Hazard-rate-curve traits. More...

#include <probabilitytraits.hpp>

Collaboration diagram for HazardRate:

Collaboration diagram for HazardRate:

Classes | |

| struct | curve |

Public Types | |

| typedef BootstrapHelper< DefaultProbabilityTermStructure > | helper |

Static Public Member Functions | |

| static Date | initialDate (const DefaultProbabilityTermStructure *c) |

| static Real | initialValue (const DefaultProbabilityTermStructure *) |

| template<class C > | |

| static Real | guess (Size i, const C *c, bool validData, Size) |

| template<class C > | |

| static Real | minValueAfter (Size i, const C *c, bool validData, Size) |

| template<class C > | |

| static Real | maxValueAfter (Size i, const C *c, bool validData, Size) |

| static void | updateGuess (std::vector< Real > &data, Real rate, Size i) |

| static Size | maxIterations () |

Detailed Description

Hazard-rate-curve traits.

Definition at line 115 of file probabilitytraits.hpp.

Member Typedef Documentation

◆ helper

Definition at line 122 of file probabilitytraits.hpp.

Member Function Documentation

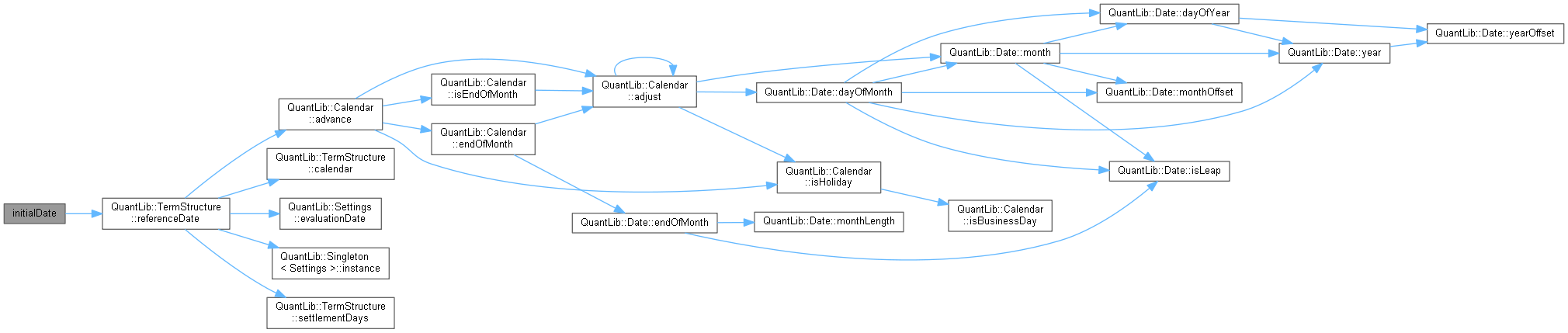

◆ initialDate()

|

static |

◆ initialValue()

|

static |

Definition at line 129 of file probabilitytraits.hpp.

◆ guess()

Definition at line 135 of file probabilitytraits.hpp.

◆ minValueAfter()

Definition at line 153 of file probabilitytraits.hpp.

◆ maxValueAfter()

Definition at line 165 of file probabilitytraits.hpp.

◆ updateGuess()

Definition at line 179 of file probabilitytraits.hpp.

◆ maxIterations()

|

static |

Definition at line 187 of file probabilitytraits.hpp.