Iteration scheme for fixed-point QD American engine. More...

#include <qdfpamericanengine.hpp>

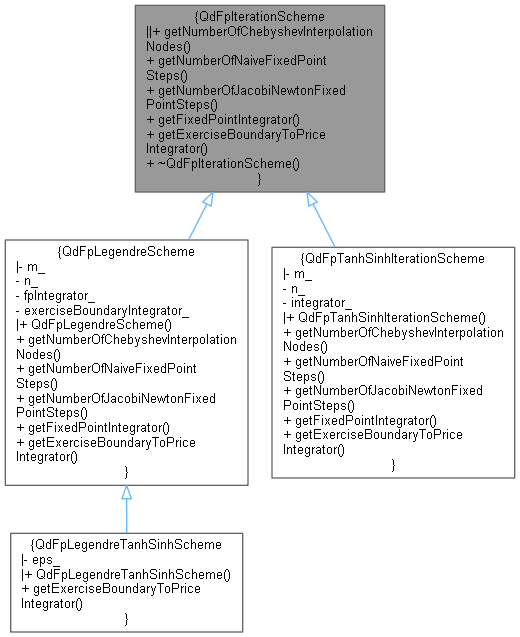

Inheritance diagram for QdFpIterationScheme:

Inheritance diagram for QdFpIterationScheme: Collaboration diagram for QdFpIterationScheme:

Collaboration diagram for QdFpIterationScheme:

Public Member Functions | |

| virtual Size | getNumberOfChebyshevInterpolationNodes () const =0 |

| virtual Size | getNumberOfNaiveFixedPointSteps () const =0 |

| virtual Size | getNumberOfJacobiNewtonFixedPointSteps () const =0 |

| virtual ext::shared_ptr< Integrator > | getFixedPointIntegrator () const =0 |

| virtual ext::shared_ptr< Integrator > | getExerciseBoundaryToPriceIntegrator () const =0 |

| virtual | ~QdFpIterationScheme ()=default |

Detailed Description

Iteration scheme for fixed-point QD American engine.

Definition at line 33 of file qdfpamericanengine.hpp.

Constructor & Destructor Documentation

◆ ~QdFpIterationScheme()

|

virtualdefault |

Member Function Documentation

◆ getNumberOfChebyshevInterpolationNodes()

|

pure virtual |

Implemented in QdFpLegendreScheme, and QdFpTanhSinhIterationScheme.

◆ getNumberOfNaiveFixedPointSteps()

|

pure virtual |

Implemented in QdFpLegendreScheme, and QdFpTanhSinhIterationScheme.

◆ getNumberOfJacobiNewtonFixedPointSteps()

|

pure virtual |

Implemented in QdFpLegendreScheme, and QdFpTanhSinhIterationScheme.

◆ getFixedPointIntegrator()

|

pure virtual |

Implemented in QdFpLegendreScheme, and QdFpTanhSinhIterationScheme.

◆ getExerciseBoundaryToPriceIntegrator()

|

pure virtual |

Implemented in QdFpLegendreScheme, QdFpLegendreTanhSinhScheme, and QdFpTanhSinhIterationScheme.