callability leaving to the holder the possibility to convert More...

#include <convertiblebonds.hpp>

Inheritance diagram for SoftCallability:

Inheritance diagram for SoftCallability: Collaboration diagram for SoftCallability:

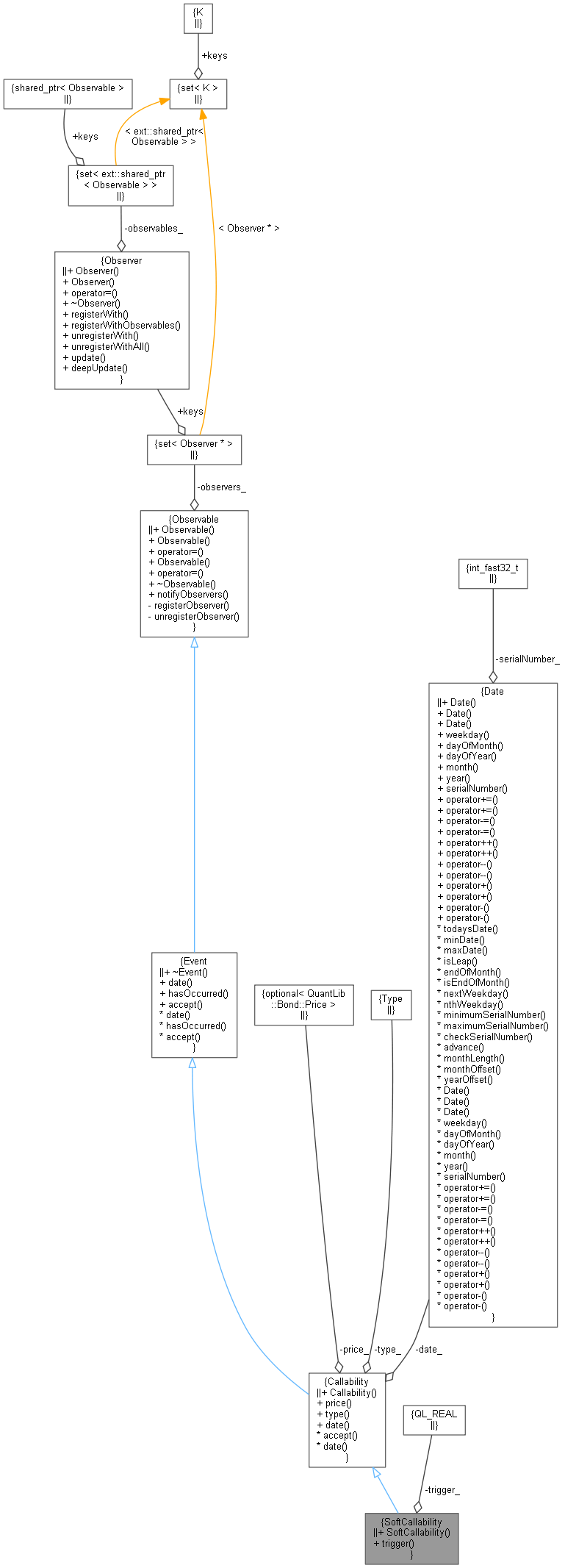

Collaboration diagram for SoftCallability:

Public Member Functions | |

| SoftCallability (const Bond::Price &price, const Date &date, Real trigger) | |

| Real | trigger () const |

| Public Member Functions inherited from Callability | |

| Callability (const Bond::Price &price, Type type, const Date &date) | |

| const Bond::Price & | price () const |

| Type | type () const |

| Date | date () const override |

| returns the date at which the event occurs More... | |

| void | accept (AcyclicVisitor &) override |

| Public Member Functions inherited from Event | |

| ~Event () override=default | |

| virtual bool | hasOccurred (const Date &refDate=Date(), ext::optional< bool > includeRefDate=ext::nullopt) const |

| returns true if an event has already occurred before a date More... | |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

Private Attributes | |

| Real | trigger_ |

Additional Inherited Members | |

| Public Types inherited from Callability | |

| enum | Type { Call , Put } |

| type of the callability More... | |

Detailed Description

callability leaving to the holder the possibility to convert

Definition at line 42 of file convertiblebonds.hpp.

Constructor & Destructor Documentation

◆ SoftCallability()

| SoftCallability | ( | const Bond::Price & | price, |

| const Date & | date, | ||

| Real | trigger | ||

| ) |

Definition at line 44 of file convertiblebonds.hpp.

Member Function Documentation

◆ trigger()

| Real trigger | ( | ) | const |

Definition at line 46 of file convertiblebonds.hpp.

Member Data Documentation

◆ trigger_

|

private |

Definition at line 49 of file convertiblebonds.hpp.