Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Container for storing Cross Currency Basis Swap quote conventions. More...

#include <ored/configuration/conventions.hpp>

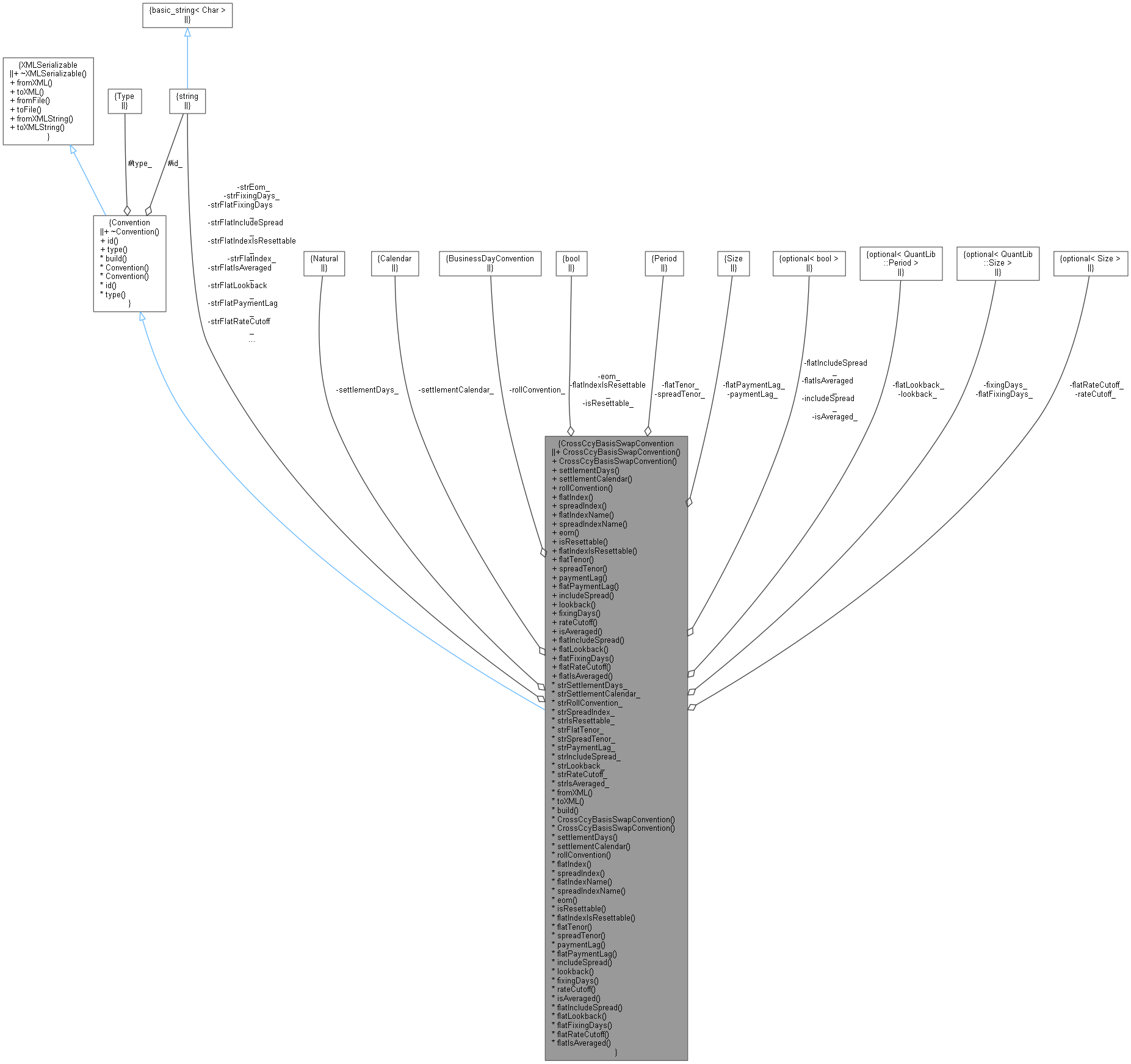

Inheritance diagram for CrossCcyBasisSwapConvention: Collaboration diagram for CrossCcyBasisSwapConvention:

Inheritance diagram for CrossCcyBasisSwapConvention: Collaboration diagram for CrossCcyBasisSwapConvention:Public Member Functions | |

Constructors | |

| CrossCcyBasisSwapConvention () | |

| Default constructor. More... | |

| CrossCcyBasisSwapConvention (const string &id, const string &strSettlementDays, const string &strSettlementCalendar, const string &strRollConvention, const string &flatIndex, const string &spreadIndex, const string &strEom="", const string &strIsResettable="", const string &strFlatIndexIsResettable="", const std::string &strFlatTenor="", const std::string &strSpreadTenor="", const string &strPaymentLag="", const string &strFlatPaymentLag="", const string &strIncludeSpread="", const string &strLookback="", const string &strFixingDays="", const string &strRateCutoff="", const string &strIsAveraged="", const string &strFlatIncludeSpread="", const string &strFlatLookback="", const string &strFlatFixingDays="", const string &strFlatRateCutoff="", const string &strFlatIsAveraged="", const Conventions *conventions=nullptr) | |

| Detailed constructor. More... | |

Inspectors | |

| Natural | settlementDays () const |

| const Calendar & | settlementCalendar () const |

| BusinessDayConvention | rollConvention () const |

| QuantLib::ext::shared_ptr< IborIndex > | flatIndex () const |

| QuantLib::ext::shared_ptr< IborIndex > | spreadIndex () const |

| const string & | flatIndexName () const |

| const string & | spreadIndexName () const |

| bool | eom () const |

| bool | isResettable () const |

| bool | flatIndexIsResettable () const |

| const QuantLib::Period & | flatTenor () const |

| const QuantLib::Period & | spreadTenor () const |

| Size | paymentLag () const |

| Size | flatPaymentLag () const |

| boost::optional< bool > | includeSpread () const |

| boost::optional< QuantLib::Period > | lookback () const |

| boost::optional< QuantLib::Size > | fixingDays () const |

| boost::optional< Size > | rateCutoff () const |

| boost::optional< bool > | isAveraged () const |

| boost::optional< bool > | flatIncludeSpread () const |

| boost::optional< QuantLib::Period > | flatLookback () const |

| boost::optional< QuantLib::Size > | flatFixingDays () const |

| boost::optional< Size > | flatRateCutoff () const |

| boost::optional< bool > | flatIsAveraged () const |

| Public Member Functions inherited from Convention | |

| virtual | ~Convention () |

| Default destructor. More... | |

| const string & | id () const |

| Type | type () const |

| Public Member Functions inherited from XMLSerializable | |

| virtual | ~XMLSerializable () |

| virtual void | fromXML (XMLNode *node)=0 |

| virtual XMLNode * | toXML (XMLDocument &doc) const =0 |

| void | fromFile (const std::string &filename) |

| void | toFile (const std::string &filename) const |

| void | fromXMLString (const std::string &xml) |

| Parse from XML string. More... | |

| std::string | toXMLString () const |

| Parse from XML string. More... | |

Additional Inherited Members | |

| Public Types inherited from Convention | |

| enum class | Type { Zero , Deposit , Future , FRA , OIS , Swap , AverageOIS , TenorBasisSwap , TenorBasisTwoSwap , BMABasisSwap , FX , CrossCcyBasis , CrossCcyFixFloat , CDS , IborIndex , OvernightIndex , SwapIndex , ZeroInflationIndex , InflationSwap , SecuritySpread , CMSSpreadOption , CommodityForward , CommodityFuture , FxOption , BondYield } |

| Supported convention types. More... | |

| Protected Member Functions inherited from Convention | |

| Convention () | |

| Convention (const string &id, Type type) | |

| Protected Attributes inherited from Convention | |

| Type | type_ |

| string | id_ |

Container for storing Cross Currency Basis Swap quote conventions.

Definition at line 841 of file conventions.hpp.

| CrossCcyBasisSwapConvention | ( | const string & | id, |

| const string & | strSettlementDays, | ||

| const string & | strSettlementCalendar, | ||

| const string & | strRollConvention, | ||

| const string & | flatIndex, | ||

| const string & | spreadIndex, | ||

| const string & | strEom = "", |

||

| const string & | strIsResettable = "", |

||

| const string & | strFlatIndexIsResettable = "", |

||

| const std::string & | strFlatTenor = "", |

||

| const std::string & | strSpreadTenor = "", |

||

| const string & | strPaymentLag = "", |

||

| const string & | strFlatPaymentLag = "", |

||

| const string & | strIncludeSpread = "", |

||

| const string & | strLookback = "", |

||

| const string & | strFixingDays = "", |

||

| const string & | strRateCutoff = "", |

||

| const string & | strIsAveraged = "", |

||

| const string & | strFlatIncludeSpread = "", |

||

| const string & | strFlatLookback = "", |

||

| const string & | strFlatFixingDays = "", |

||

| const string & | strFlatRateCutoff = "", |

||

| const string & | strFlatIsAveraged = "", |

||

| const Conventions * | conventions = nullptr |

||

| ) |

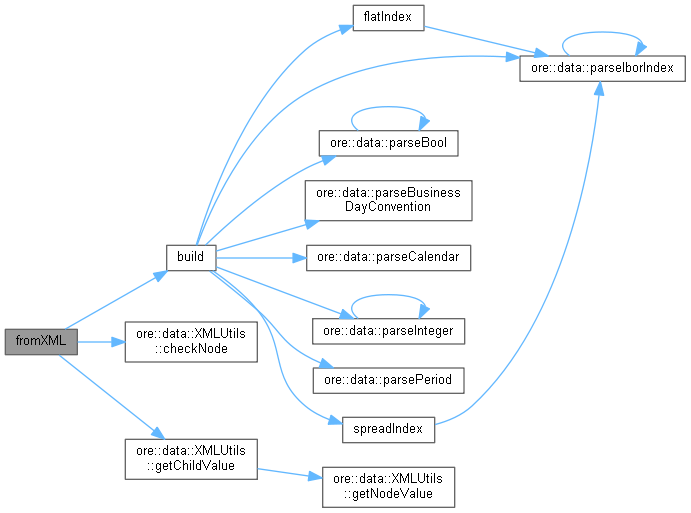

Detailed constructor.

Definition at line 907 of file conventions.cpp.

Here is the call graph for this function:| Natural settlementDays | ( | ) | const |

Definition at line 863 of file conventions.hpp.

| const Calendar & settlementCalendar | ( | ) | const |

Definition at line 864 of file conventions.hpp.

| BusinessDayConvention rollConvention | ( | ) | const |

Definition at line 865 of file conventions.hpp.

| QuantLib::ext::shared_ptr< IborIndex > flatIndex | ( | ) | const |

Definition at line 1077 of file conventions.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| QuantLib::ext::shared_ptr< IborIndex > spreadIndex | ( | ) | const |

Definition at line 1078 of file conventions.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| const string & flatIndexName | ( | ) | const |

Definition at line 868 of file conventions.hpp.

| const string & spreadIndexName | ( | ) | const |

Definition at line 869 of file conventions.hpp.

| bool eom | ( | ) | const |

Definition at line 871 of file conventions.hpp.

| bool isResettable | ( | ) | const |

Definition at line 872 of file conventions.hpp.

| bool flatIndexIsResettable | ( | ) | const |

Definition at line 873 of file conventions.hpp.

| const QuantLib::Period & flatTenor | ( | ) | const |

Definition at line 874 of file conventions.hpp.

| const QuantLib::Period & spreadTenor | ( | ) | const |

Definition at line 875 of file conventions.hpp.

| Size paymentLag | ( | ) | const |

Definition at line 877 of file conventions.hpp.

| Size flatPaymentLag | ( | ) | const |

Definition at line 878 of file conventions.hpp.

| boost::optional< bool > includeSpread | ( | ) | const |

Definition at line 881 of file conventions.hpp.

| boost::optional< QuantLib::Period > lookback | ( | ) | const |

Definition at line 882 of file conventions.hpp.

| boost::optional< QuantLib::Size > fixingDays | ( | ) | const |

Definition at line 883 of file conventions.hpp.

| boost::optional< Size > rateCutoff | ( | ) | const |

Definition at line 884 of file conventions.hpp.

| boost::optional< bool > isAveraged | ( | ) | const |

Definition at line 885 of file conventions.hpp.

| boost::optional< bool > flatIncludeSpread | ( | ) | const |

Definition at line 886 of file conventions.hpp.

| boost::optional< QuantLib::Period > flatLookback | ( | ) | const |

Definition at line 887 of file conventions.hpp.

| boost::optional< QuantLib::Size > flatFixingDays | ( | ) | const |

Definition at line 888 of file conventions.hpp.

| boost::optional< Size > flatRateCutoff | ( | ) | const |

Definition at line 889 of file conventions.hpp.

| boost::optional< bool > flatIsAveraged | ( | ) | const |

Definition at line 890 of file conventions.hpp.

|

overridevirtual |

Implements XMLSerializable.

Definition at line 989 of file conventions.cpp.

Here is the call graph for this function:

|

overridevirtual |

Implements XMLSerializable.

Definition at line 1027 of file conventions.cpp.

Here is the call graph for this function:

|

overridevirtual |

Implements Convention.

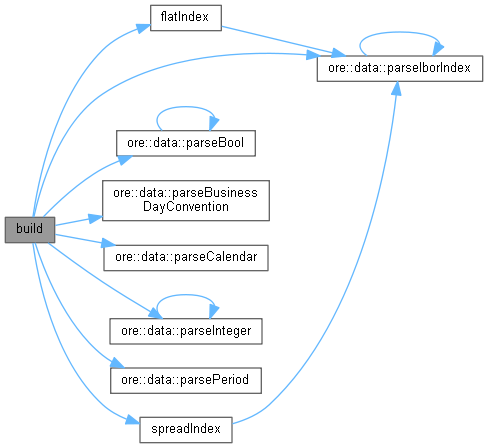

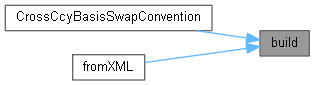

Definition at line 928 of file conventions.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

private |

Definition at line 900 of file conventions.hpp.

|

private |

Definition at line 901 of file conventions.hpp.

|

private |

Definition at line 902 of file conventions.hpp.

|

private |

Definition at line 903 of file conventions.hpp.

|

private |

Definition at line 904 of file conventions.hpp.

|

private |

Definition at line 905 of file conventions.hpp.

|

private |

Definition at line 906 of file conventions.hpp.

|

private |

Definition at line 907 of file conventions.hpp.

|

private |

Definition at line 908 of file conventions.hpp.

|

private |

Definition at line 909 of file conventions.hpp.

|

private |

Definition at line 911 of file conventions.hpp.

|

private |

Definition at line 912 of file conventions.hpp.

|

private |

Definition at line 913 of file conventions.hpp.

|

private |

Definition at line 914 of file conventions.hpp.

|

private |

Definition at line 915 of file conventions.hpp.

|

private |

Definition at line 916 of file conventions.hpp.

|

private |

Definition at line 917 of file conventions.hpp.

|

private |

Definition at line 918 of file conventions.hpp.

|

private |

Definition at line 919 of file conventions.hpp.

|

private |

Definition at line 920 of file conventions.hpp.

|

private |

Definition at line 923 of file conventions.hpp.

|

private |

Definition at line 924 of file conventions.hpp.

|

private |

Definition at line 925 of file conventions.hpp.

|

private |

Definition at line 926 of file conventions.hpp.

|

private |

Definition at line 927 of file conventions.hpp.

|

private |

Definition at line 928 of file conventions.hpp.

|

private |

Definition at line 929 of file conventions.hpp.

|

private |

Definition at line 930 of file conventions.hpp.

|

private |

Definition at line 931 of file conventions.hpp.

|

private |

Definition at line 932 of file conventions.hpp.

|

private |

Definition at line 933 of file conventions.hpp.

|

private |

Definition at line 934 of file conventions.hpp.

|

private |

Definition at line 936 of file conventions.hpp.

|

private |

Definition at line 937 of file conventions.hpp.

|

private |

Definition at line 938 of file conventions.hpp.

|

private |

Definition at line 939 of file conventions.hpp.

|

private |

Definition at line 940 of file conventions.hpp.

|

private |

Definition at line 941 of file conventions.hpp.

|

private |

Definition at line 942 of file conventions.hpp.

|

private |

Definition at line 943 of file conventions.hpp.

|

private |

Definition at line 944 of file conventions.hpp.

|

private |

Definition at line 945 of file conventions.hpp.