 141 of file utilities.hpp.

|

private |

Definition at line 142 of file utilities.hpp.

|

private |

Definition at line 143 of file utilities.hpp.

|

private |

Definition at line 143 of file utilities.hpp.

|

private |

Definition at line 143 of file utilities.hpp.

|

private |

Definition at line 143 of file utilities.hpp.

|

private |

Definition at line 143 of file utilities.hpp.

|

private |

Definition at line 143 of file utilities.hpp.

|

private |

Definition at line 143 of file utilities.hpp.

|

private |

Definition at line 143 of file utilities.hpp.

|

private |

Definition at line 144 of file utilities.hpp.

|

private |

Definition at line 145 of file utilities.hpp.

|

private |

Definition at line 146 of file utilities.hpp.

|

private |

Definition at line 147 of file utilities.hpp.

|

private |

Definition at line 148 of file utilities.hpp.

|

private |

Definition at line 149 of file utilities.hpp.

|

private |

Definition at line 150 of file utilities.hpp.

|

private |

Definition at line 151 of file utilities.hpp.

|

private |

Definition at line 151 of file utilities.hpp.