#include <sobolbrownianbridgersg.hpp>

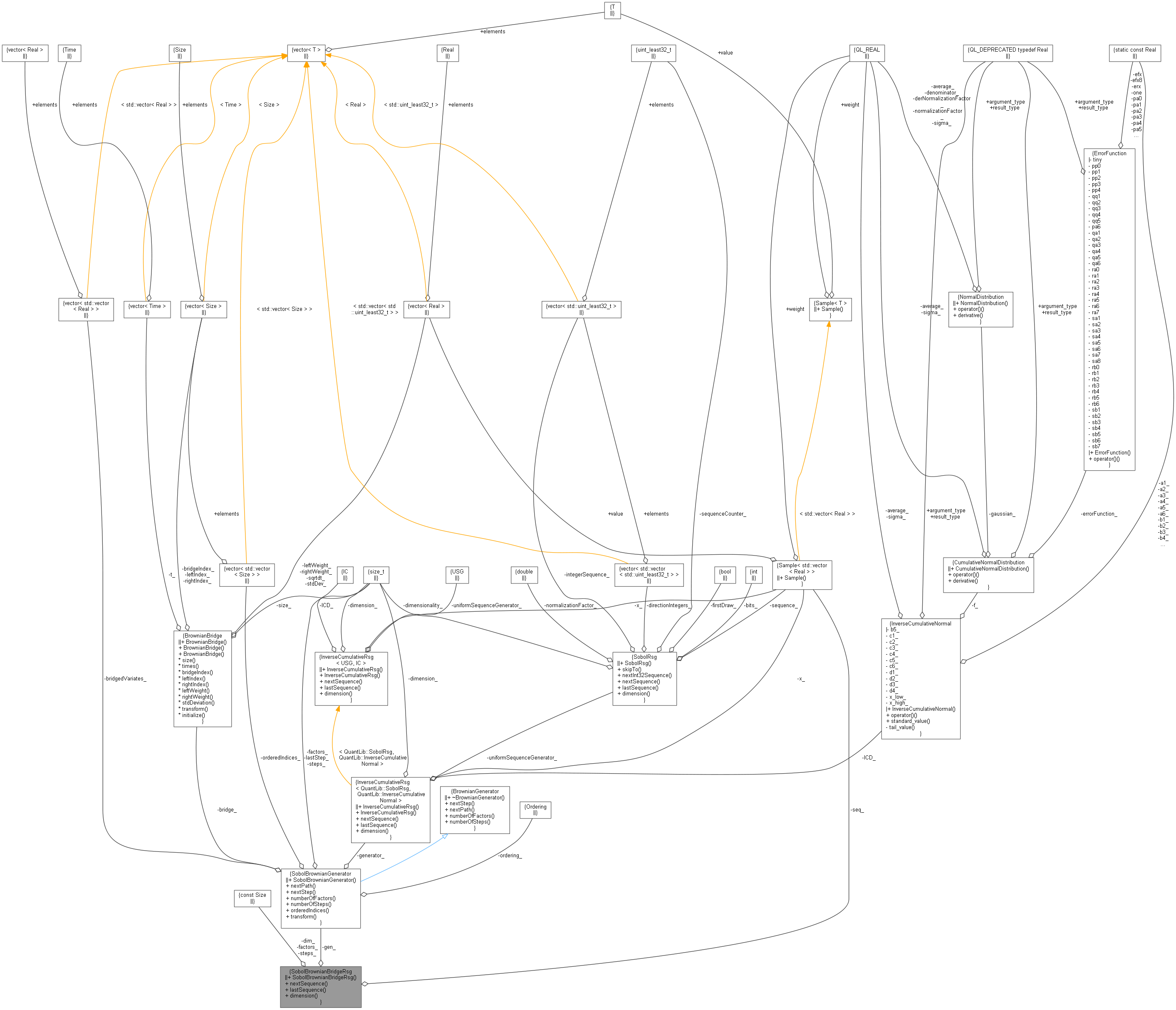

Collaboration diagram for SobolBrownianBridgeRsg:

Collaboration diagram for SobolBrownianBridgeRsg:

Public Types | |

| typedef Sample< std::vector< Real > > | sample_type |

Public Member Functions | |

| SobolBrownianBridgeRsg (Size factors, Size steps, SobolBrownianGenerator::Ordering ordering=SobolBrownianGenerator::Diagonal, unsigned long seed=0, SobolRsg::DirectionIntegers directionIntegers=SobolRsg::JoeKuoD7) | |

| const sample_type & | nextSequence () const |

| const sample_type & | lastSequence () const |

| Size | dimension () const |

Private Attributes | |

| sample_type | seq_ |

| SobolBrownianGenerator | gen_ |

Detailed Description

Definition at line 32 of file sobolbrownianbridgersg.hpp.

Member Typedef Documentation

◆ sample_type

| typedef Sample<std::vector<Real> > sample_type |

Definition at line 34 of file sobolbrownianbridgersg.hpp.

Constructor & Destructor Documentation

◆ SobolBrownianBridgeRsg()

| SobolBrownianBridgeRsg | ( | Size | factors, |

| Size | steps, | ||

| SobolBrownianGenerator::Ordering | ordering = SobolBrownianGenerator::Diagonal, |

||

| unsigned long | seed = 0, |

||

| SobolRsg::DirectionIntegers | directionIntegers = SobolRsg::JoeKuoD7 |

||

| ) |

Definition at line 40 of file sobolbrownianbridgersg.cpp.

Member Function Documentation

◆ nextSequence()

| const SobolBrownianBridgeRsg::sample_type & nextSequence | ( | ) | const |

Definition at line 49 of file sobolbrownianbridgersg.cpp.

◆ lastSequence()

| const SobolBrownianBridgeRsg::sample_type & lastSequence | ( | ) | const |

Definition at line 56 of file sobolbrownianbridgersg.cpp.

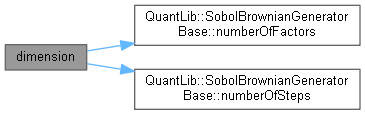

◆ dimension()

| Size dimension | ( | ) | const |

Member Data Documentation

◆ seq_

|

mutableprivate |

Definition at line 48 of file sobolbrownianbridgersg.hpp.

◆ gen_

|

mutableprivate |

Definition at line 49 of file sobolbrownianbridgersg.hpp.