#include <multistepswaption.hpp>

Inheritance diagram for MultiStepSwaption:

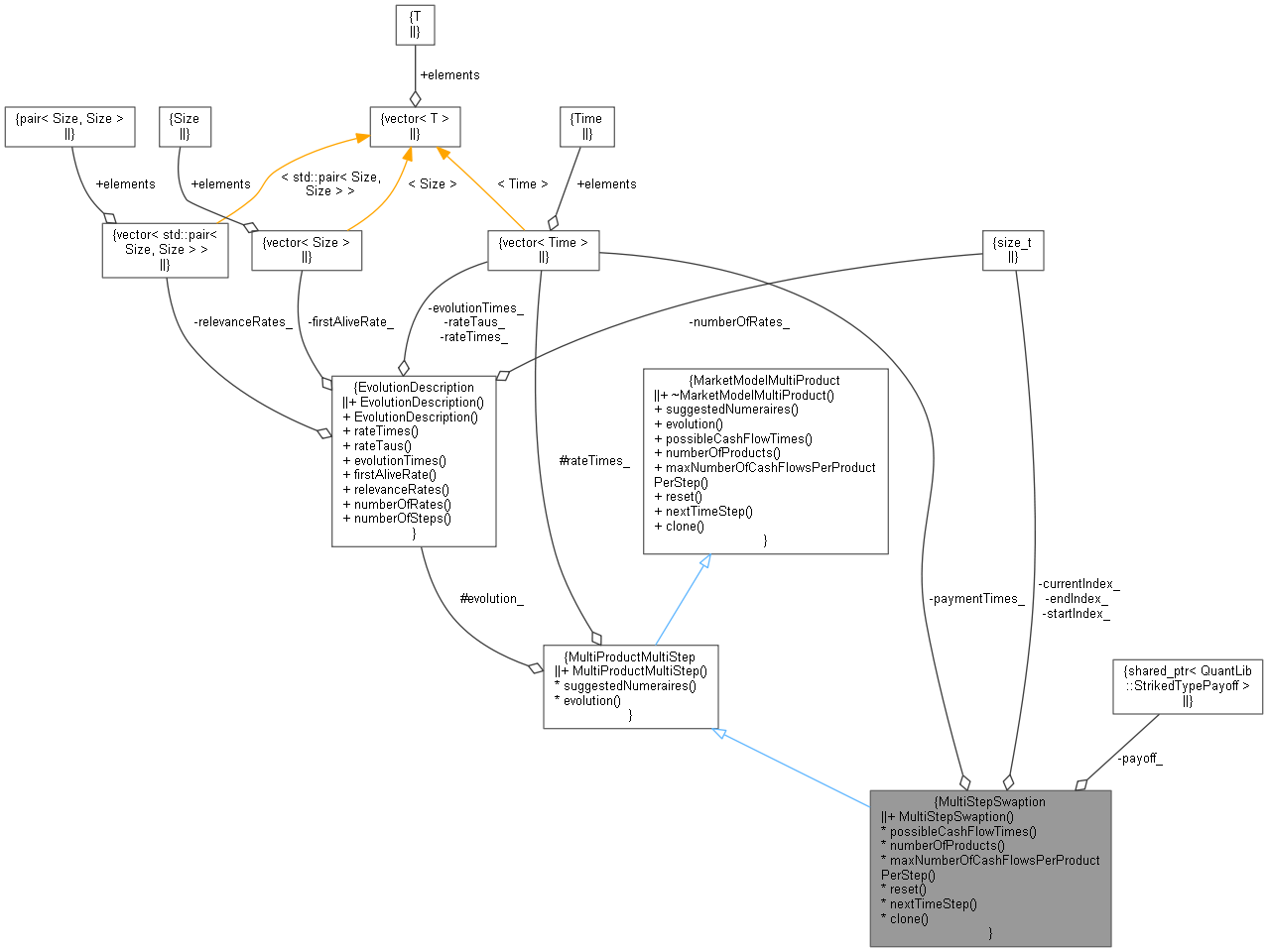

Inheritance diagram for MultiStepSwaption: Collaboration diagram for MultiStepSwaption:

Collaboration diagram for MultiStepSwaption:

Public Member Functions | |

| MultiStepSwaption (const std::vector< Time > &rateTimes, Size startIndex, Size endIndex, ext::shared_ptr< StrikedTypePayoff > &) | |

| Public Member Functions inherited from MultiProductMultiStep | |

| MultiProductMultiStep (std::vector< Time > rateTimes) | |

| std::vector< Size > | suggestedNumeraires () const override |

| const EvolutionDescription & | evolution () const override |

| Public Member Functions inherited from MarketModelMultiProduct | |

| virtual | ~MarketModelMultiProduct ()=default |

| virtual std::vector< Size > | suggestedNumeraires () const =0 |

| virtual const EvolutionDescription & | evolution () const =0 |

| virtual std::vector< Time > | possibleCashFlowTimes () const =0 |

| virtual Size | numberOfProducts () const =0 |

| virtual Size | maxNumberOfCashFlowsPerProductPerStep () const =0 |

| virtual void | reset ()=0 |

| during simulation put product at start of path More... | |

| virtual bool | nextTimeStep (const CurveState ¤tState, std::vector< Size > &numberCashFlowsThisStep, std::vector< std::vector< CashFlow > > &cashFlowsGenerated)=0 |

| return value indicates whether path is finished, TRUE means done More... | |

| virtual std::unique_ptr< MarketModelMultiProduct > | clone () const =0 |

| returns a newly-allocated copy of itself More... | |

MarketModelMultiProduct interface | |

| Size | startIndex_ |

| Size | endIndex_ |

| ext::shared_ptr< StrikedTypePayoff > | payoff_ |

| std::vector< Time > | paymentTimes_ |

| Size | currentIndex_ |

| std::vector< Time > | possibleCashFlowTimes () const override |

| Size | numberOfProducts () const override |

| Size | maxNumberOfCashFlowsPerProductPerStep () const override |

| void | reset () override |

| during simulation put product at start of path More... | |

| bool | nextTimeStep (const CurveState ¤tState, std::vector< Size > &numberCashFlowsThisStep, std::vector< std::vector< CashFlow > > &cashFlowsGenerated) override |

| return value indicates whether path is finished, TRUE means done More... | |

| std::unique_ptr< MarketModelMultiProduct > | clone () const override |

| returns a newly-allocated copy of itself More... | |

Additional Inherited Members | |

| Protected Attributes inherited from MultiProductMultiStep | |

| std::vector< Time > | rateTimes_ |

| EvolutionDescription | evolution_ |

Detailed Description

Price a swaption associated to a contiguous subset of rates. Useful only for testing purposes. Steps through all rate times up to start of swap.

Definition at line 36 of file multistepswaption.hpp.

Constructor & Destructor Documentation

◆ MultiStepSwaption()

| MultiStepSwaption | ( | const std::vector< Time > & | rateTimes, |

| Size | startIndex, | ||

| Size | endIndex, | ||

| ext::shared_ptr< StrikedTypePayoff > & | payOff | ||

| ) |

Definition at line 28 of file multistepswaption.cpp.

Member Function Documentation

◆ possibleCashFlowTimes()

|

overridevirtual |

Implements MarketModelMultiProduct.

Definition at line 67 of file multistepswaption.hpp.

◆ numberOfProducts()

|

overridevirtual |

Implements MarketModelMultiProduct.

Definition at line 72 of file multistepswaption.hpp.

◆ maxNumberOfCashFlowsPerProductPerStep()

|

overridevirtual |

Implements MarketModelMultiProduct.

Definition at line 77 of file multistepswaption.hpp.

◆ reset()

|

overridevirtual |

during simulation put product at start of path

Implements MarketModelMultiProduct.

Definition at line 81 of file multistepswaption.hpp.

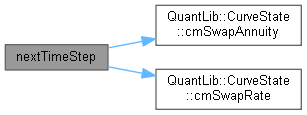

◆ nextTimeStep()

|

overridevirtual |

return value indicates whether path is finished, TRUE means done

Implements MarketModelMultiProduct.

Definition at line 42 of file multistepswaption.cpp.

Here is the call graph for this function:

◆ clone()

|

overridevirtual |

returns a newly-allocated copy of itself

Implements MarketModelMultiProduct.

Definition at line 72 of file multistepswaption.cpp.

Member Data Documentation

◆ startIndex_

|

private |

Definition at line 56 of file multistepswaption.hpp.

◆ endIndex_

|

private |

Definition at line 57 of file multistepswaption.hpp.

◆ payoff_

|

private |

Definition at line 58 of file multistepswaption.hpp.

◆ paymentTimes_

|

private |

Definition at line 59 of file multistepswaption.hpp.

◆ currentIndex_

|

private |

Definition at line 61 of file multistepswaption.hpp.