#include <fdcevvanillaengine.hpp>

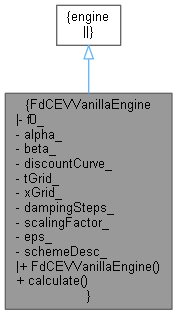

Inheritance diagram for FdCEVVanillaEngine:

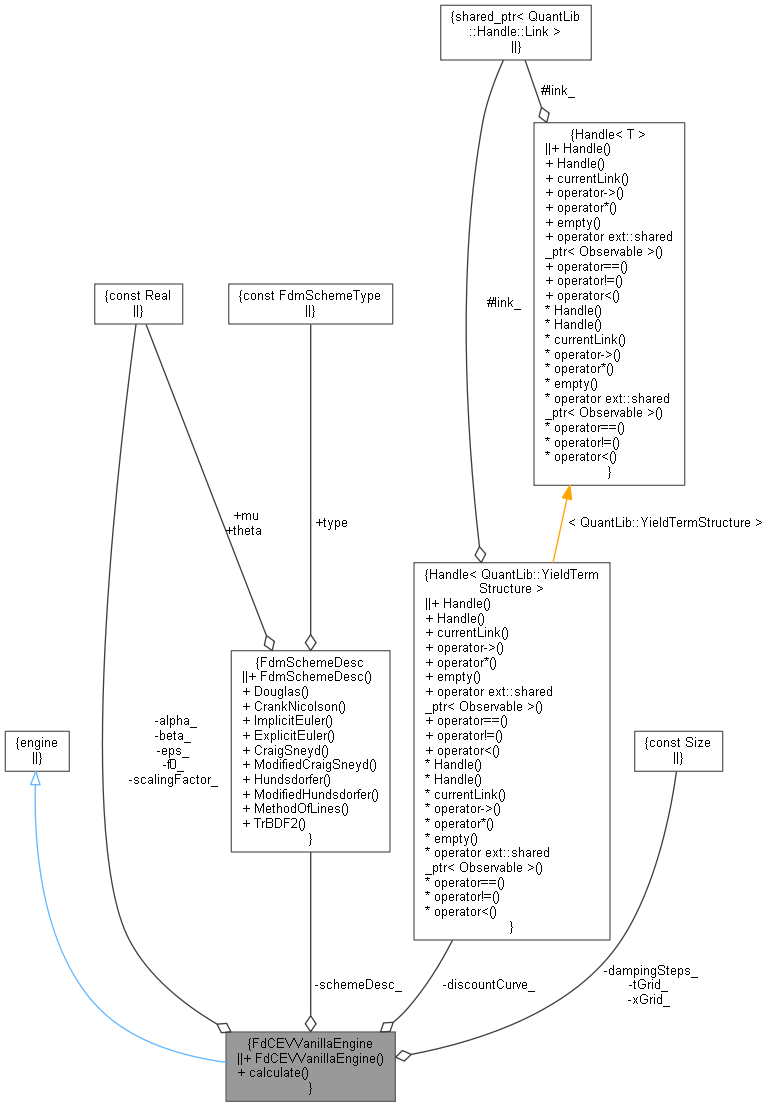

Inheritance diagram for FdCEVVanillaEngine: Collaboration diagram for FdCEVVanillaEngine:

Collaboration diagram for FdCEVVanillaEngine:

Public Member Functions | |

| FdCEVVanillaEngine (Real f0, Real alpha, Real beta, Handle< YieldTermStructure > discountCurve, Size tGrid=50, Size xGrid=400, Size dampingSteps=0, Real scalingFactor=1.0, Real eps=1e-4, const FdmSchemeDesc &schemeDesc=FdmSchemeDesc::Douglas()) | |

| void | calculate () const override |

Private Attributes | |

| const Real | f0_ |

| const Real | alpha_ |

| const Real | beta_ |

| const Handle< YieldTermStructure > | discountCurve_ |

| const Size | tGrid_ |

| const Size | xGrid_ |

| const Size | dampingSteps_ |

| const Real | scalingFactor_ |

| const Real | eps_ |

| const FdmSchemeDesc | schemeDesc_ |

Detailed Description

Definition at line 34 of file fdcevvanillaengine.hpp.

Constructor & Destructor Documentation

◆ FdCEVVanillaEngine()

| FdCEVVanillaEngine | ( | Real | f0, |

| Real | alpha, | ||

| Real | beta, | ||

| Handle< YieldTermStructure > | discountCurve, | ||

| Size | tGrid = 50, |

||

| Size | xGrid = 400, |

||

| Size | dampingSteps = 0, |

||

| Real | scalingFactor = 1.0, |

||

| Real | eps = 1e-4, |

||

| const FdmSchemeDesc & | schemeDesc = FdmSchemeDesc::Douglas() |

||

| ) |

Definition at line 69 of file fdcevvanillaengine.cpp.

Member Function Documentation

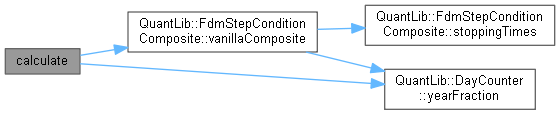

◆ calculate()

|

override |

Member Data Documentation

◆ f0_

|

private |

Definition at line 50 of file fdcevvanillaengine.hpp.

◆ alpha_

|

private |

Definition at line 50 of file fdcevvanillaengine.hpp.

◆ beta_

|

private |

Definition at line 50 of file fdcevvanillaengine.hpp.

◆ discountCurve_

|

private |

Definition at line 51 of file fdcevvanillaengine.hpp.

◆ tGrid_

|

private |

Definition at line 52 of file fdcevvanillaengine.hpp.

◆ xGrid_

|

private |

Definition at line 52 of file fdcevvanillaengine.hpp.

◆ dampingSteps_

|

private |

Definition at line 52 of file fdcevvanillaengine.hpp.

◆ scalingFactor_

|

private |

Definition at line 53 of file fdcevvanillaengine.hpp.

◆ eps_

|

private |

Definition at line 53 of file fdcevvanillaengine.hpp.

◆ schemeDesc_

|

private |

Definition at line 54 of file fdcevvanillaengine.hpp.