Results from single-asset option calculation More...

#include <oneassetoption.hpp>

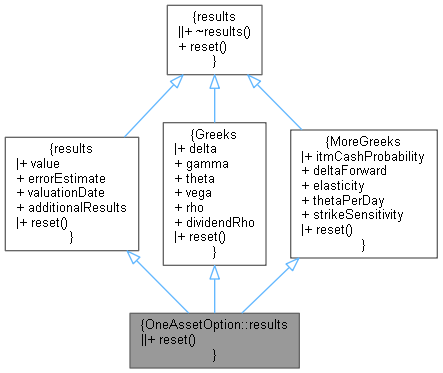

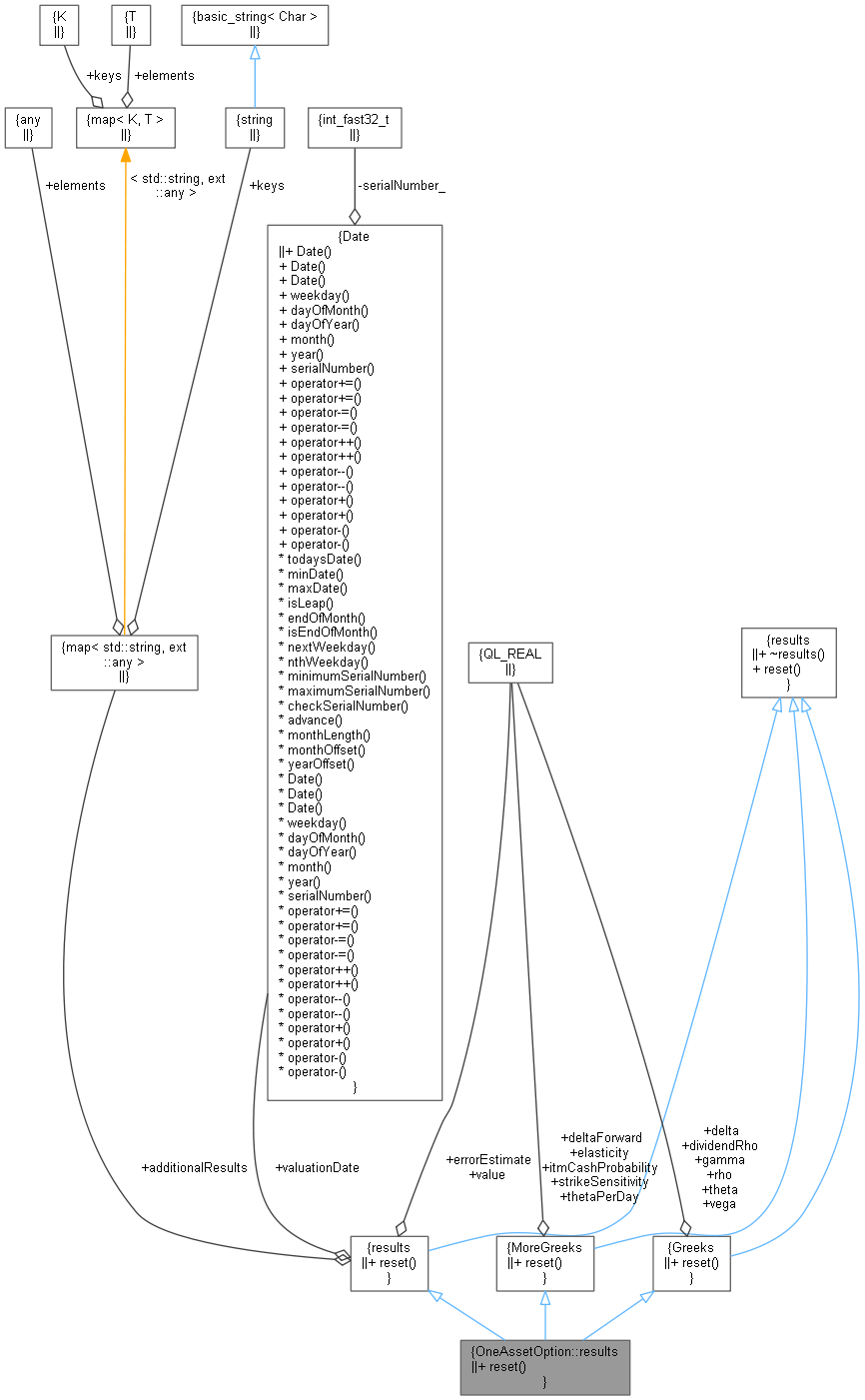

Inheritance diagram for OneAssetOption::results:

Inheritance diagram for OneAssetOption::results: Collaboration diagram for OneAssetOption::results:

Collaboration diagram for OneAssetOption::results:

Public Member Functions | |

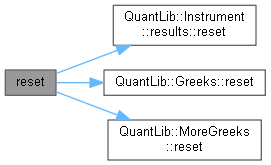

| void | reset () override |

| void | reset () override |

| Public Member Functions inherited from PricingEngine::results | |

| virtual | ~results ()=default |

| virtual void | reset ()=0 |

| Public Member Functions inherited from Greeks | |

| void | reset () override |

| Public Member Functions inherited from MoreGreeks | |

| void | reset () override |

Additional Inherited Members | |

| Public Attributes inherited from Instrument::results | |

| Real | value |

| Real | errorEstimate |

| Date | valuationDate |

| std::map< std::string, ext::any > | additionalResults |

| Public Attributes inherited from Greeks | |

| Real | delta |

| Real | gamma |

| Real | theta |

| Real | vega |

| Real | rho |

| Real | dividendRho |

| Public Attributes inherited from MoreGreeks | |

| Real | itmCashProbability |

| Real | deltaForward |

| Real | elasticity |

| Real | thetaPerDay |

| Real | strikeSensitivity |

Detailed Description

Results from single-asset option calculation

Definition at line 69 of file oneassetoption.hpp.

Member Function Documentation

◆ reset()

|

overridevirtual |

Reimplemented from Instrument::results.

Definition at line 73 of file oneassetoption.hpp.

Here is the call graph for this function: