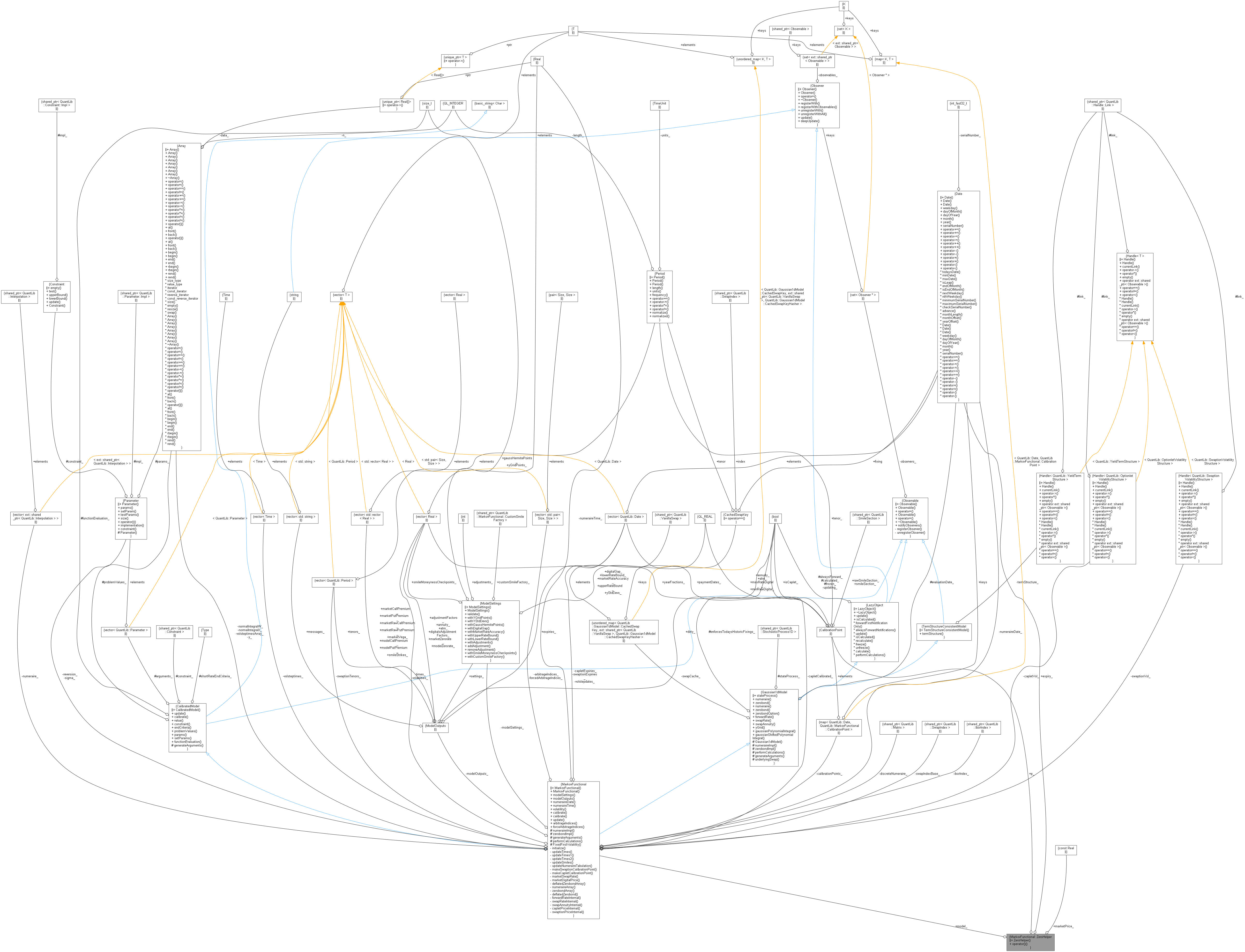

Collaboration diagram for MarkovFunctional::ZeroHelper:

Collaboration diagram for MarkovFunctional::ZeroHelper:

Public Member Functions | |

| ZeroHelper (const MarkovFunctional *model, const Date &expiry, const CalibrationPoint &p, const Real marketPrice) | |

| Real | operator() (Real strike) const |

Public Attributes | |

| const MarkovFunctional * | model_ |

| const Real | marketPrice_ |

| const Date & | expiry_ |

| const CalibrationPoint & | p_ |

Detailed Description

Definition at line 480 of file markovfunctional.hpp.

Constructor & Destructor Documentation

◆ ZeroHelper()

| ZeroHelper | ( | const MarkovFunctional * | model, |

| const Date & | expiry, | ||

| const CalibrationPoint & | p, | ||

| const Real | marketPrice | ||

| ) |

Definition at line 482 of file markovfunctional.hpp.

Member Function Documentation

◆ operator()()

Member Data Documentation

◆ model_

| const MarkovFunctional* model_ |

Definition at line 491 of file markovfunctional.hpp.

◆ marketPrice_

| const Real marketPrice_ |

Definition at line 492 of file markovfunctional.hpp.

◆ expiry_

| const Date& expiry_ |

Definition at line 493 of file markovfunctional.hpp.

◆ p_

| const CalibrationPoint& p_ |

Definition at line 494 of file markovfunctional.hpp.