Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Linear Gauss Markov Model Parameters. More...

#include <ored/model/lgmdata.hpp>

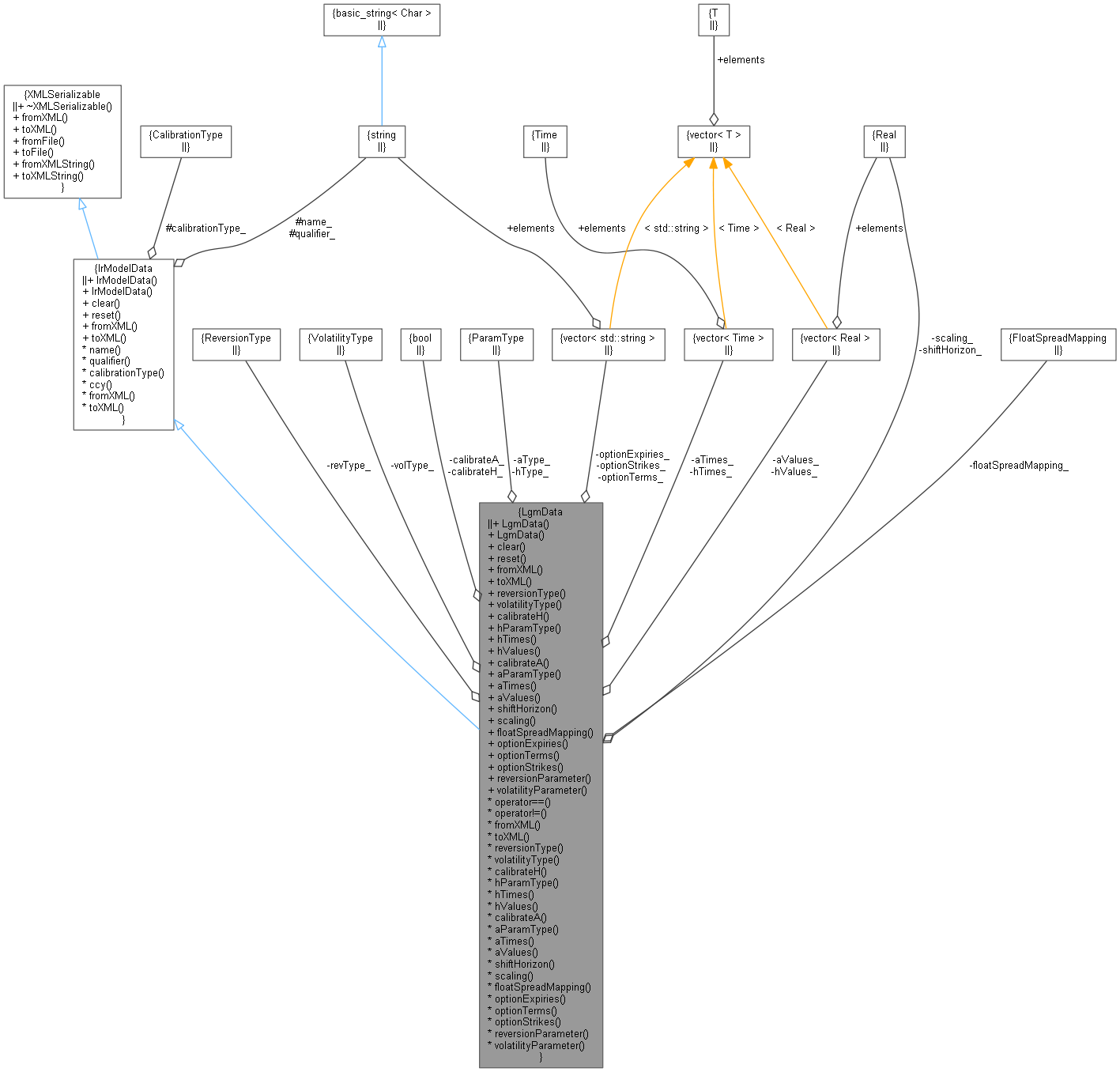

Inheritance diagram for LgmData: Collaboration diagram for LgmData:

Inheritance diagram for LgmData: Collaboration diagram for LgmData:Public Types | |

| enum class | ReversionType { HullWhite , Hagan } |

| Supported mean reversion types. More... | |

| enum class | VolatilityType { HullWhite , Hagan } |

| Supported volatility types. More... | |

Public Member Functions | |

| LgmData () | |

| Default constructor. More... | |

| LgmData (std::string qualifier, CalibrationType calibrationType, ReversionType revType, VolatilityType volType, bool calibrateH, ParamType hType, std::vector< Time > hTimes, std::vector< Real > hValues, bool calibrateA, ParamType aType, std::vector< Time > aTimes, std::vector< Real > aValues, Real shiftHorizon=0.0, Real scaling=1.0, std::vector< std::string > optionExpiries=std::vector< std::string >(), std::vector< std::string > optionTerms=std::vector< std::string >(), std::vector< std::string > optionStrikes=std::vector< std::string >(), const QuantExt::AnalyticLgmSwaptionEngine::FloatSpreadMapping inputFloatSpreadMapping=QuantExt::AnalyticLgmSwaptionEngine::proRata) | |

| Detailed constructor. More... | |

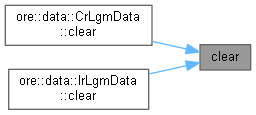

| void | clear () override |

| Clear list of calibration instruments. More... | |

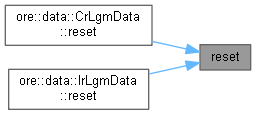

| void | reset () override |

| Reset member variables to defaults. More... | |

Serialisation | |

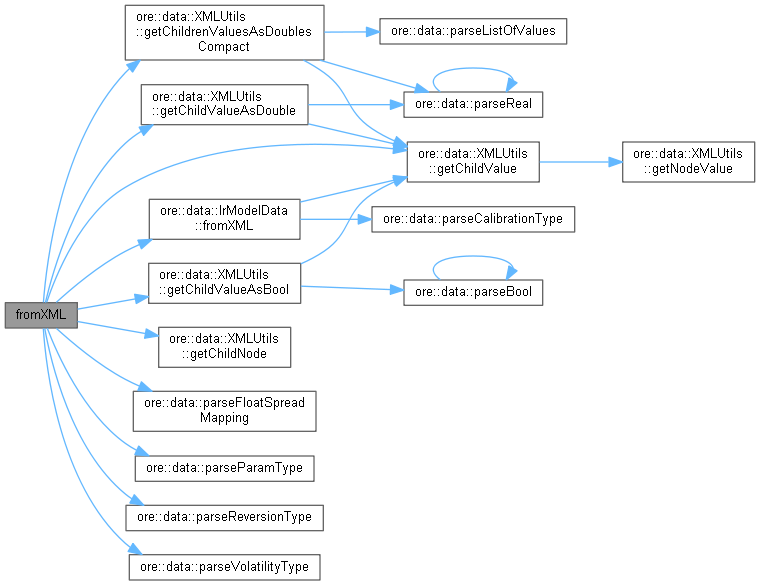

| virtual void | fromXML (XMLNode *node) override |

| virtual XMLNode * | toXML (XMLDocument &doc) const override |

Setters/Getters | |

| ReversionType & | reversionType () |

| VolatilityType & | volatilityType () |

| bool & | calibrateH () |

| ParamType & | hParamType () |

| std::vector< Time > & | hTimes () |

| std::vector< Real > & | hValues () |

| bool & | calibrateA () |

| ParamType & | aParamType () |

| std::vector< Time > & | aTimes () |

| std::vector< Real > & | aValues () |

| Real & | shiftHorizon () |

| Real & | scaling () |

| QuantExt::AnalyticLgmSwaptionEngine::FloatSpreadMapping & | floatSpreadMapping () |

| std::vector< std::string > & | optionExpiries () const |

| std::vector< std::string > & | optionTerms () const |

| std::vector< std::string > & | optionStrikes () const |

| ReversionParameter | reversionParameter () const |

| VolatilityParameter | volatilityParameter () const |

| Public Member Functions inherited from IrModelData | |

| IrModelData (const std::string &name) | |

| minimal constructor More... | |

| IrModelData (const std::string &name, const std::string &qualifier, CalibrationType calibrationType) | |

| Detailed constructor. More... | |

| virtual void | clear () |

| Clear list of calibration instruments. More... | |

| virtual void | reset () |

| Reset member variables to defaults. More... | |

| const std::string & | name () |

| std::string & | qualifier () |

| CalibrationType & | calibrationType () |

| virtual std::string | ccy () const |

| Public Member Functions inherited from XMLSerializable | |

| virtual | ~XMLSerializable () |

| virtual void | fromXML (XMLNode *node)=0 |

| virtual XMLNode * | toXML (XMLDocument &doc) const =0 |

| void | fromFile (const std::string &filename) |

| void | toFile (const std::string &filename) const |

| void | fromXMLString (const std::string &xml) |

| Parse from XML string. More... | |

| std::string | toXMLString () const |

| Parse from XML string. More... | |

Operators | |

| ReversionType | revType_ |

| VolatilityType | volType_ |

| bool | calibrateH_ |

| ParamType | hType_ |

| std::vector< Time > | hTimes_ |

| std::vector< Real > | hValues_ |

| bool | calibrateA_ |

| ParamType | aType_ |

| std::vector< Time > | aTimes_ |

| std::vector< Real > | aValues_ |

| Real | shiftHorizon_ |

| Real | scaling_ |

| std::vector< std::string > | optionExpiries_ |

| std::vector< std::string > | optionTerms_ |

| std::vector< std::string > | optionStrikes_ |

| QuantExt::AnalyticLgmSwaptionEngine::FloatSpreadMapping | floatSpreadMapping_ |

| bool | operator== (const LgmData &rhs) |

| bool | operator!= (const LgmData &rhs) |

Additional Inherited Members | |

| Protected Attributes inherited from IrModelData | |

| std::string | name_ |

| std::string | qualifier_ |

| CalibrationType | calibrationType_ |

Linear Gauss Markov Model Parameters.

This class contains the description of a Linear Gauss Markov interest rate model and instructions for how to calibrate it.

Definition at line 53 of file lgmdata.hpp.

|

strong |

Supported mean reversion types.

Definition at line 56 of file lgmdata.hpp.

|

strong |

Supported volatility types.

| Enumerator | |

|---|---|

| HullWhite | Parametrize volatility as HullWhite sigma(t) |

| Hagan | Parametrize volatility as Hagan alpha(t) |

Definition at line 67 of file lgmdata.hpp.

| LgmData | ( | ) |

Default constructor.

Definition at line 75 of file lgmdata.hpp.

| LgmData | ( | std::string | qualifier, |

| CalibrationType | calibrationType, | ||

| ReversionType | revType, | ||

| VolatilityType | volType, | ||

| bool | calibrateH, | ||

| ParamType | hType, | ||

| std::vector< Time > | hTimes, | ||

| std::vector< Real > | hValues, | ||

| bool | calibrateA, | ||

| ParamType | aType, | ||

| std::vector< Time > | aTimes, | ||

| std::vector< Real > | aValues, | ||

| Real | shiftHorizon = 0.0, |

||

| Real | scaling = 1.0, |

||

| std::vector< std::string > | optionExpiries = std::vector<std::string>(), |

||

| std::vector< std::string > | optionTerms = std::vector<std::string>(), |

||

| std::vector< std::string > | optionStrikes = std::vector<std::string>(), |

||

| const QuantExt::AnalyticLgmSwaptionEngine::FloatSpreadMapping | inputFloatSpreadMapping = QuantExt::AnalyticLgmSwaptionEngine::proRata |

||

| ) |

Detailed constructor.

Definition at line 81 of file lgmdata.hpp.

|

overridevirtual |

Clear list of calibration instruments.

Reimplemented from IrModelData.

Definition at line 123 of file lgmdata.cpp.

Here is the caller graph for this function:

|

overridevirtual |

Reset member variables to defaults.

Reimplemented from IrModelData.

Definition at line 129 of file lgmdata.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

overridevirtual |

Reimplemented from IrModelData.

Reimplemented in CrLgmData, and IrLgmData.

Definition at line 145 of file lgmdata.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

overridevirtual |

Reimplemented from IrModelData.

Reimplemented in CrLgmData, and IrLgmData.

Definition at line 207 of file lgmdata.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| ReversionType & reversionType | ( | ) |

Definition at line 108 of file lgmdata.hpp.

| VolatilityType & volatilityType | ( | ) |

Definition at line 109 of file lgmdata.hpp.

| bool & calibrateH | ( | ) |

Definition at line 110 of file lgmdata.hpp.

| ParamType & hParamType | ( | ) |

Definition at line 111 of file lgmdata.hpp.

| std::vector< Time > & hTimes | ( | ) |

Definition at line 112 of file lgmdata.hpp.

| std::vector< Real > & hValues | ( | ) |

Definition at line 113 of file lgmdata.hpp.

| bool & calibrateA | ( | ) |

Definition at line 114 of file lgmdata.hpp.

| ParamType & aParamType | ( | ) |

Definition at line 115 of file lgmdata.hpp.

| std::vector< Time > & aTimes | ( | ) |

Definition at line 116 of file lgmdata.hpp.

| std::vector< Real > & aValues | ( | ) |

Definition at line 117 of file lgmdata.hpp.

| Real & shiftHorizon | ( | ) |

Definition at line 118 of file lgmdata.hpp.

| Real & scaling | ( | ) |

Definition at line 119 of file lgmdata.hpp.

| QuantExt::AnalyticLgmSwaptionEngine::FloatSpreadMapping & floatSpreadMapping | ( | ) |

Definition at line 120 of file lgmdata.hpp.

| std::vector< std::string > & optionExpiries | ( | ) | const |

| std::vector< std::string > & optionTerms | ( | ) | const |

| std::vector< std::string > & optionStrikes | ( | ) | const |

| ReversionParameter reversionParameter | ( | ) | const |

Definition at line 243 of file lgmdata.cpp.

| VolatilityParameter volatilityParameter | ( | ) | const |

Definition at line 247 of file lgmdata.cpp.

Definition at line 47 of file lgmdata.cpp.

Definition at line 60 of file lgmdata.cpp.

|

private |

Definition at line 135 of file lgmdata.hpp.

|

private |

Definition at line 136 of file lgmdata.hpp.

|

private |

Definition at line 137 of file lgmdata.hpp.

|

private |

Definition at line 138 of file lgmdata.hpp.

|

private |

Definition at line 139 of file lgmdata.hpp.

|

private |

Definition at line 140 of file lgmdata.hpp.

|

private |

Definition at line 141 of file lgmdata.hpp.

|

private |

Definition at line 142 of file lgmdata.hpp.

|

private |

Definition at line 143 of file lgmdata.hpp.

|

private |

Definition at line 144 of file lgmdata.hpp.

|

private |

Definition at line 145 of file lgmdata.hpp.

|

private |

Definition at line 145 of file lgmdata.hpp.

|

mutableprivate |

Definition at line 146 of file lgmdata.hpp.

|

mutableprivate |

Definition at line 147 of file lgmdata.hpp.

|

mutableprivate |

Definition at line 148 of file lgmdata.hpp.

|

private |

Definition at line 149 of file lgmdata.hpp.