Black 1976 calculator class. More...

#include <blackcalculator.hpp>

Inheritance diagram for BlackCalculator:

Inheritance diagram for BlackCalculator: Collaboration diagram for BlackCalculator:

Collaboration diagram for BlackCalculator:

Public Member Functions | |

| BlackCalculator (const ext::shared_ptr< StrikedTypePayoff > &payoff, Real forward, Real stdDev, Real discount=1.0) | |

| BlackCalculator (Option::Type optionType, Real strike, Real forward, Real stdDev, Real discount=1.0) | |

| virtual | ~BlackCalculator ()=default |

| Real | value () const |

| Real | deltaForward () const |

| virtual Real | delta (Real spot) const |

| Real | elasticityForward () const |

| virtual Real | elasticity (Real spot) const |

| Real | gammaForward () const |

| virtual Real | gamma (Real spot) const |

| virtual Real | theta (Real spot, Time maturity) const |

| virtual Real | thetaPerDay (Real spot, Time maturity) const |

| Real | vega (Time maturity) const |

| Real | rho (Time maturity) const |

| Real | dividendRho (Time maturity) const |

| Real | itmCashProbability () const |

| Real | itmAssetProbability () const |

| Real | strikeSensitivity () const |

| Real | strikeGamma () const |

| Real | alpha () const |

| Real | beta () const |

Protected Member Functions | |

| void | initialize (const ext::shared_ptr< StrikedTypePayoff > &p) |

Protected Attributes | |

| Real | strike_ |

| Real | forward_ |

| Real | stdDev_ |

| Real | discount_ |

| Real | variance_ |

| Real | d1_ |

| Real | d2_ |

| Real | alpha_ |

| Real | beta_ |

| Real | DalphaDd1_ |

| Real | DbetaDd2_ |

| Real | n_d1_ |

| Real | cum_d1_ |

| Real | n_d2_ |

| Real | cum_d2_ |

| Real | x_ |

| Real | DxDs_ |

| Real | DxDstrike_ |

Detailed Description

Black 1976 calculator class.

- Bug:

- When the variance is null, division by zero occur during the calculation of delta, delta forward, gamma, gamma forward, rho, dividend rho, vega, and strike sensitivity.

- Examples

- DiscreteHedging.cpp.

Definition at line 37 of file blackcalculator.hpp.

Constructor & Destructor Documentation

◆ BlackCalculator() [1/2]

| BlackCalculator | ( | const ext::shared_ptr< StrikedTypePayoff > & | payoff, |

| Real | forward, | ||

| Real | stdDev, | ||

| Real | discount = 1.0 |

||

| ) |

◆ BlackCalculator() [2/2]

| BlackCalculator | ( | Option::Type | optionType, |

| Real | strike, | ||

| Real | forward, | ||

| Real | stdDev, | ||

| Real | discount = 1.0 |

||

| ) |

Definition at line 54 of file blackcalculator.cpp.

◆ ~BlackCalculator()

|

virtualdefault |

Member Function Documentation

◆ value()

| Real value | ( | ) | const |

- Examples

- DiscreteHedging.cpp.

Definition at line 197 of file blackcalculator.cpp.

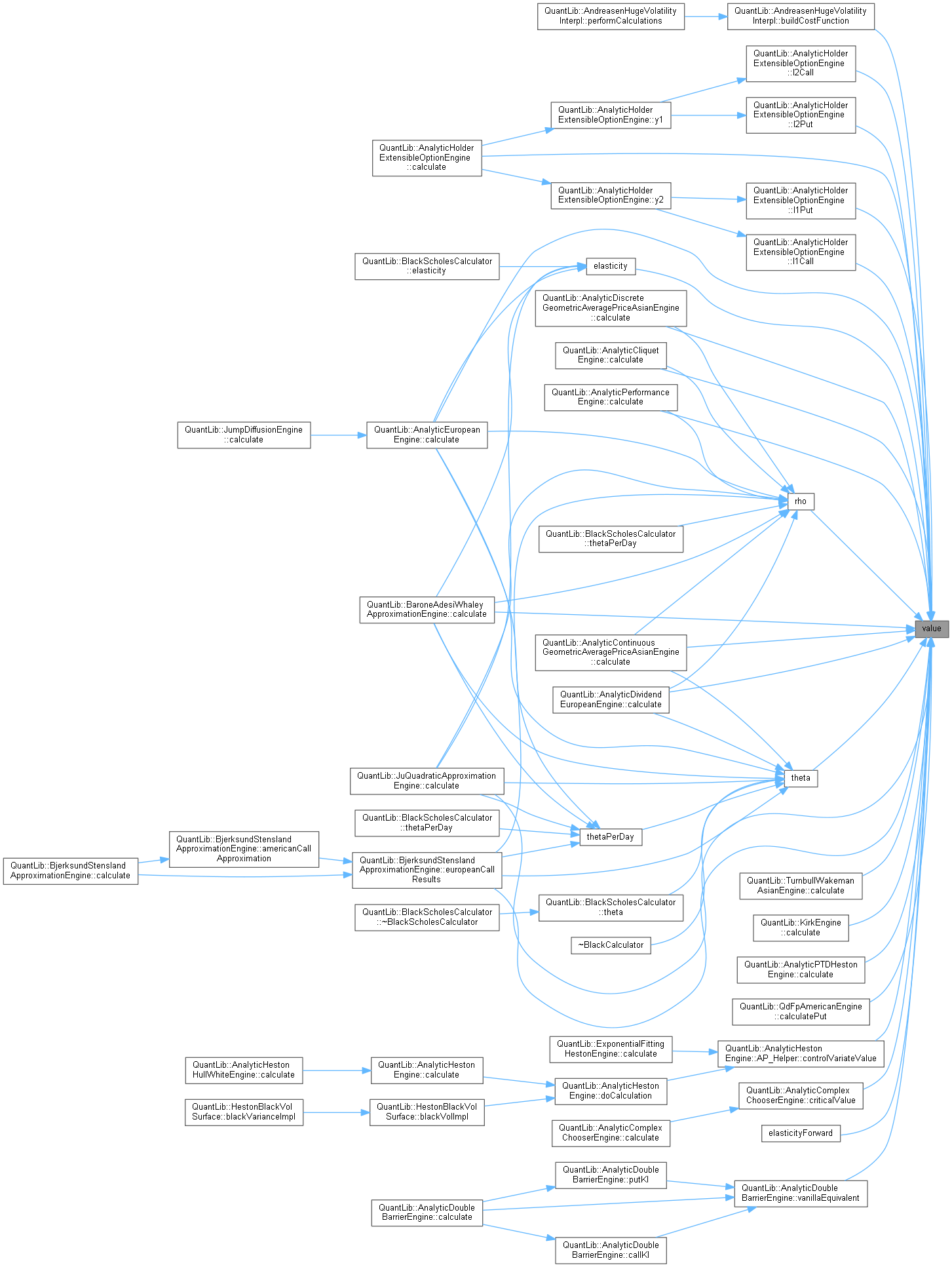

Here is the caller graph for this function:

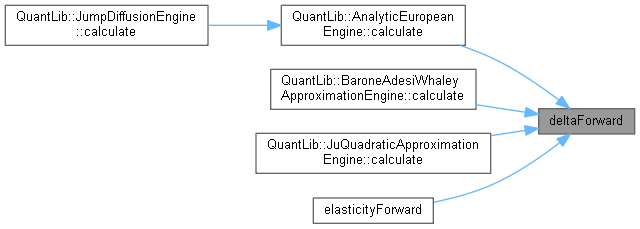

◆ deltaForward()

| Real deltaForward | ( | ) | const |

Sensitivity to change in the underlying forward price.

Definition at line 218 of file blackcalculator.cpp.

Here is the caller graph for this function:

◆ delta()

Sensitivity to change in the underlying spot price.

Reimplemented in BlackScholesCalculator.

Definition at line 202 of file blackcalculator.cpp.

Here is the caller graph for this function:

◆ elasticityForward()

| Real elasticityForward | ( | ) | const |

Sensitivity in percent to a percent change in the underlying forward price.

Definition at line 242 of file blackcalculator.cpp.

Here is the call graph for this function:

◆ elasticity()

Sensitivity in percent to a percent change in the underlying spot price.

Reimplemented in BlackScholesCalculator.

Definition at line 229 of file blackcalculator.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ gammaForward()

| Real gammaForward | ( | ) | const |

Second order derivative with respect to change in the underlying forward price.

Definition at line 275 of file blackcalculator.cpp.

◆ gamma()

Second order derivative with respect to change in the underlying spot price.

Reimplemented in BlackScholesCalculator.

Definition at line 255 of file blackcalculator.cpp.

Here is the caller graph for this function:

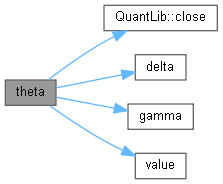

◆ theta()

Sensitivity to time to maturity.

Reimplemented in BlackScholesCalculator.

Definition at line 290 of file blackcalculator.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

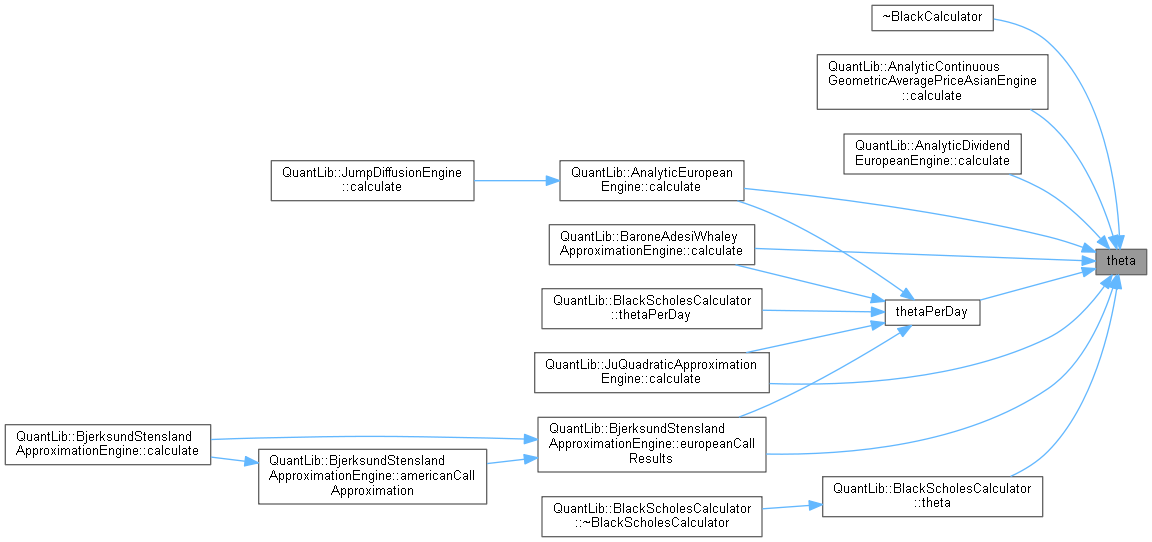

◆ thetaPerDay()

Sensitivity to time to maturity per day, assuming 365 day per year.

Reimplemented in BlackScholesCalculator.

Definition at line 120 of file blackcalculator.hpp.

Here is the caller graph for this function:

◆ vega()

Sensitivity to volatility.

- Examples

- DiscreteHedging.cpp.

Definition at line 301 of file blackcalculator.cpp.

Here is the caller graph for this function:

◆ rho()

Sensitivity to discounting rate.

Definition at line 316 of file blackcalculator.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ dividendRho()

Sensitivity to dividend/growth rate.

Definition at line 328 of file blackcalculator.cpp.

Here is the caller graph for this function:

◆ itmCashProbability()

| Real itmCashProbability | ( | ) | const |

Probability of being in the money in the bond martingale measure, i.e. N(d2). It is a risk-neutral probability, not the real world one.

Definition at line 125 of file blackcalculator.hpp.

Here is the caller graph for this function:

◆ itmAssetProbability()

| Real itmAssetProbability | ( | ) | const |

Probability of being in the money in the asset martingale measure, i.e. N(d1). It is a risk-neutral probability, not the real world one.

Definition at line 129 of file blackcalculator.hpp.

◆ strikeSensitivity()

| Real strikeSensitivity | ( | ) | const |

Sensitivity to strike.

Definition at line 341 of file blackcalculator.cpp.

Here is the caller graph for this function:

◆ strikeGamma()

| Real strikeGamma | ( | ) | const |

gamma w.r.t. strike.

Definition at line 354 of file blackcalculator.cpp.

◆ alpha()

| Real alpha | ( | ) | const |

Definition at line 133 of file blackcalculator.hpp.

◆ beta()

| Real beta | ( | ) | const |

◆ initialize()

|

protected |

Member Data Documentation

◆ strike_

|

protected |

Definition at line 112 of file blackcalculator.hpp.

◆ forward_

|

protected |

Definition at line 112 of file blackcalculator.hpp.

◆ stdDev_

|

protected |

Definition at line 112 of file blackcalculator.hpp.

◆ discount_

|

protected |

Definition at line 112 of file blackcalculator.hpp.

◆ variance_

|

protected |

Definition at line 112 of file blackcalculator.hpp.

◆ d1_

|

protected |

Definition at line 113 of file blackcalculator.hpp.

◆ d2_

|

protected |

Definition at line 113 of file blackcalculator.hpp.

◆ alpha_

|

protected |

Definition at line 114 of file blackcalculator.hpp.

◆ beta_

|

protected |

Definition at line 114 of file blackcalculator.hpp.

◆ DalphaDd1_

|

protected |

Definition at line 114 of file blackcalculator.hpp.

◆ DbetaDd2_

|

protected |

Definition at line 114 of file blackcalculator.hpp.

◆ n_d1_

|

protected |

Definition at line 115 of file blackcalculator.hpp.

◆ cum_d1_

|

protected |

Definition at line 115 of file blackcalculator.hpp.

◆ n_d2_

|

protected |

Definition at line 115 of file blackcalculator.hpp.

◆ cum_d2_

|

protected |

Definition at line 115 of file blackcalculator.hpp.

◆ x_

|

protected |

Definition at line 116 of file blackcalculator.hpp.

◆ DxDs_

|

protected |

Definition at line 116 of file blackcalculator.hpp.

◆ DxDstrike_

|

protected |

Definition at line 116 of file blackcalculator.hpp.