base class for market-model factories More...

#include <marketmodel.hpp>

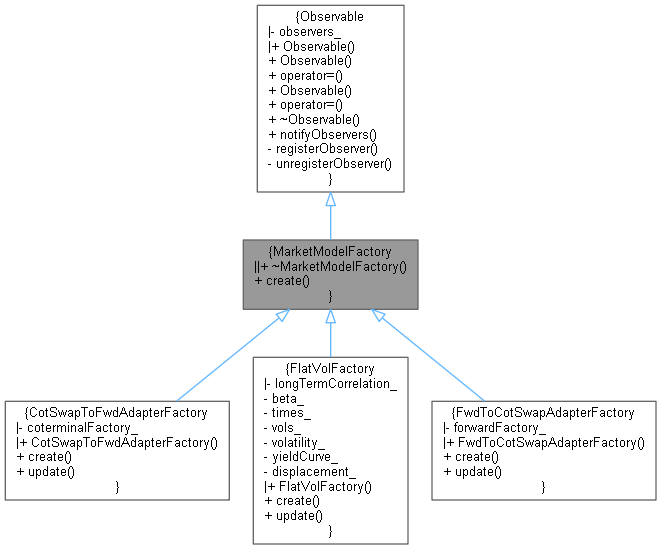

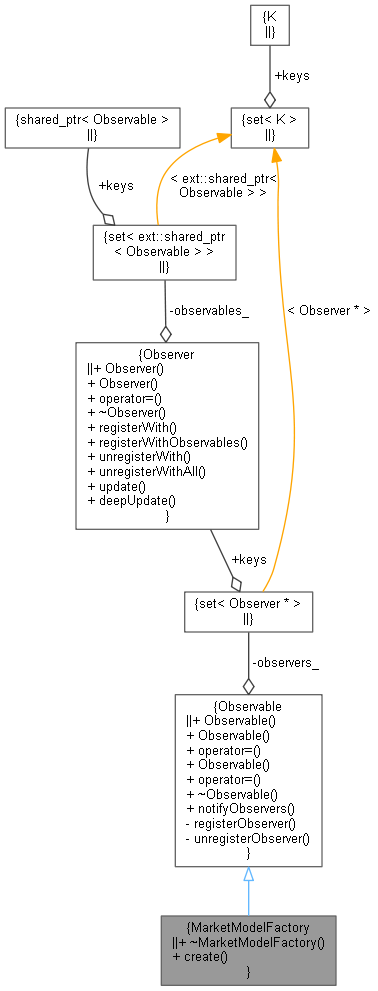

Inheritance diagram for MarketModelFactory:

Inheritance diagram for MarketModelFactory: Collaboration diagram for MarketModelFactory:

Collaboration diagram for MarketModelFactory:

Public Member Functions | |

| ~MarketModelFactory () override=default | |

| virtual ext::shared_ptr< MarketModel > | create (const EvolutionDescription &, Size numberOfFactors) const =0 |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

Detailed Description

base class for market-model factories

Definition at line 57 of file marketmodel.hpp.

Constructor & Destructor Documentation

◆ ~MarketModelFactory()

|

overridedefault |

Member Function Documentation

◆ create()

|

pure virtual |

Implemented in CotSwapToFwdAdapterFactory, FlatVolFactory, and FwdToCotSwapAdapterFactory.