36 {

37

38 LOG(

"FlexiSwap::build() for id \"" <<

id() <<

"\" called.");

39

40

45

46 QL_REQUIRE(

swap_.size() == 2,

"swap must have 2 legs");

47 QL_REQUIRE(swap_[0].currency() == swap_[1].currency(), "swap must be single currency");

48

49 string ccy_str =

swap_[0].currency();

51

52 Size fixedLegIndex, floatingLegIndex;

53 if (swap_[0].legType() == "Floating" && swap_[1].legType() == "Fixed") {

54 floatingLegIndex = 0;

55 fixedLegIndex = 1;

56 } else if (swap_[1].legType() == "Floating" && swap_[0].legType() == "Fixed") {

57 floatingLegIndex = 1;

58 fixedLegIndex = 0;

59 } else {

60 QL_FAIL("Invalid leg types " << swap_[0].legType() << " + " << swap_[1].legType());

61 }

62

63 QuantLib::ext::shared_ptr<FixedLegData> fixedLegData =

64 QuantLib::ext::dynamic_pointer_cast<FixedLegData>(swap_[fixedLegIndex].concreteLegData());

65 QuantLib::ext::shared_ptr<FloatingLegData> floatingLegData =

66 QuantLib::ext::dynamic_pointer_cast<FloatingLegData>(swap_[floatingLegIndex].concreteLegData());

67

68 QL_REQUIRE(fixedLegData != nullptr, "expected fixed leg data");

69 QL_REQUIRE(floatingLegData != nullptr, "expected floating leg data");

70

71 QuantLib::ext::shared_ptr<EngineBuilder> tmp = engineFactory->builder("FlexiSwap");

72 auto builder = QuantLib::ext::dynamic_pointer_cast<FlexiSwapBGSEngineBuilderBase>(tmp);

73 QL_REQUIRE(builder, "No Flexi-Swap Builder found for \"" << id() << "\"");

74

78 swap_[fixedLegIndex].notionals(), swap_[fixedLegIndex].notionalDates(),

fixedSchedule, 0.0);

80 swap_[floatingLegIndex].notionals(), swap_[floatingLegIndex].notionalDates(),

floatingSchedule, 0.0);

92 DayCounter fixedDayCounter =

parseDayCounter(swap_[fixedLegIndex].dayCounter());

93 Handle<IborIndex> index =

94 engineFactory->market()->iborIndex(floatingIndex_, builder->configuration(MarketContext::pricing));

95 DayCounter floatingDayCounter =

parseDayCounter(swap_[floatingLegIndex].dayCounter());

97 VanillaSwap::Type

type =

swap_[fixedLegIndex].isPayer() ? VanillaSwap::Payer : VanillaSwap::Receiver;

98

101

102

103

105 "can not have lower notional bounds and exercise dates / types / values specified at the same time");

106

107

108

110 lowerNotionalBounds =

112 DLOG(

"optionality is given by lower notional bounds");

113 }

114

115

116

117

118

119

120

122 DLOG(

"optionality is given by exercise dates, types, values");

123

124

125

126

127

129

130

131 Date previousExerciseDate = Null<Date>();

134 QL_REQUIRE(exerciseValues_[i] > 0.0 ||

close_enough(exerciseValues_[i], 0.0),

135 "exercise value #" << i << " (" << exerciseValues_[i] << ") must be non-negative");

136 QL_REQUIRE(i == 0 || previousExerciseDate < d, "exercise dates must be strictly increasing, got "

137 << QuantLib::io::iso_date(previousExerciseDate)

138 << " and " << QuantLib::io::iso_date(d) << " as #" << i

139 << " and #" << i + 1);

140 previousExerciseDate = d;

141

145 DLOG(

"exercise date "

146 << QuantLib::io::iso_date(d)

147 << " ignored since there is no whole fixed leg period with accrual start >= exercise date");

148 continue;

149 }

151 if (exerciseTypes_[i] == "ReductionUpToLowerBound") {

152 for (Size j = exerciseIdx; j < lowerNotionalBounds.size(); ++j) {

153 lowerNotionalBounds[j] = std::min(lowerNotionalBounds[j], exerciseValues_[i]);

154 }

155 } else if (exerciseTypes_[i] == "ReductionByAbsoluteAmount" ||

156 exerciseTypes_[i] == "ReductionUpToAbsoluteAmount") {

157

158

159

160 for (Size j = exerciseIdx; j < lowerNotionalBounds.size(); ++j) {

161 lowerNotionalBounds[j] = std::max(lowerNotionalBounds[j] - exerciseValues_[i], 0.0);

162 }

163 } else {

164 QL_FAIL("exercise type '" << exerciseTypes_[i]

165 << "' unknown, expected ReductionUpToLowerBound, ReductionByAbsoluteAmount, "

166 "ReductionUpToAbsoluteAmount");

167 }

168 }

169 }

170

171 DLOG(

"fixedPeriod#,notional,lowerNotionalBound,canBeReduced");

172 for (Size i = 0; i < lowerNotionalBounds.size(); ++i) {

173 DLOG(i <<

"," <<

fixedNominal.at(i) <<

"," << lowerNotionalBounds[i] <<

"," << std::boolalpha

175 }

176

177

178

180

181 auto flexiSwap = QuantLib::ext::make_shared<QuantExt::FlexiSwap>(

185

186 auto fixLeg = flexiSwap->leg(0);

187 auto fltLeg = flexiSwap->leg(1);

188

189

190

191 bool hasCapsFloors = false;

192 for (auto const& k : caps) {

193 if (k != Null<Real>())

194 hasCapsFloors = true;

195 }

196 for (auto const& k : floors) {

197 if (k != Null<Real>())

198 hasCapsFloors = true;

199 }

200 if (hasCapsFloors) {

201 QuantLib::ext::shared_ptr<EngineBuilder> cfBuilder = engineFactory->builder("CapFlooredIborLeg");

202 QL_REQUIRE(cfBuilder, "No builder found for CapFlooredIborLeg");

203 QuantLib::ext::shared_ptr<CapFlooredIborLegEngineBuilder> cappedFlooredIborBuilder =

204 QuantLib::ext::dynamic_pointer_cast<CapFlooredIborLegEngineBuilder>(cfBuilder);

205 QL_REQUIRE(cappedFlooredIborBuilder != nullptr, "expected CapFlooredIborLegEngineBuilder");

206 QuantLib::ext::shared_ptr<FloatingRateCouponPricer> couponPricer =

207 cappedFlooredIborBuilder->engine(IndexNameTranslator::instance().oreName(index->name()));

208 QuantLib::setCouponPricer(fltLeg, couponPricer);

209 }

210

211

212 std::vector<Date> expiryDates;

214 Date today = Settings::instance().evaluationDate();

215 Size legRatio = fltLeg.size() / fixLeg.size();

216 for (Size i = 0; i < fltLeg.size(); ++i) {

217 auto fltcpn = QuantLib::ext::dynamic_pointer_cast<FloatingRateCoupon>(fltLeg[i]);

218 if (fltcpn != nullptr && fltcpn->fixingDate() > today && i % legRatio == 0) {

219 expiryDates.push_back(fltcpn->fixingDate());

220 auto fixcpn = QuantLib::ext::dynamic_pointer_cast<FixedRateCoupon>(fixLeg[i / legRatio]);

221 QL_REQUIRE(fixcpn != nullptr, "FlexiSwap Builder: expected fixed rate coupon");

222 strikes.push_back(fixcpn->rate() - fltcpn->spread());

223 }

224 }

225

226

227

228 flexiSwap->setPricingEngine(

229 builder->engine(id(), "", index.empty() ? ccy_str : IndexNameTranslator::instance().oreName(index->name()),

230 expiryDates, flexiSwap->maturityDate(), strikes));

232

233

234 instrument_ = QuantLib::ext::make_shared<VanillaInstrument>(flexiSwap);

235

240 legs_ = {fixLeg, fltLeg};

244}

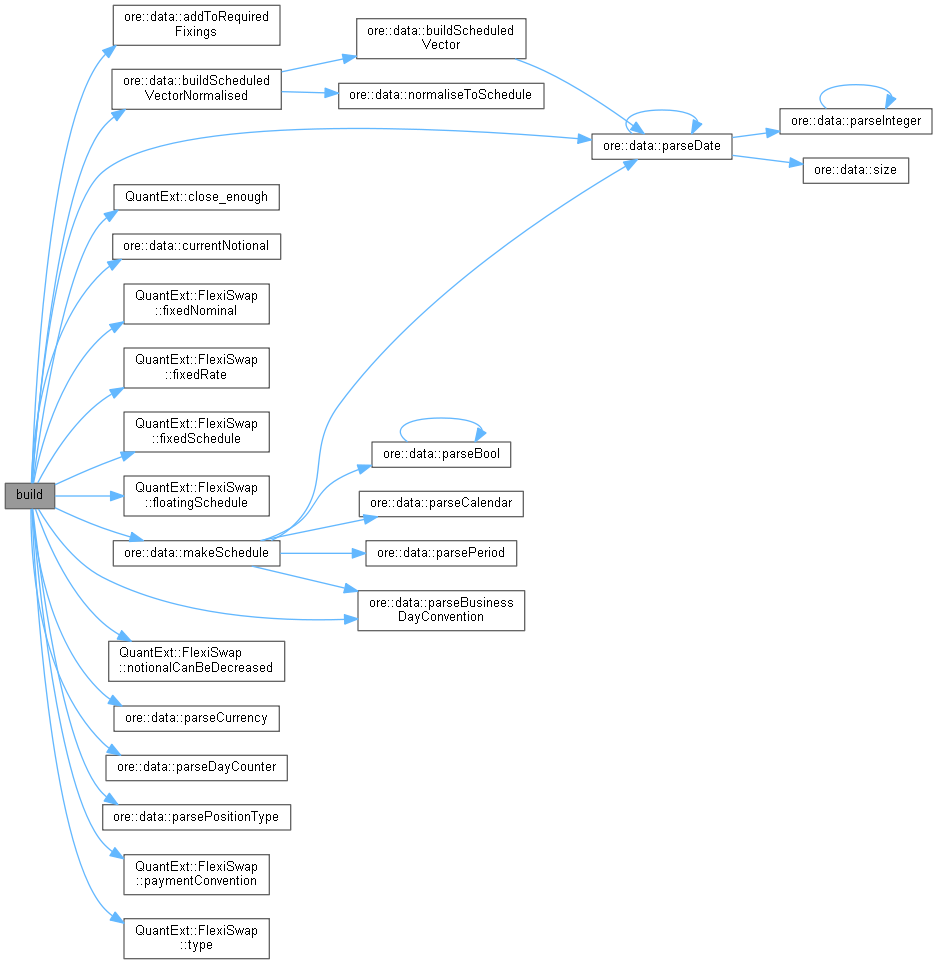

const std::vector< bool > & notionalCanBeDecreased() const

const std::vector< Real > & fixedNominal() const

BusinessDayConvention paymentConvention() const

const Schedule & fixedSchedule() const

const Schedule & floatingSchedule() const

VanillaSwap::Type type() const

const std::vector< Real > & fixedRate() const

std::string floatingIndex_

Store the name of the floating leg index.

const std::vector< double > & lowerNotionalBounds() const

const std::string & optionLongShort() const

std::vector< bool > legPayers_

std::vector< string > legCurrencies_

std::vector< QuantLib::Leg > legs_

void setSensitivityTemplate(const EngineBuilder &builder)

QuantLib::ext::shared_ptr< InstrumentWrapper > instrument_

std::map< std::string, boost::any > additionalData_

Date parseDate(const string &s)

Convert std::string to QuantLib::Date.

Currency parseCurrency(const string &s)

Convert text to QuantLib::Currency.

Position::Type parsePositionType(const std::string &s)

Convert text to QuantLib::Position::Type.

BusinessDayConvention parseBusinessDayConvention(const string &s)

Convert text to QuantLib::BusinessDayConvention.

DayCounter parseDayCounter(const string &s)

Convert text to QuantLib::DayCounter.

#define LOG(text)

Logging Macro (Level = Notice)

#define DLOG(text)

Logging Macro (Level = Debug)

Filter close_enough(const RandomVariable &x, const RandomVariable &y)

vector< T > buildScheduledVectorNormalised(const vector< T > &values, const vector< string > &dates, const Schedule &schedule, const T &defaultValue, const bool checkAllValuesAppearInResult=false)

Real currentNotional(const Leg &leg)

void addToRequiredFixings(const QuantLib::Leg &leg, const QuantLib::ext::shared_ptr< FixingDateGetter > &fixingDateGetter)

Schedule makeSchedule(const ScheduleDates &data)

Inheritance diagram for FlexiSwap:

Inheritance diagram for FlexiSwap: