#include <lsstrategy.hpp>

Inheritance diagram for LongstaffSchwartzExerciseStrategy:

Inheritance diagram for LongstaffSchwartzExerciseStrategy: Collaboration diagram for LongstaffSchwartzExerciseStrategy:

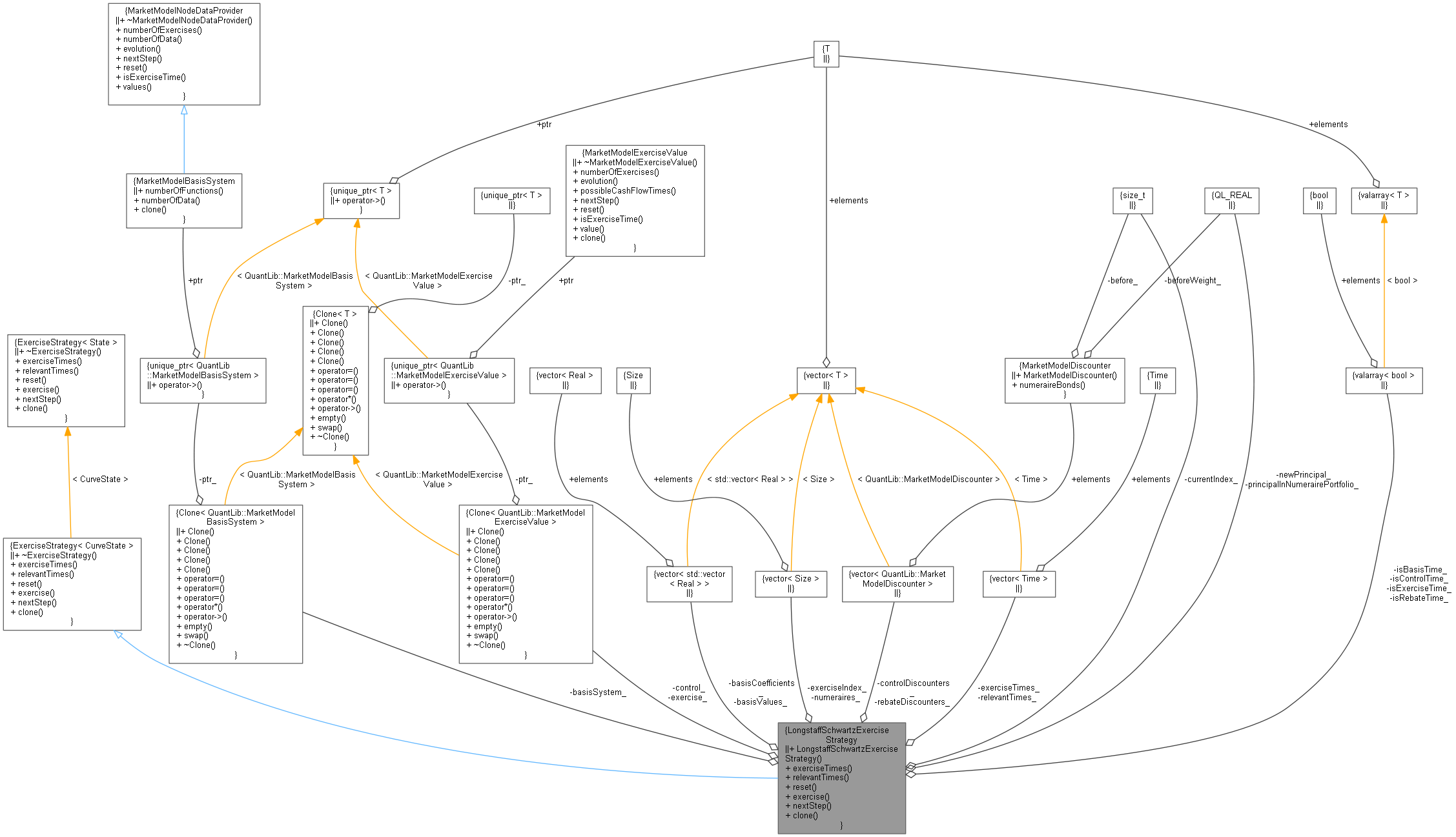

Collaboration diagram for LongstaffSchwartzExerciseStrategy:

Public Member Functions | |

| LongstaffSchwartzExerciseStrategy (Clone< MarketModelBasisSystem > basisSystem, std::vector< std::vector< Real > > basisCoefficients, const EvolutionDescription &evolution, const std::vector< Size > &numeraires, Clone< MarketModelExerciseValue > exercise, Clone< MarketModelExerciseValue > control) | |

| std::vector< Time > | exerciseTimes () const override |

| std::vector< Time > | relevantTimes () const override |

| void | reset () override |

| bool | exercise (const CurveState ¤tState) const override |

| void | nextStep (const CurveState ¤tState) override |

| std::unique_ptr< ExerciseStrategy< CurveState > > | clone () const override |

| Public Member Functions inherited from ExerciseStrategy< CurveState > | |

| virtual | ~ExerciseStrategy ()=default |

| virtual std::vector< Time > | exerciseTimes () const=0 |

| virtual std::vector< Time > | relevantTimes () const=0 |

| virtual void | reset ()=0 |

| virtual bool | exercise (const CurveState ¤tState) const=0 |

| virtual void | nextStep (const CurveState ¤tState)=0 |

| virtual std::unique_ptr< ExerciseStrategy< CurveState > > | clone () const=0 |

Private Attributes | |

| Clone< MarketModelBasisSystem > | basisSystem_ |

| std::vector< std::vector< Real > > | basisCoefficients_ |

| Clone< MarketModelExerciseValue > | exercise_ |

| Clone< MarketModelExerciseValue > | control_ |

| std::vector< Size > | numeraires_ |

| Size | currentIndex_ |

| Real | principalInNumerairePortfolio_ |

| Real | newPrincipal_ |

| std::vector< Time > | exerciseTimes_ |

| std::vector< Time > | relevantTimes_ |

| std::valarray< bool > | isBasisTime_ |

| std::valarray< bool > | isRebateTime_ |

| std::valarray< bool > | isControlTime_ |

| std::valarray< bool > | isExerciseTime_ |

| std::vector< MarketModelDiscounter > | rebateDiscounters_ |

| std::vector< MarketModelDiscounter > | controlDiscounters_ |

| std::vector< std::vector< Real > > | basisValues_ |

| std::vector< Size > | exerciseIndex_ |

Detailed Description

- Examples

- MarketModels.cpp.

Definition at line 32 of file lsstrategy.hpp.

Constructor & Destructor Documentation

◆ LongstaffSchwartzExerciseStrategy()

| LongstaffSchwartzExerciseStrategy | ( | Clone< MarketModelBasisSystem > | basisSystem, |

| std::vector< std::vector< Real > > | basisCoefficients, | ||

| const EvolutionDescription & | evolution, | ||

| const std::vector< Size > & | numeraires, | ||

| Clone< MarketModelExerciseValue > | exercise, | ||

| Clone< MarketModelExerciseValue > | control | ||

| ) |

Member Function Documentation

◆ exerciseTimes()

|

overridevirtual |

Implements ExerciseStrategy< CurveState >.

Definition at line 88 of file lsstrategy.cpp.

◆ relevantTimes()

|

overridevirtual |

Implements ExerciseStrategy< CurveState >.

Definition at line 93 of file lsstrategy.cpp.

◆ reset()

|

overridevirtual |

Implements ExerciseStrategy< CurveState >.

Definition at line 97 of file lsstrategy.cpp.

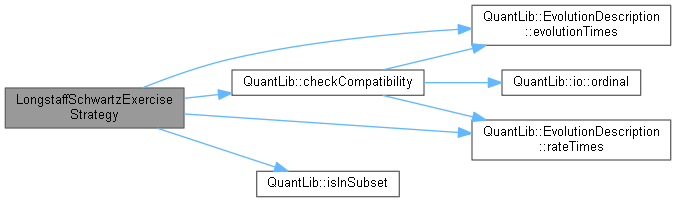

◆ exercise()

|

overridevirtual |

Implements ExerciseStrategy< CurveState >.

Definition at line 105 of file lsstrategy.cpp.

Here is the call graph for this function:

◆ nextStep()

|

overridevirtual |

Implements ExerciseStrategy< CurveState >.

Definition at line 136 of file lsstrategy.cpp.

Here is the call graph for this function:

◆ clone()

|

overridevirtual |

Implements ExerciseStrategy< CurveState >.

Definition at line 158 of file lsstrategy.cpp.

Member Data Documentation

◆ basisSystem_

|

private |

Definition at line 48 of file lsstrategy.hpp.

◆ basisCoefficients_

|

private |

Definition at line 49 of file lsstrategy.hpp.

◆ exercise_

|

private |

Definition at line 50 of file lsstrategy.hpp.

◆ control_

|

private |

Definition at line 51 of file lsstrategy.hpp.

◆ numeraires_

|

private |

Definition at line 52 of file lsstrategy.hpp.

◆ currentIndex_

|

private |

Definition at line 54 of file lsstrategy.hpp.

◆ principalInNumerairePortfolio_

|

private |

Definition at line 55 of file lsstrategy.hpp.

◆ newPrincipal_

|

private |

Definition at line 55 of file lsstrategy.hpp.

◆ exerciseTimes_

|

private |

Definition at line 56 of file lsstrategy.hpp.

◆ relevantTimes_

|

private |

Definition at line 56 of file lsstrategy.hpp.

◆ isBasisTime_

|

private |

Definition at line 57 of file lsstrategy.hpp.

◆ isRebateTime_

|

private |

Definition at line 57 of file lsstrategy.hpp.

◆ isControlTime_

|

private |

Definition at line 57 of file lsstrategy.hpp.

◆ isExerciseTime_

|

private |

Definition at line 58 of file lsstrategy.hpp.

◆ rebateDiscounters_

|

private |

Definition at line 59 of file lsstrategy.hpp.

◆ controlDiscounters_

|

private |

Definition at line 60 of file lsstrategy.hpp.

◆ basisValues_

|

mutableprivate |

Definition at line 61 of file lsstrategy.hpp.

◆ exerciseIndex_

|

private |

Definition at line 62 of file lsstrategy.hpp.