Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <ored/configuration/conventions.hpp>

Inheritance diagram for CommodityFutureConvention: Collaboration diagram for CommodityFutureConvention:

Inheritance diagram for CommodityFutureConvention: Collaboration diagram for CommodityFutureConvention:Classes | |

| class | AveragingData |

| struct | BusinessDaysAfter |

| struct | CalendarDaysBefore |

| struct | DayOfMonth |

| Classes to differentiate constructors below. More... | |

| class | OffPeakPowerIndexData |

| Class to store conventions for creating an off peak power index. More... | |

| struct | OptionExpiryAnchorDateRule |

| class | ProhibitedExpiry |

| Class to hold prohibited expiry information. More... | |

| struct | WeeklyWeekday |

Public Types | |

| enum class | AnchorType { DayOfMonth , NthWeekday , CalendarDaysBefore , LastWeekday , BusinessDaysAfter , WeeklyDayOfTheWeek } |

| enum class | OptionAnchorType { DayOfMonth , NthWeekday , BusinessDaysBefore , LastWeekday , WeeklyDayOfTheWeek } |

| Public Types inherited from Convention | |

| enum class | Type { Zero , Deposit , Future , FRA , OIS , Swap , AverageOIS , TenorBasisSwap , TenorBasisTwoSwap , BMABasisSwap , FX , CrossCcyBasis , CrossCcyFixFloat , CDS , IborIndex , OvernightIndex , SwapIndex , ZeroInflationIndex , InflationSwap , SecuritySpread , CMSSpreadOption , CommodityForward , CommodityFuture , FxOption , BondYield } |

| Supported convention types. More... | |

Public Member Functions | |

Constructors | |

| CommodityFutureConvention () | |

| Default constructor. More... | |

| CommodityFutureConvention (const std::string &id, const DayOfMonth &dayOfMonth, const std::string &contractFrequency, const std::string &calendar, const std::string &expiryCalendar="", QuantLib::Size expiryMonthLag=0, const std::string &oneContractMonth="", const std::string &offsetDays="", const std::string &bdc="", bool adjustBeforeOffset=true, bool isAveraging=false, const OptionExpiryAnchorDateRule &optionExpiryDateRule=OptionExpiryAnchorDateRule(), const std::set< ProhibitedExpiry > &prohibitedExpiries={}, QuantLib::Size optionExpiryMonthLag=0, const std::string &optionBdc="", const std::map< QuantLib::Natural, QuantLib::Natural > &futureContinuationMappings={}, const std::map< QuantLib::Natural, QuantLib::Natural > &optionContinuationMappings={}, const AveragingData &averagingData=AveragingData(), QuantLib::Natural hoursPerDay=QuantLib::Null< QuantLib::Natural >(), const boost::optional< OffPeakPowerIndexData > &offPeakPowerIndexData=boost::none, const std::string &indexName="", const std::string &optionFrequency="") | |

| Day of month based constructor. More... | |

| CommodityFutureConvention (const std::string &id, const std::string &nth, const std::string &weekday, const std::string &contractFrequency, const std::string &calendar, const std::string &expiryCalendar="", QuantLib::Size expiryMonthLag=0, const std::string &oneContractMonth="", const std::string &offsetDays="", const std::string &bdc="", bool adjustBeforeOffset=true, bool isAveraging=false, const OptionExpiryAnchorDateRule &optionExpiryDateRule=OptionExpiryAnchorDateRule(), const std::set< ProhibitedExpiry > &prohibitedExpiries={}, QuantLib::Size optionExpiryMonthLag=0, const std::string &optionBdc="", const std::map< QuantLib::Natural, QuantLib::Natural > &futureContinuationMappings={}, const std::map< QuantLib::Natural, QuantLib::Natural > &optionContinuationMappings={}, const AveragingData &averagingData=AveragingData(), QuantLib::Natural hoursPerDay=QuantLib::Null< QuantLib::Natural >(), const boost::optional< OffPeakPowerIndexData > &offPeakPowerIndexData=boost::none, const std::string &indexName="", const std::string &optionFrequency="") | |

| N-th weekday based constructor. More... | |

| CommodityFutureConvention (const std::string &id, const CalendarDaysBefore &calendarDaysBefore, const std::string &contractFrequency, const std::string &calendar, const std::string &expiryCalendar="", QuantLib::Size expiryMonthLag=0, const std::string &oneContractMonth="", const std::string &offsetDays="", const std::string &bdc="", bool adjustBeforeOffset=true, bool isAveraging=false, const OptionExpiryAnchorDateRule &optionExpiryDateRule=OptionExpiryAnchorDateRule(), const std::set< ProhibitedExpiry > &prohibitedExpiries={}, QuantLib::Size optionExpiryMonthLag=0, const std::string &optionBdc="", const std::map< QuantLib::Natural, QuantLib::Natural > &futureContinuationMappings={}, const std::map< QuantLib::Natural, QuantLib::Natural > &optionContinuationMappings={}, const AveragingData &averagingData=AveragingData(), QuantLib::Natural hoursPerDay=QuantLib::Null< QuantLib::Natural >(), const boost::optional< OffPeakPowerIndexData > &offPeakPowerIndexData=boost::none, const std::string &indexName="", const std::string &optionFrequency="") | |

| Calendar days before based constructor. More... | |

| CommodityFutureConvention (const std::string &id, const BusinessDaysAfter &businessDaysAfter, const std::string &contractFrequency, const std::string &calendar, const std::string &expiryCalendar="", QuantLib::Size expiryMonthLag=0, const std::string &oneContractMonth="", const std::string &offsetDays="", const std::string &bdc="", bool adjustBeforeOffset=true, bool isAveraging=false, const OptionExpiryAnchorDateRule &optionExpiryDateRule=OptionExpiryAnchorDateRule(), const std::set< ProhibitedExpiry > &prohibitedExpiries={}, QuantLib::Size optionExpiryMonthLag=0, const std::string &optionBdc="", const std::map< QuantLib::Natural, QuantLib::Natural > &futureContinuationMappings={}, const std::map< QuantLib::Natural, QuantLib::Natural > &optionContinuationMappings={}, const AveragingData &averagingData=AveragingData(), QuantLib::Natural hoursPerDay=QuantLib::Null< QuantLib::Natural >(), const boost::optional< OffPeakPowerIndexData > &offPeakPowerIndexData=boost::none, const std::string &indexName="", const std::string &optionFrequency="") | |

| Business days before based constructor. More... | |

| Public Member Functions inherited from Convention | |

| virtual | ~Convention () |

| Default destructor. More... | |

| const string & | id () const |

| Type | type () const |

| Public Member Functions inherited from XMLSerializable | |

| virtual | ~XMLSerializable () |

| virtual void | fromXML (XMLNode *node)=0 |

| virtual XMLNode * | toXML (XMLDocument &doc) const =0 |

| void | fromFile (const std::string &filename) |

| void | toFile (const std::string &filename) const |

| void | fromXMLString (const std::string &xml) |

| Parse from XML string. More... | |

| std::string | toXMLString () const |

| Parse from XML string. More... | |

Inspectors | |

| AnchorType | anchorType_ |

| QuantLib::Natural | dayOfMonth_ |

| QuantLib::Natural | nth_ |

| QuantLib::Weekday | weekday_ |

| QuantLib::Natural | calendarDaysBefore_ |

| QuantLib::Integer | businessDaysAfter_ |

| QuantLib::Frequency | contractFrequency_ |

| QuantLib::Calendar | calendar_ |

| QuantLib::Calendar | expiryCalendar_ |

| QuantLib::Month | oneContractMonth_ |

| QuantLib::Integer | offsetDays_ |

| QuantLib::BusinessDayConvention | bdc_ |

| std::string | strDayOfMonth_ |

| std::string | strNth_ |

| std::string | strWeekday_ |

| std::string | strCalendarDaysBefore_ |

| std::string | strBusinessDaysAfter_ |

| std::string | strContractFrequency_ |

| std::string | strCalendar_ |

| std::string | strExpiryCalendar_ |

| QuantLib::Size | expiryMonthLag_ |

| std::string | strOneContractMonth_ |

| std::string | strOffsetDays_ |

| std::string | strBdc_ |

| bool | adjustBeforeOffset_ |

| bool | isAveraging_ |

| std::set< ProhibitedExpiry > | prohibitedExpiries_ |

| QuantLib::Size | optionExpiryMonthLag_ |

| QuantLib::BusinessDayConvention | optionBdc_ |

| std::string | strOptionBdc_ |

| std::map< QuantLib::Natural, QuantLib::Natural > | futureContinuationMappings_ |

| std::map< QuantLib::Natural, QuantLib::Natural > | optionContinuationMappings_ |

| AveragingData | averagingData_ |

| QuantLib::Natural | hoursPerDay_ |

| boost::optional< OffPeakPowerIndexData > | offPeakPowerIndexData_ |

| std::string | indexName_ |

| std::string | strOptionContractFrequency_ |

| OptionAnchorType | optionAnchorType_ |

| std::string | strOptionExpiryOffset_ |

| std::string | strOptionExpiryDay_ |

| std::string | strOptionNth_ |

| std::string | strOptionWeekday_ |

| QuantLib::Frequency | optionContractFrequency_ |

| QuantLib::Natural | optionExpiryOffset_ |

| QuantLib::Natural | optionNth_ |

| QuantLib::Weekday | optionWeekday_ |

| QuantLib::Natural | optionExpiryDay_ |

| std::set< QuantLib::Month > | validContractMonths_ |

| std::string | savingsTime_ |

| bool | balanceOfTheMonth_ |

| std::string | balanceOfTheMonthPricingCalendarStr_ |

| Calendar | balanceOfTheMonthPricingCalendar_ |

| std::string | optionUnderlyingFutureConvention_ |

| Option Underlying Future convention. More... | |

| AnchorType | anchorType () const |

| QuantLib::Natural | dayOfMonth () const |

| QuantLib::Natural | nth () const |

| QuantLib::Weekday | weekday () const |

| QuantLib::Natural | calendarDaysBefore () const |

| QuantLib::Integer | businessDaysAfter () const |

| QuantLib::Frequency | contractFrequency () const |

| const QuantLib::Calendar & | calendar () const |

| const QuantLib::Calendar & | expiryCalendar () const |

| QuantLib::Size | expiryMonthLag () const |

| QuantLib::Month | oneContractMonth () const |

| QuantLib::Integer | offsetDays () const |

| QuantLib::BusinessDayConvention | businessDayConvention () const |

| bool | adjustBeforeOffset () const |

| bool | isAveraging () const |

| QuantLib::Natural | optionExpiryOffset () const |

| const std::set< ProhibitedExpiry > & | prohibitedExpiries () const |

| QuantLib::Size | optionExpiryMonthLag () const |

| QuantLib::Natural | optionExpiryDay () const |

| QuantLib::BusinessDayConvention | optionBusinessDayConvention () const |

| const std::map< QuantLib::Natural, QuantLib::Natural > & | futureContinuationMappings () const |

| const std::map< QuantLib::Natural, QuantLib::Natural > & | optionContinuationMappings () const |

| const AveragingData & | averagingData () const |

| QuantLib::Natural | hoursPerDay () const |

| const boost::optional< OffPeakPowerIndexData > & | offPeakPowerIndexData () const |

| const std::string & | indexName () const |

| QuantLib::Frequency | optionContractFrequency () const |

| OptionAnchorType | optionAnchorType () const |

| QuantLib::Natural | optionNth () const |

| QuantLib::Weekday | optionWeekday () const |

| const std::string & | savingsTime () const |

| const std::set< QuantLib::Month > & | validContractMonths () const |

| bool | balanceOfTheMonth () const |

| Calendar | balanceOfTheMonthPricingCalendar () const |

| const std::string & | optionUnderlyingFutureConvention () const |

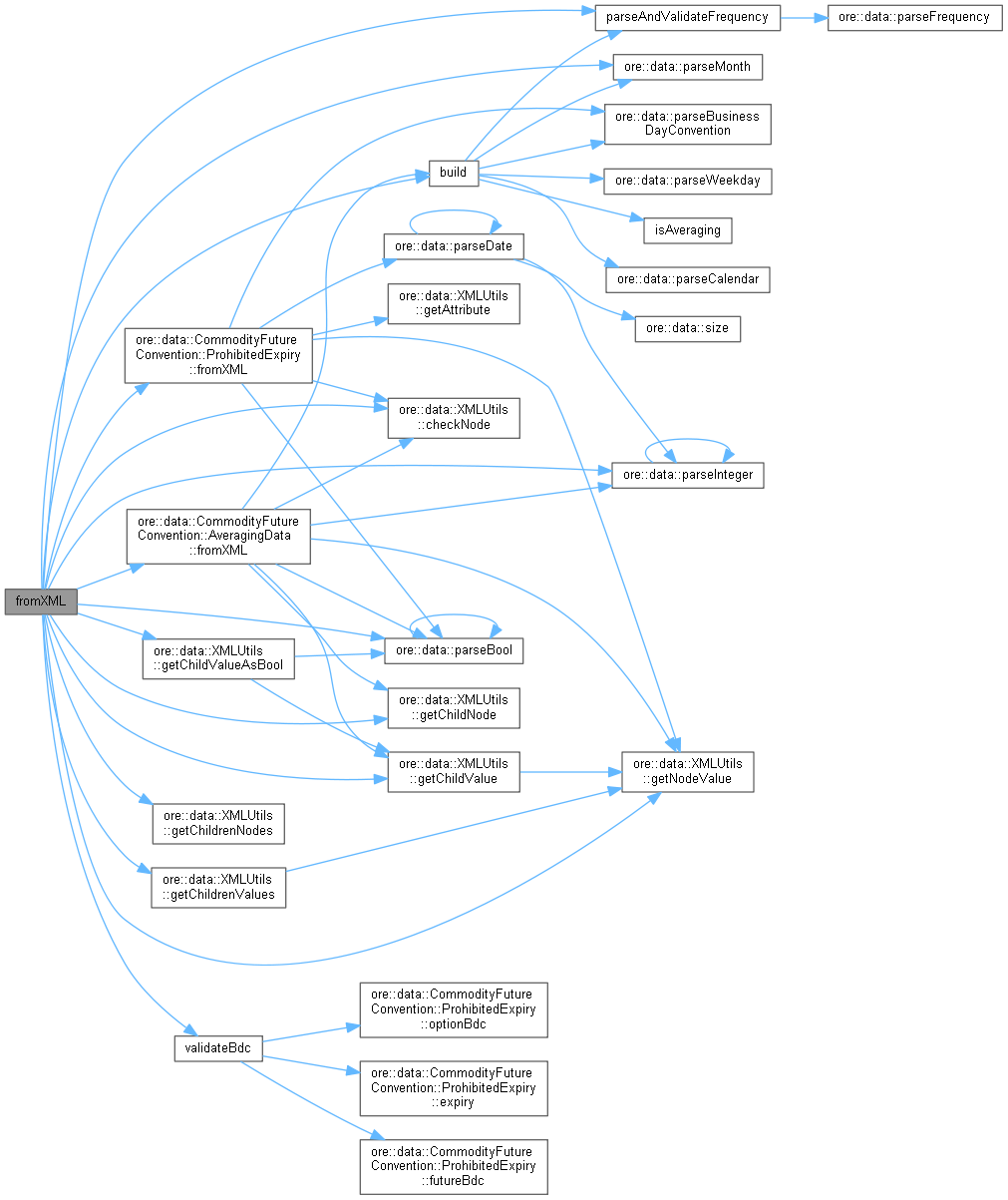

| void | fromXML (XMLNode *node) override |

| Serialisation. More... | |

| XMLNode * | toXML (XMLDocument &doc) const override |

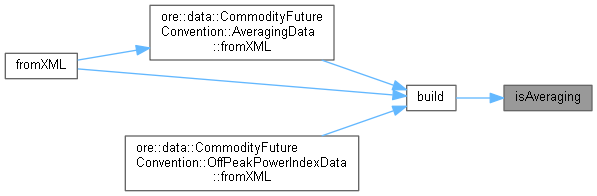

| void | build () override |

| Implementation. More... | |

| Frequency | parseAndValidateFrequency (const std::string &strFrequency) |

| Populate and check frequency. More... | |

| bool | validateBdc (const ProhibitedExpiry &pe) const |

| Validate the business day conventions in the ProhibitedExpiry. More... | |

Additional Inherited Members | |

| Protected Member Functions inherited from Convention | |

| Convention () | |

| Convention (const string &id, Type type) | |

| Protected Attributes inherited from Convention | |

| Type | type_ |

| string | id_ |

Container for storing commodity future conventions

Definition at line 1317 of file conventions.hpp.

|

strong |

The anchor day type of commodity future convention

| Enumerator | |

|---|---|

| DayOfMonth | |

| NthWeekday | |

| CalendarDaysBefore | |

| LastWeekday | |

| BusinessDaysAfter | |

| WeeklyDayOfTheWeek | |

Definition at line 1321 of file conventions.hpp.

|

strong |

| Enumerator | |

|---|---|

| DayOfMonth | |

| NthWeekday | |

| BusinessDaysBefore | |

| LastWeekday | |

| WeeklyDayOfTheWeek | |

Definition at line 1322 of file conventions.hpp.

Default constructor.

Definition at line 1712 of file conventions.cpp.

| CommodityFutureConvention | ( | const std::string & | id, |

| const DayOfMonth & | dayOfMonth, | ||

| const std::string & | contractFrequency, | ||

| const std::string & | calendar, | ||

| const std::string & | expiryCalendar = "", |

||

| QuantLib::Size | expiryMonthLag = 0, |

||

| const std::string & | oneContractMonth = "", |

||

| const std::string & | offsetDays = "", |

||

| const std::string & | bdc = "", |

||

| bool | adjustBeforeOffset = true, |

||

| bool | isAveraging = false, |

||

| const OptionExpiryAnchorDateRule & | optionExpiryDateRule = OptionExpiryAnchorDateRule(), |

||

| const std::set< ProhibitedExpiry > & | prohibitedExpiries = {}, |

||

| QuantLib::Size | optionExpiryMonthLag = 0, |

||

| const std::string & | optionBdc = "", |

||

| const std::map< QuantLib::Natural, QuantLib::Natural > & | futureContinuationMappings = {}, |

||

| const std::map< QuantLib::Natural, QuantLib::Natural > & | optionContinuationMappings = {}, |

||

| const AveragingData & | averagingData = AveragingData(), |

||

| QuantLib::Natural | hoursPerDay = QuantLib::Null< QuantLib::Natural >(), |

||

| const boost::optional< OffPeakPowerIndexData > & | offPeakPowerIndexData = boost::none, |

||

| const std::string & | indexName = "", |

||

| const std::string & | optionFrequency = "" |

||

| ) |

Day of month based constructor.

| CommodityFutureConvention | ( | const std::string & | id, |

| const std::string & | nth, | ||

| const std::string & | weekday, | ||

| const std::string & | contractFrequency, | ||

| const std::string & | calendar, | ||

| const std::string & | expiryCalendar = "", |

||

| QuantLib::Size | expiryMonthLag = 0, |

||

| const std::string & | oneContractMonth = "", |

||

| const std::string & | offsetDays = "", |

||

| const std::string & | bdc = "", |

||

| bool | adjustBeforeOffset = true, |

||

| bool | isAveraging = false, |

||

| const OptionExpiryAnchorDateRule & | optionExpiryDateRule = OptionExpiryAnchorDateRule(), |

||

| const std::set< ProhibitedExpiry > & | prohibitedExpiries = {}, |

||

| QuantLib::Size | optionExpiryMonthLag = 0, |

||

| const std::string & | optionBdc = "", |

||

| const std::map< QuantLib::Natural, QuantLib::Natural > & | futureContinuationMappings = {}, |

||

| const std::map< QuantLib::Natural, QuantLib::Natural > & | optionContinuationMappings = {}, |

||

| const AveragingData & | averagingData = AveragingData(), |

||

| QuantLib::Natural | hoursPerDay = QuantLib::Null< QuantLib::Natural >(), |

||

| const boost::optional< OffPeakPowerIndexData > & | offPeakPowerIndexData = boost::none, |

||

| const std::string & | indexName = "", |

||

| const std::string & | optionFrequency = "" |

||

| ) |

N-th weekday based constructor.

| CommodityFutureConvention | ( | const std::string & | id, |

| const CalendarDaysBefore & | calendarDaysBefore, | ||

| const std::string & | contractFrequency, | ||

| const std::string & | calendar, | ||

| const std::string & | expiryCalendar = "", |

||

| QuantLib::Size | expiryMonthLag = 0, |

||

| const std::string & | oneContractMonth = "", |

||

| const std::string & | offsetDays = "", |

||

| const std::string & | bdc = "", |

||

| bool | adjustBeforeOffset = true, |

||

| bool | isAveraging = false, |

||

| const OptionExpiryAnchorDateRule & | optionExpiryDateRule = OptionExpiryAnchorDateRule(), |

||

| const std::set< ProhibitedExpiry > & | prohibitedExpiries = {}, |

||

| QuantLib::Size | optionExpiryMonthLag = 0, |

||

| const std::string & | optionBdc = "", |

||

| const std::map< QuantLib::Natural, QuantLib::Natural > & | futureContinuationMappings = {}, |

||

| const std::map< QuantLib::Natural, QuantLib::Natural > & | optionContinuationMappings = {}, |

||

| const AveragingData & | averagingData = AveragingData(), |

||

| QuantLib::Natural | hoursPerDay = QuantLib::Null< QuantLib::Natural >(), |

||

| const boost::optional< OffPeakPowerIndexData > & | offPeakPowerIndexData = boost::none, |

||

| const std::string & | indexName = "", |

||

| const std::string & | optionFrequency = "" |

||

| ) |

Calendar days before based constructor.

| CommodityFutureConvention | ( | const std::string & | id, |

| const BusinessDaysAfter & | businessDaysAfter, | ||

| const std::string & | contractFrequency, | ||

| const std::string & | calendar, | ||

| const std::string & | expiryCalendar = "", |

||

| QuantLib::Size | expiryMonthLag = 0, |

||

| const std::string & | oneContractMonth = "", |

||

| const std::string & | offsetDays = "", |

||

| const std::string & | bdc = "", |

||

| bool | adjustBeforeOffset = true, |

||

| bool | isAveraging = false, |

||

| const OptionExpiryAnchorDateRule & | optionExpiryDateRule = OptionExpiryAnchorDateRule(), |

||

| const std::set< ProhibitedExpiry > & | prohibitedExpiries = {}, |

||

| QuantLib::Size | optionExpiryMonthLag = 0, |

||

| const std::string & | optionBdc = "", |

||

| const std::map< QuantLib::Natural, QuantLib::Natural > & | futureContinuationMappings = {}, |

||

| const std::map< QuantLib::Natural, QuantLib::Natural > & | optionContinuationMappings = {}, |

||

| const AveragingData & | averagingData = AveragingData(), |

||

| QuantLib::Natural | hoursPerDay = QuantLib::Null< QuantLib::Natural >(), |

||

| const boost::optional< OffPeakPowerIndexData > & | offPeakPowerIndexData = boost::none, |

||

| const std::string & | indexName = "", |

||

| const std::string & | optionFrequency = "" |

||

| ) |

Business days before based constructor.

| AnchorType anchorType | ( | ) | const |

| QuantLib::Natural dayOfMonth | ( | ) | const |

| QuantLib::Natural nth | ( | ) | const |

| QuantLib::Weekday weekday | ( | ) | const |

| QuantLib::Natural calendarDaysBefore | ( | ) | const |

| QuantLib::Integer businessDaysAfter | ( | ) | const |

Definition at line 1570 of file conventions.hpp.

Here is the caller graph for this function:| QuantLib::Frequency contractFrequency | ( | ) | const |

| const QuantLib::Calendar & calendar | ( | ) | const |

Definition at line 1572 of file conventions.hpp.

Here is the caller graph for this function:| const QuantLib::Calendar & expiryCalendar | ( | ) | const |

Definition at line 1573 of file conventions.hpp.

Here is the caller graph for this function:| QuantLib::Size expiryMonthLag | ( | ) | const |

| QuantLib::Month oneContractMonth | ( | ) | const |

Definition at line 1575 of file conventions.hpp.

| QuantLib::Integer offsetDays | ( | ) | const |

| QuantLib::BusinessDayConvention businessDayConvention | ( | ) | const |

| bool adjustBeforeOffset | ( | ) | const |

| bool isAveraging | ( | ) | const |

| QuantLib::Natural optionExpiryOffset | ( | ) | const |

| const std::set< ProhibitedExpiry > & prohibitedExpiries | ( | ) | const |

Definition at line 1581 of file conventions.hpp.

Here is the caller graph for this function:| QuantLib::Size optionExpiryMonthLag | ( | ) | const |

| QuantLib::Natural optionExpiryDay | ( | ) | const |

| QuantLib::BusinessDayConvention optionBusinessDayConvention | ( | ) | const |

| const std::map< QuantLib::Natural, QuantLib::Natural > & futureContinuationMappings | ( | ) | const |

Definition at line 1587 of file conventions.hpp.

| const std::map< QuantLib::Natural, QuantLib::Natural > & optionContinuationMappings | ( | ) | const |

Definition at line 1590 of file conventions.hpp.

| const AveragingData & averagingData | ( | ) | const |

Definition at line 1593 of file conventions.hpp.

| QuantLib::Natural hoursPerDay | ( | ) | const |

Definition at line 1594 of file conventions.hpp.

| const boost::optional< OffPeakPowerIndexData > & offPeakPowerIndexData | ( | ) | const |

Definition at line 1595 of file conventions.hpp.

| const std::string & indexName | ( | ) | const |

Definition at line 1596 of file conventions.hpp.

| QuantLib::Frequency optionContractFrequency | ( | ) | const |

| OptionAnchorType optionAnchorType | ( | ) | const |

| QuantLib::Natural optionNth | ( | ) | const |

| QuantLib::Weekday optionWeekday | ( | ) | const |

| const std::string & savingsTime | ( | ) | const |

Definition at line 1601 of file conventions.hpp.

| const std::set< QuantLib::Month > & validContractMonths | ( | ) | const |

Definition at line 1602 of file conventions.hpp.

Here is the caller graph for this function:| bool balanceOfTheMonth | ( | ) | const |

Definition at line 1603 of file conventions.hpp.

| Calendar balanceOfTheMonthPricingCalendar | ( | ) | const |

Definition at line 1604 of file conventions.hpp.

| const std::string & optionUnderlyingFutureConvention | ( | ) | const |

Definition at line 1605 of file conventions.hpp.

|

overridevirtual |

Serialisation.

Implements XMLSerializable.

Definition at line 1858 of file conventions.cpp.

Here is the call graph for this function:

|

overridevirtual |

Implements XMLSerializable.

Definition at line 2069 of file conventions.cpp.

Here is the call graph for this function:

|

overridevirtual |

Implementation.

Implements Convention.

Definition at line 2203 of file conventions.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

private |

Populate and check frequency.

Definition at line 2283 of file conventions.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

private |

Validate the business day conventions in the ProhibitedExpiry.

Definition at line 2290 of file conventions.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

private |

Definition at line 1618 of file conventions.hpp.

|

private |

Definition at line 1619 of file conventions.hpp.

|

private |

Definition at line 1620 of file conventions.hpp.

|

private |

Definition at line 1621 of file conventions.hpp.

|

private |

Definition at line 1622 of file conventions.hpp.

|

private |

Definition at line 1623 of file conventions.hpp.

|

private |

Definition at line 1624 of file conventions.hpp.

|

private |

Definition at line 1625 of file conventions.hpp.

|

private |

Definition at line 1626 of file conventions.hpp.

|

private |

Definition at line 1627 of file conventions.hpp.

|

private |

Definition at line 1628 of file conventions.hpp.

|

private |

Definition at line 1629 of file conventions.hpp.

|

private |

Definition at line 1632 of file conventions.hpp.

|

private |

Definition at line 1633 of file conventions.hpp.

|

private |

Definition at line 1634 of file conventions.hpp.

|

private |

Definition at line 1635 of file conventions.hpp.

|

private |

Definition at line 1636 of file conventions.hpp.

|

private |

Definition at line 1637 of file conventions.hpp.

|

private |

Definition at line 1638 of file conventions.hpp.

|

private |

Definition at line 1639 of file conventions.hpp.

|

private |

Definition at line 1640 of file conventions.hpp.

|

private |

Definition at line 1641 of file conventions.hpp.

|

private |

Definition at line 1642 of file conventions.hpp.

|

private |

Definition at line 1643 of file conventions.hpp.

|

private |

Definition at line 1644 of file conventions.hpp.

|

private |

Definition at line 1645 of file conventions.hpp.

|

private |

Definition at line 1646 of file conventions.hpp.

|

private |

Definition at line 1647 of file conventions.hpp.

|

private |

Definition at line 1648 of file conventions.hpp.

|

private |

Definition at line 1649 of file conventions.hpp.

|

private |

Definition at line 1650 of file conventions.hpp.

|

private |

Definition at line 1651 of file conventions.hpp.

|

private |

Definition at line 1652 of file conventions.hpp.

|

private |

Definition at line 1653 of file conventions.hpp.

|

private |

Definition at line 1654 of file conventions.hpp.

|

private |

Definition at line 1655 of file conventions.hpp.

|

private |

Definition at line 1657 of file conventions.hpp.

|

private |

Definition at line 1659 of file conventions.hpp.

|

private |

Definition at line 1660 of file conventions.hpp.

|

private |

Definition at line 1661 of file conventions.hpp.

|

private |

Definition at line 1662 of file conventions.hpp.

|

private |

Definition at line 1663 of file conventions.hpp.

|

private |

Definition at line 1666 of file conventions.hpp.

|

private |

Definition at line 1667 of file conventions.hpp.

|

private |

Definition at line 1668 of file conventions.hpp.

|

private |

Definition at line 1669 of file conventions.hpp.

|

private |

Definition at line 1670 of file conventions.hpp.

|

private |

Definition at line 1672 of file conventions.hpp.

|

private |

Definition at line 1673 of file conventions.hpp.

|

private |

Definition at line 1677 of file conventions.hpp.

|

private |

Definition at line 1678 of file conventions.hpp.

|

private |

Definition at line 1679 of file conventions.hpp.

|

private |

Option Underlying Future convention.

Definition at line 1681 of file conventions.hpp.