Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <ored/portfolio/creditdefaultswapdata.hpp>

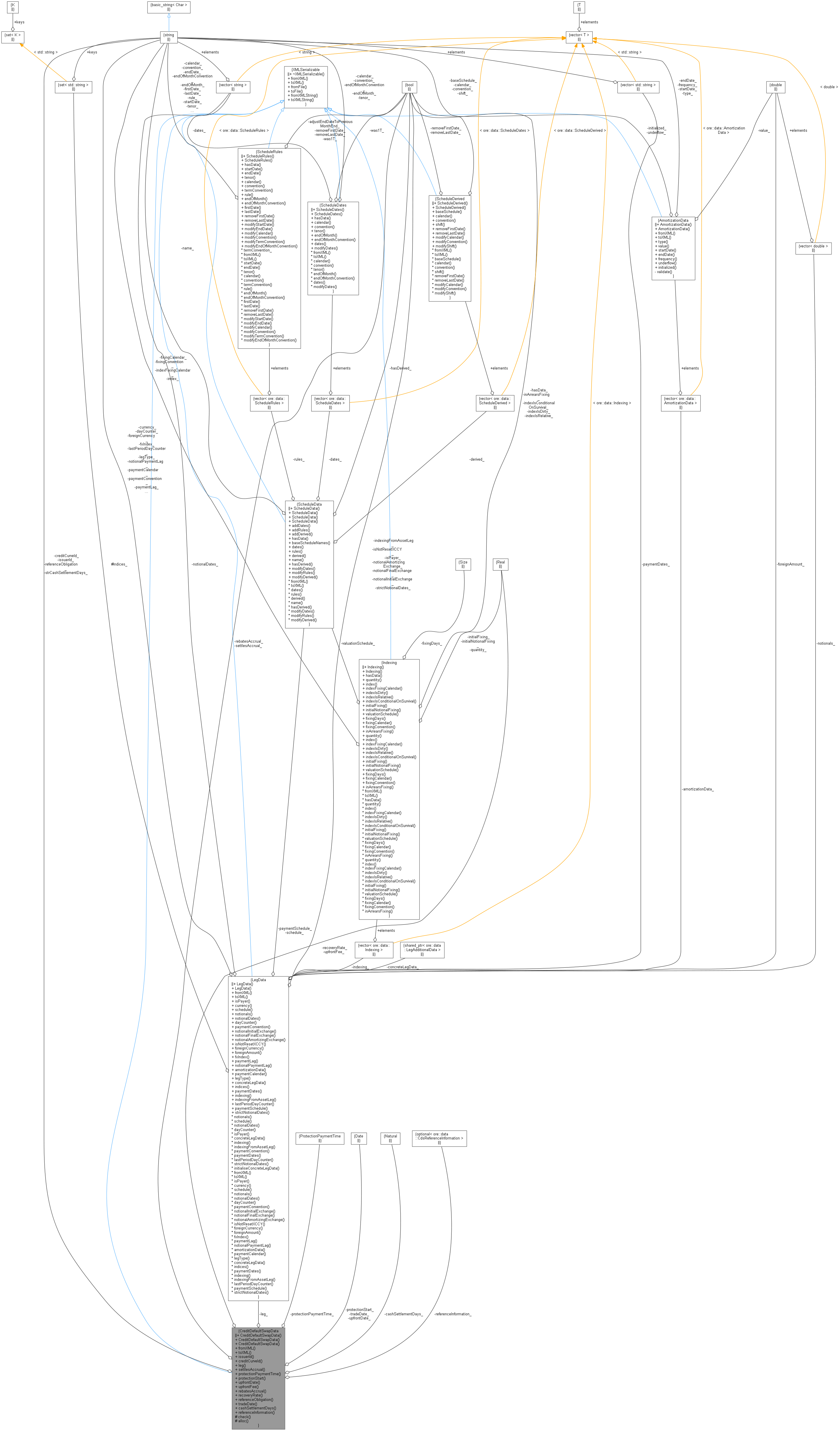

Inheritance diagram for CreditDefaultSwapData: Collaboration diagram for CreditDefaultSwapData:

Inheritance diagram for CreditDefaultSwapData: Collaboration diagram for CreditDefaultSwapData:Public Types | |

| using | PPT = QuantLib::CreditDefaultSwap::ProtectionPaymentTime |

Public Member Functions | |

| CreditDefaultSwapData () | |

| Default constructor. More... | |

| CreditDefaultSwapData (const string &issuerId, const string &creditCurveId, const LegData &leg, const bool settlesAccrual=true, const PPT protectionPaymentTime=PPT::atDefault, const Date &protectionStart=Date(), const Date &upfrontDate=Date(), const Real upfrontFee=Null< Real >(), QuantLib::Real recoveryRate=QuantLib::Null< QuantLib::Real >(), const std::string &referenceObligation="", const Date &tradeDate=Date(), const std::string &cashSettlementDays="", const bool rebatesAccrual=true) | |

Constructor that takes an explicit creditCurveId. More... | |

| CreditDefaultSwapData (const std::string &issuerId, const CdsReferenceInformation &referenceInformation, const LegData &leg, bool settlesAccrual=true, const PPT protectionPaymentTime=PPT::atDefault, const QuantLib::Date &protectionStart=QuantLib::Date(), const QuantLib::Date &upfrontDate=QuantLib::Date(), QuantLib::Real upfrontFee=QuantLib::Null< QuantLib::Real >(), QuantLib::Real recoveryRate=QuantLib::Null< QuantLib::Real >(), const std::string &referenceObligation="", const Date &tradeDate=Date(), const std::string &cashSettlementDays="", const bool rebatesAccrual=true) | |

Constructor that takes a referenceInformation object. More... | |

| void | fromXML (XMLNode *node) override |

| XMLNode * | toXML (XMLDocument &doc) const override |

| const string & | issuerId () const |

| const string & | creditCurveId () const |

| const LegData & | leg () const |

| bool | settlesAccrual () const |

| PPT | protectionPaymentTime () const |

| const Date & | protectionStart () const |

| const Date & | upfrontDate () const |

| Real | upfrontFee () const |

| bool | rebatesAccrual () const |

| QuantLib::Real | recoveryRate () const |

| const std::string & | referenceObligation () const |

| CDS Reference Obligation. More... | |

| const QuantLib::Date & | tradeDate () const |

| QuantLib::Natural | cashSettlementDays () const |

| const boost::optional< CdsReferenceInformation > & | referenceInformation () const |

| Public Member Functions inherited from XMLSerializable | |

| virtual | ~XMLSerializable () |

| virtual void | fromXML (XMLNode *node)=0 |

| virtual XMLNode * | toXML (XMLDocument &doc) const =0 |

| void | fromFile (const std::string &filename) |

| void | toFile (const std::string &filename) const |

| void | fromXMLString (const std::string &xml) |

| Parse from XML string. More... | |

| std::string | toXMLString () const |

| Parse from XML string. More... | |

Protected Member Functions | |

| virtual void | check (XMLNode *node) const |

| virtual XMLNode * | alloc (XMLDocument &doc) const |

Private Attributes | |

| std::string | issuerId_ |

| std::string | creditCurveId_ |

| LegData | leg_ |

| bool | settlesAccrual_ |

| PPT | protectionPaymentTime_ |

| QuantLib::Date | protectionStart_ |

| QuantLib::Date | upfrontDate_ |

| QuantLib::Real | upfrontFee_ |

| bool | rebatesAccrual_ |

| QuantLib::Real | recoveryRate_ |

Populated if the CDS is a fixed recovery rate CDS, otherwise Null<Real>() More... | |

| std::string | referenceObligation_ |

| QuantLib::Date | tradeDate_ |

| std::string | strCashSettlementDays_ |

| QuantLib::Natural | cashSettlementDays_ |

| boost::optional< CdsReferenceInformation > | referenceInformation_ |

Serializable credit default swap data

Definition at line 133 of file creditdefaultswapdata.hpp.

| using PPT = QuantLib::CreditDefaultSwap::ProtectionPaymentTime |

Definition at line 138 of file creditdefaultswapdata.hpp.

Default constructor.

Definition at line 486 of file creditdefaultswapdata.cpp.

| CreditDefaultSwapData | ( | const string & | issuerId, |

| const string & | creditCurveId, | ||

| const LegData & | leg, | ||

| const bool | settlesAccrual = true, |

||

| const PPT | protectionPaymentTime = PPT::atDefault, |

||

| const Date & | protectionStart = Date(), |

||

| const Date & | upfrontDate = Date(), |

||

| const Real | upfrontFee = Null< Real >(), |

||

| QuantLib::Real | recoveryRate = QuantLib::Null< QuantLib::Real >(), |

||

| const std::string & | referenceObligation = "", |

||

| const Date & | tradeDate = Date(), |

||

| const std::string & | cashSettlementDays = "", |

||

| const bool | rebatesAccrual = true |

||

| ) |

Constructor that takes an explicit creditCurveId.

| CreditDefaultSwapData | ( | const std::string & | issuerId, |

| const CdsReferenceInformation & | referenceInformation, | ||

| const LegData & | leg, | ||

| bool | settlesAccrual = true, |

||

| const PPT | protectionPaymentTime = PPT::atDefault, |

||

| const QuantLib::Date & | protectionStart = QuantLib::Date(), |

||

| const QuantLib::Date & | upfrontDate = QuantLib::Date(), |

||

| QuantLib::Real | upfrontFee = QuantLib::Null< QuantLib::Real >(), |

||

| QuantLib::Real | recoveryRate = QuantLib::Null< QuantLib::Real >(), |

||

| const std::string & | referenceObligation = "", |

||

| const Date & | tradeDate = Date(), |

||

| const std::string & | cashSettlementDays = "", |

||

| const bool | rebatesAccrual = true |

||

| ) |

Constructor that takes a referenceInformation object.

|

overridevirtual |

Implements XMLSerializable.

Reimplemented in IndexCreditDefaultSwapData.

Definition at line 515 of file creditdefaultswapdata.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

overridevirtual |

Implements XMLSerializable.

Reimplemented in IndexCreditDefaultSwapData.

Definition at line 599 of file creditdefaultswapdata.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| const string & issuerId | ( | ) | const |

Definition at line 168 of file creditdefaultswapdata.hpp.

Here is the caller graph for this function:| const string & creditCurveId | ( | ) | const |

Definition at line 652 of file creditdefaultswapdata.cpp.

Here is the caller graph for this function:| const LegData & leg | ( | ) | const |

Definition at line 170 of file creditdefaultswapdata.hpp.

Here is the caller graph for this function:| bool settlesAccrual | ( | ) | const |

Definition at line 171 of file creditdefaultswapdata.hpp.

Here is the caller graph for this function:| PPT protectionPaymentTime | ( | ) | const |

Definition at line 172 of file creditdefaultswapdata.hpp.

Here is the caller graph for this function:| const Date & protectionStart | ( | ) | const |

Definition at line 173 of file creditdefaultswapdata.hpp.

Here is the caller graph for this function:| const Date & upfrontDate | ( | ) | const |

Definition at line 174 of file creditdefaultswapdata.hpp.

Here is the caller graph for this function:| Real upfrontFee | ( | ) | const |

Definition at line 175 of file creditdefaultswapdata.hpp.

Here is the caller graph for this function:| bool rebatesAccrual | ( | ) | const |

Definition at line 176 of file creditdefaultswapdata.hpp.

Here is the caller graph for this function:| QuantLib::Real recoveryRate | ( | ) | const |

If the CDS is a fixed recovery CDS, this returns the recovery rate. For a standard CDS, it returns Null<Real>().

Definition at line 181 of file creditdefaultswapdata.hpp.

Here is the caller graph for this function:| const std::string & referenceObligation | ( | ) | const |

CDS Reference Obligation.

Definition at line 184 of file creditdefaultswapdata.hpp.

Here is the caller graph for this function:| const QuantLib::Date & tradeDate | ( | ) | const |

Definition at line 186 of file creditdefaultswapdata.hpp.

Here is the caller graph for this function:| QuantLib::Natural cashSettlementDays | ( | ) | const |

Definition at line 187 of file creditdefaultswapdata.hpp.

Here is the caller graph for this function:| const boost::optional< CdsReferenceInformation > & referenceInformation | ( | ) | const |

CDS reference information. This will be empty if an explicit credit curve ID has been used.

Definition at line 191 of file creditdefaultswapdata.hpp.

Here is the caller graph for this function:

|

protectedvirtual |

Reimplemented in IndexCreditDefaultSwapData.

Definition at line 660 of file creditdefaultswapdata.cpp.

Here is the call graph for this function:

|

protectedvirtual |

Reimplemented in IndexCreditDefaultSwapData.

Definition at line 664 of file creditdefaultswapdata.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

private |

Definition at line 198 of file creditdefaultswapdata.hpp.

|

private |

Definition at line 199 of file creditdefaultswapdata.hpp.

|

private |

Definition at line 200 of file creditdefaultswapdata.hpp.

|

private |

Definition at line 201 of file creditdefaultswapdata.hpp.

|

private |

Definition at line 202 of file creditdefaultswapdata.hpp.

|

private |

Definition at line 203 of file creditdefaultswapdata.hpp.

|

private |

Definition at line 204 of file creditdefaultswapdata.hpp.

|

private |

Definition at line 205 of file creditdefaultswapdata.hpp.

|

private |

Definition at line 206 of file creditdefaultswapdata.hpp.

|

private |

Populated if the CDS is a fixed recovery rate CDS, otherwise Null<Real>()

Definition at line 209 of file creditdefaultswapdata.hpp.

|

private |

Definition at line 211 of file creditdefaultswapdata.hpp.

|

private |

Definition at line 212 of file creditdefaultswapdata.hpp.

|

private |

Definition at line 213 of file creditdefaultswapdata.hpp.

|

private |

Definition at line 214 of file creditdefaultswapdata.hpp.

|

private |

Definition at line 216 of file creditdefaultswapdata.hpp.