Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <ored/utilities/currencyhedgedequityindexdecomposition.hpp>

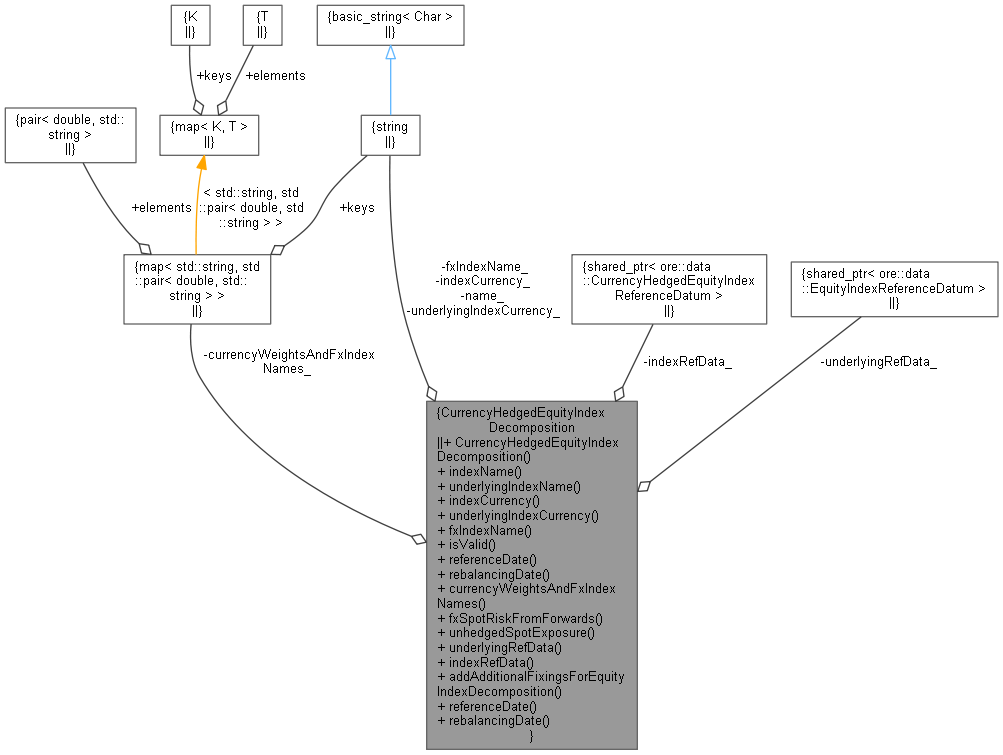

Collaboration diagram for CurrencyHedgedEquityIndexDecomposition:

Collaboration diagram for CurrencyHedgedEquityIndexDecomposition:Public Member Functions | |

| CurrencyHedgedEquityIndexDecomposition (const std::string indexName, const QuantLib::ext::shared_ptr< ore::data::CurrencyHedgedEquityIndexReferenceDatum > &indexRefData, const QuantLib::ext::shared_ptr< ore::data::EquityIndexReferenceDatum > underlyingRefData, const std::string &indexCurrency, const std::string &underlyingIndexCurrency, const std::string &fxIndexName, const std::map< std::string, std::pair< double, std::string > > ¤cyWeightsAndFxIndexNames) | |

| const std::string & | indexName () const |

| const std::string & | underlyingIndexName () const |

| const std::string & | indexCurrency () const |

| const std::string & | underlyingIndexCurrency () const |

| const std::string & | fxIndexName () const |

| bool | isValid () const |

| QuantLib::Date | referenceDate (const QuantLib::Date &asof) const |

| QuantLib::Date | rebalancingDate (const QuantLib::Date &asof) const |

| const std::map< std::string, std::pair< double, std::string > > & | currencyWeightsAndFxIndexNames () const |

| std::map< std::string, double > | fxSpotRiskFromForwards (const double quantity, const QuantLib::Date &asof, const QuantLib::ext::shared_ptr< ore::data::Market > &todaysMarket, const double shiftsize) const |

| double | unhedgedSpotExposure (double hedgedExposure, const double quantity, const QuantLib::Date &asof, const QuantLib::ext::shared_ptr< ore::data::Market > &todaysMarket) const |

| QuantLib::ext::shared_ptr< ore::data::EquityIndexReferenceDatum > | underlyingRefData () const |

| QuantLib::ext::shared_ptr< ore::data::CurrencyHedgedEquityIndexReferenceDatum > | indexRefData () const |

| void | addAdditionalFixingsForEquityIndexDecomposition (const QuantLib::Date &asof, std::map< std::string, RequiredFixings::FixingDates > &fixings) const |

Static Public Member Functions | |

| static QuantLib::Date | referenceDate (const QuantLib::ext::shared_ptr< CurrencyHedgedEquityIndexReferenceDatum > &refData, const QuantLib::Date &asof) |

| static QuantLib::Date | rebalancingDate (const QuantLib::ext::shared_ptr< CurrencyHedgedEquityIndexReferenceDatum > &refData, const QuantLib::Date &asof) |

Private Attributes | |

| std::string | name_ |

| QuantLib::ext::shared_ptr< ore::data::CurrencyHedgedEquityIndexReferenceDatum > | indexRefData_ |

| QuantLib::ext::shared_ptr< ore::data::EquityIndexReferenceDatum > | underlyingRefData_ |

| std::string | indexCurrency_ |

| std::string | underlyingIndexCurrency_ |

| std::string | fxIndexName_ |

| std::map< std::string, std::pair< double, std::string > > | currencyWeightsAndFxIndexNames_ |

Definition at line 21 of file currencyhedgedequityindexdecomposition.hpp.

| CurrencyHedgedEquityIndexDecomposition | ( | const std::string | indexName, |

| const QuantLib::ext::shared_ptr< ore::data::CurrencyHedgedEquityIndexReferenceDatum > & | indexRefData, | ||

| const QuantLib::ext::shared_ptr< ore::data::EquityIndexReferenceDatum > | underlyingRefData, | ||

| const std::string & | indexCurrency, | ||

| const std::string & | underlyingIndexCurrency, | ||

| const std::string & | fxIndexName, | ||

| const std::map< std::string, std::pair< double, std::string > > & | currencyWeightsAndFxIndexNames | ||

| ) |

Definition at line 23 of file currencyhedgedequityindexdecomposition.hpp.

| const std::string & indexName | ( | ) | const |

Definition at line 40 of file currencyhedgedequityindexdecomposition.hpp.

Here is the caller graph for this function:| const std::string & underlyingIndexName | ( | ) | const |

Definition at line 42 of file currencyhedgedequityindexdecomposition.hpp.

Here is the caller graph for this function:| const std::string & indexCurrency | ( | ) | const |

Definition at line 44 of file currencyhedgedequityindexdecomposition.hpp.

| const std::string & underlyingIndexCurrency | ( | ) | const |

Definition at line 46 of file currencyhedgedequityindexdecomposition.hpp.

| const std::string & fxIndexName | ( | ) | const |

Definition at line 48 of file currencyhedgedequityindexdecomposition.hpp.

Here is the caller graph for this function:| bool isValid | ( | ) | const |

Definition at line 50 of file currencyhedgedequityindexdecomposition.hpp.

Here is the caller graph for this function:| QuantLib::Date referenceDate | ( | const QuantLib::Date & | asof | ) | const |

Definition at line 149 of file currencyhedgedequityindexdecomposition.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| QuantLib::Date rebalancingDate | ( | const QuantLib::Date & | asof | ) | const |

Definition at line 153 of file currencyhedgedequityindexdecomposition.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

static |

Definition at line 119 of file currencyhedgedequityindexdecomposition.cpp.

Here is the call graph for this function:

|

static |

Definition at line 131 of file currencyhedgedequityindexdecomposition.cpp.

| const std::map< std::string, std::pair< double, std::string > > & currencyWeightsAndFxIndexNames | ( | ) | const |

Definition at line 62 of file currencyhedgedequityindexdecomposition.hpp.

Here is the caller graph for this function:| std::map< std::string, double > fxSpotRiskFromForwards | ( | const double | quantity, |

| const QuantLib::Date & | asof, | ||

| const QuantLib::ext::shared_ptr< ore::data::Market > & | todaysMarket, | ||

| const double | shiftsize | ||

| ) | const |

Definition at line 157 of file currencyhedgedequityindexdecomposition.cpp.

Here is the call graph for this function:| double unhedgedSpotExposure | ( | double | hedgedExposure, |

| const double | quantity, | ||

| const QuantLib::Date & | asof, | ||

| const QuantLib::ext::shared_ptr< ore::data::Market > & | todaysMarket | ||

| ) | const |

Definition at line 182 of file currencyhedgedequityindexdecomposition.cpp.

Here is the call graph for this function:| QuantLib::ext::shared_ptr< ore::data::EquityIndexReferenceDatum > underlyingRefData | ( | ) | const |

Definition at line 73 of file currencyhedgedequityindexdecomposition.hpp.

| QuantLib::ext::shared_ptr< ore::data::CurrencyHedgedEquityIndexReferenceDatum > indexRefData | ( | ) | const |

Definition at line 75 of file currencyhedgedequityindexdecomposition.hpp.

Here is the caller graph for this function:| void addAdditionalFixingsForEquityIndexDecomposition | ( | const QuantLib::Date & | asof, |

| std::map< std::string, RequiredFixings::FixingDates > & | fixings | ||

| ) | const |

Definition at line 203 of file currencyhedgedequityindexdecomposition.cpp.

Here is the call graph for this function:

|

private |

Definition at line 82 of file currencyhedgedequityindexdecomposition.hpp.

|

private |

Definition at line 83 of file currencyhedgedequityindexdecomposition.hpp.

|

private |

Definition at line 84 of file currencyhedgedequityindexdecomposition.hpp.

|

private |

Definition at line 85 of file currencyhedgedequityindexdecomposition.hpp.

|

private |

Definition at line 86 of file currencyhedgedequityindexdecomposition.hpp.

|

private |

Definition at line 87 of file currencyhedgedequityindexdecomposition.hpp.

|

private |

Definition at line 88 of file currencyhedgedequityindexdecomposition.hpp.