#include <cotswaptofwdadapter.hpp>

Inheritance diagram for CotSwapToFwdAdapter:

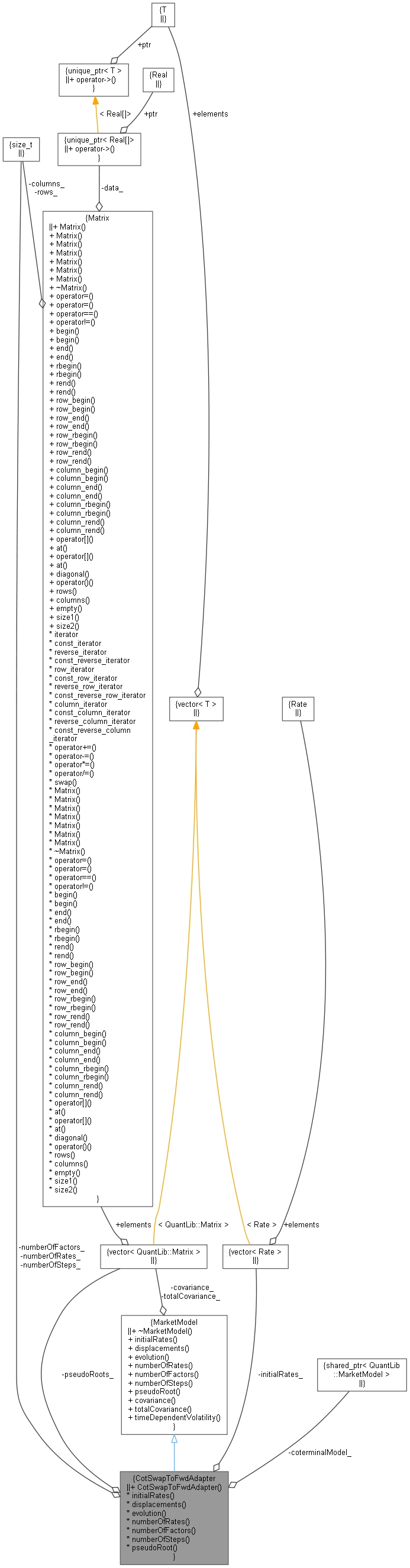

Inheritance diagram for CotSwapToFwdAdapter: Collaboration diagram for CotSwapToFwdAdapter:

Collaboration diagram for CotSwapToFwdAdapter:

Public Member Functions | |

| CotSwapToFwdAdapter (const ext::shared_ptr< MarketModel > &coterminalModel) | |

| Public Member Functions inherited from MarketModel | |

| virtual | ~MarketModel ()=default |

| virtual const std::vector< Rate > & | initialRates () const =0 |

| virtual const std::vector< Spread > & | displacements () const =0 |

| virtual const EvolutionDescription & | evolution () const =0 |

| virtual Size | numberOfRates () const =0 |

| virtual Size | numberOfFactors () const =0 |

| virtual Size | numberOfSteps () const =0 |

| virtual const Matrix & | pseudoRoot (Size i) const =0 |

| virtual const Matrix & | covariance (Size i) const |

| virtual const Matrix & | totalCovariance (Size endIndex) const |

| std::vector< Volatility > | timeDependentVolatility (Size i) const |

MarketModel interface | |

| ext::shared_ptr< MarketModel > | coterminalModel_ |

| Size | numberOfFactors_ |

| Size | numberOfRates_ |

| Size | numberOfSteps_ |

| std::vector< Rate > | initialRates_ |

| std::vector< Matrix > | pseudoRoots_ |

| const std::vector< Rate > & | initialRates () const override |

| const std::vector< Spread > & | displacements () const override |

| const EvolutionDescription & | evolution () const override |

| Size | numberOfRates () const override |

| Size | numberOfFactors () const override |

| Size | numberOfSteps () const override |

| const Matrix & | pseudoRoot (Size i) const override |

Detailed Description

Definition at line 31 of file cotswaptofwdadapter.hpp.

Constructor & Destructor Documentation

◆ CotSwapToFwdAdapter()

| CotSwapToFwdAdapter | ( | const ext::shared_ptr< MarketModel > & | coterminalModel | ) |

Member Function Documentation

◆ initialRates()

|

overridevirtual |

Implements MarketModel.

Definition at line 70 of file cotswaptofwdadapter.hpp.

◆ displacements()

|

overridevirtual |

Implements MarketModel.

Definition at line 75 of file cotswaptofwdadapter.hpp.

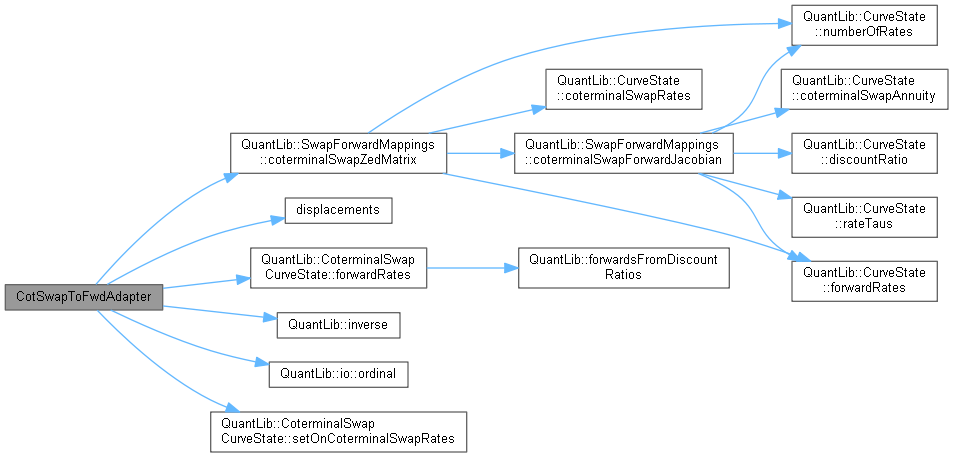

Here is the caller graph for this function:

◆ evolution()

|

overridevirtual |

Implements MarketModel.

Definition at line 80 of file cotswaptofwdadapter.hpp.

◆ numberOfRates()

|

overridevirtual |

Implements MarketModel.

Definition at line 84 of file cotswaptofwdadapter.hpp.

◆ numberOfFactors()

|

overridevirtual |

Implements MarketModel.

Definition at line 88 of file cotswaptofwdadapter.hpp.

◆ numberOfSteps()

|

overridevirtual |

Implements MarketModel.

Definition at line 92 of file cotswaptofwdadapter.hpp.

◆ pseudoRoot()

Implements MarketModel.

Definition at line 96 of file cotswaptofwdadapter.hpp.

Member Data Documentation

◆ coterminalModel_

|

private |

Definition at line 46 of file cotswaptofwdadapter.hpp.

◆ numberOfFactors_

|

private |

Definition at line 47 of file cotswaptofwdadapter.hpp.

◆ numberOfRates_

|

private |

Definition at line 47 of file cotswaptofwdadapter.hpp.

◆ numberOfSteps_

|

private |

Definition at line 47 of file cotswaptofwdadapter.hpp.

◆ initialRates_

|

private |

Definition at line 48 of file cotswaptofwdadapter.hpp.

◆ pseudoRoots_

|

private |

Definition at line 49 of file cotswaptofwdadapter.hpp.