Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <ored/portfolio/commoditylegdata.hpp>

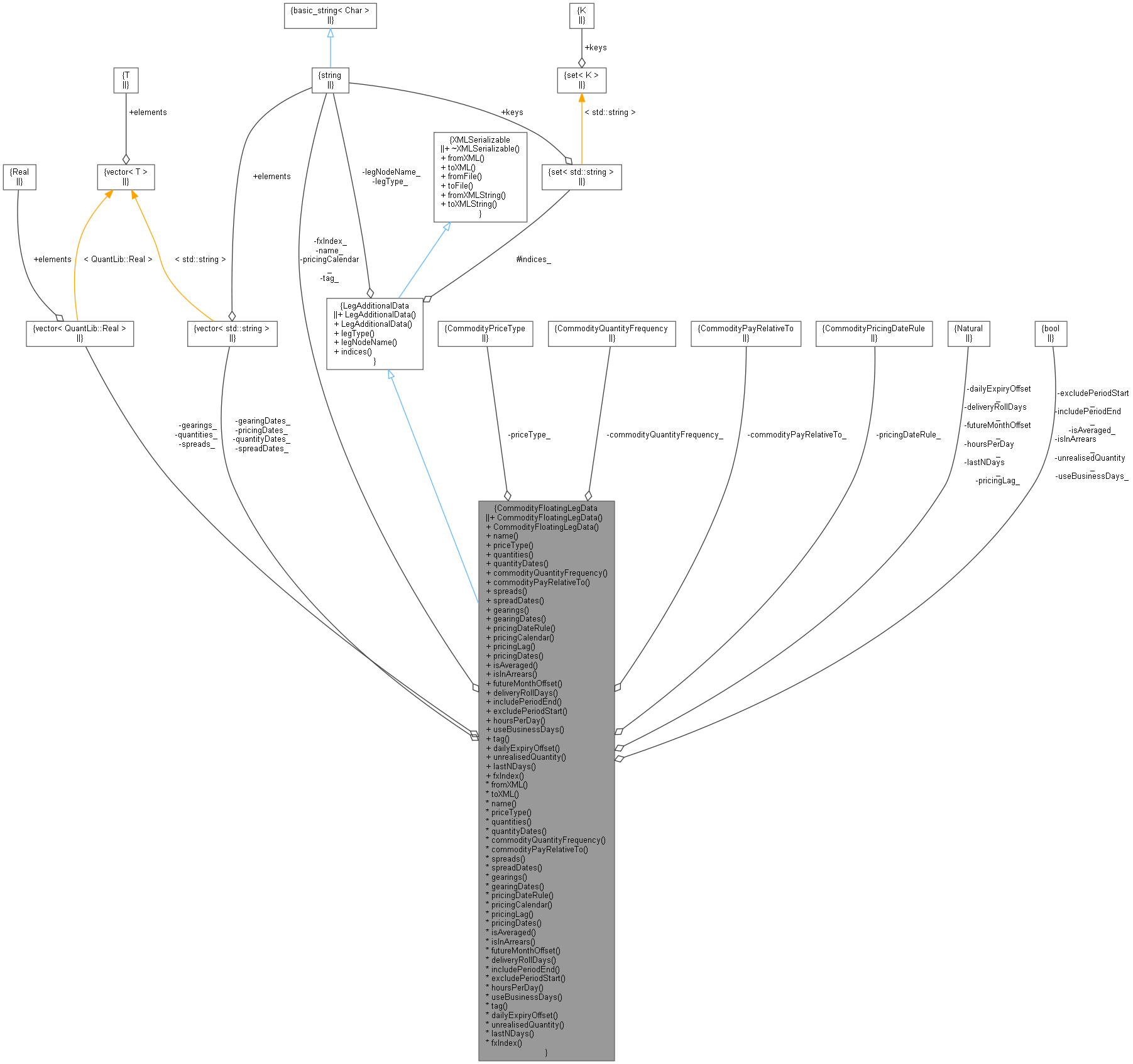

Inheritance diagram for CommodityFloatingLegData: Collaboration diagram for CommodityFloatingLegData:

Inheritance diagram for CommodityFloatingLegData: Collaboration diagram for CommodityFloatingLegData:Public Member Functions | |

| CommodityFloatingLegData () | |

| Default constructor. More... | |

| CommodityFloatingLegData (const std::string &name, CommodityPriceType priceType, const std::vector< QuantLib::Real > &quantities, const std::vector< std::string > &quantityDates, QuantExt::CommodityQuantityFrequency commodityQuantityFrequency=QuantExt::CommodityQuantityFrequency::PerCalculationPeriod, CommodityPayRelativeTo commodityPayRelativeTo=CommodityPayRelativeTo::CalculationPeriodEndDate, const std::vector< QuantLib::Real > &spreads={}, const std::vector< std::string > &spreadDates={}, const std::vector< QuantLib::Real > &gearings={}, const std::vector< std::string > &gearingDates={}, CommodityPricingDateRule pricingDateRule=CommodityPricingDateRule::FutureExpiryDate, const std::string &pricingCalendar="", QuantLib::Natural pricingLag=0, const std::vector< std::string > &pricingDates={}, bool isAveraged=false, bool isInArrears=true, QuantLib::Natural futureMonthOffset=0, QuantLib::Natural deliveryRollDays=0, bool includePeriodEnd=true, bool excludePeriodStart=true, QuantLib::Natural hoursPerDay=QuantLib::Null< QuantLib::Natural >(), bool useBusinessDays=true, const std::string &tag="", QuantLib::Natural dailyExpiryOffset=QuantLib::Null< QuantLib::Natural >(), bool unrealisedQuantity=false, QuantLib::Natural lastNDays=QuantLib::Null< QuantLib::Natural >(), std::string fxIndex="") | |

| Constructor. More... | |

Inspectors | |

| const std::string & | name () const |

| CommodityPriceType | priceType () const |

| const std::vector< QuantLib::Real > & | quantities () const |

| const std::vector< std::string > & | quantityDates () const |

| QuantExt::CommodityQuantityFrequency | commodityQuantityFrequency () const |

| CommodityPayRelativeTo | commodityPayRelativeTo () const |

| const std::vector< QuantLib::Real > & | spreads () const |

| const std::vector< std::string > & | spreadDates () const |

| const std::vector< QuantLib::Real > & | gearings () const |

| const std::vector< std::string > & | gearingDates () const |

| CommodityPricingDateRule | pricingDateRule () const |

| const std::string & | pricingCalendar () const |

| QuantLib::Natural | pricingLag () const |

| const std::vector< std::string > & | pricingDates () const |

| bool | isAveraged () const |

| bool | isInArrears () const |

| QuantLib::Natural | futureMonthOffset () const |

| QuantLib::Natural | deliveryRollDays () const |

| bool | includePeriodEnd () const |

| bool | excludePeriodStart () const |

| QuantLib::Natural | hoursPerDay () const |

| bool | useBusinessDays () const |

| const std::string & | tag () const |

| QuantLib::Natural | dailyExpiryOffset () const |

| bool | unrealisedQuantity () const |

| QuantLib::Natural | lastNDays () const |

| std::string const & | fxIndex () const |

| Public Member Functions inherited from LegAdditionalData | |

| LegAdditionalData (const string &legType, const string &legNodeName) | |

| LegAdditionalData (const string &legType) | |

| const string & | legType () const |

| const string & | legNodeName () const |

| const std::set< std::string > & | indices () const |

| Public Member Functions inherited from XMLSerializable | |

| virtual | ~XMLSerializable () |

| virtual void | fromXML (XMLNode *node)=0 |

| virtual XMLNode * | toXML (XMLDocument &doc) const =0 |

| void | fromFile (const std::string &filename) |

| void | toFile (const std::string &filename) const |

| void | fromXMLString (const std::string &xml) |

| Parse from XML string. More... | |

| std::string | toXMLString () const |

| Parse from XML string. More... | |

Additional Inherited Members | |

| Protected Attributes inherited from LegAdditionalData | |

| std::set< std::string > | indices_ |

Definition at line 96 of file commoditylegdata.hpp.

Default constructor.

Definition at line 171 of file commoditylegdata.cpp.

| CommodityFloatingLegData | ( | const std::string & | name, |

| CommodityPriceType | priceType, | ||

| const std::vector< QuantLib::Real > & | quantities, | ||

| const std::vector< std::string > & | quantityDates, | ||

| QuantExt::CommodityQuantityFrequency | commodityQuantityFrequency = QuantExt::CommodityQuantityFrequency::PerCalculationPeriod, |

||

| CommodityPayRelativeTo | commodityPayRelativeTo = CommodityPayRelativeTo::CalculationPeriodEndDate, |

||

| const std::vector< QuantLib::Real > & | spreads = {}, |

||

| const std::vector< std::string > & | spreadDates = {}, |

||

| const std::vector< QuantLib::Real > & | gearings = {}, |

||

| const std::vector< std::string > & | gearingDates = {}, |

||

| CommodityPricingDateRule | pricingDateRule = CommodityPricingDateRule::FutureExpiryDate, |

||

| const std::string & | pricingCalendar = "", |

||

| QuantLib::Natural | pricingLag = 0, |

||

| const std::vector< std::string > & | pricingDates = {}, |

||

| bool | isAveraged = false, |

||

| bool | isInArrears = true, |

||

| QuantLib::Natural | futureMonthOffset = 0, |

||

| QuantLib::Natural | deliveryRollDays = 0, |

||

| bool | includePeriodEnd = true, |

||

| bool | excludePeriodStart = true, |

||

| QuantLib::Natural | hoursPerDay = QuantLib::Null< QuantLib::Natural >(), |

||

| bool | useBusinessDays = true, |

||

| const std::string & | tag = "", |

||

| QuantLib::Natural | dailyExpiryOffset = QuantLib::Null< QuantLib::Natural >(), |

||

| bool | unrealisedQuantity = false, |

||

| QuantLib::Natural | lastNDays = QuantLib::Null< QuantLib::Natural >(), |

||

| std::string | fxIndex = "" |

||

| ) |

Constructor.

| const std::string & name | ( | ) | const |

Definition at line 122 of file commoditylegdata.hpp.

| CommodityPriceType priceType | ( | ) | const |

Definition at line 123 of file commoditylegdata.hpp.

| const std::vector< QuantLib::Real > & quantities | ( | ) | const |

Definition at line 124 of file commoditylegdata.hpp.

| const std::vector< std::string > & quantityDates | ( | ) | const |

Definition at line 125 of file commoditylegdata.hpp.

| QuantExt::CommodityQuantityFrequency commodityQuantityFrequency | ( | ) | const |

Definition at line 126 of file commoditylegdata.hpp.

| CommodityPayRelativeTo commodityPayRelativeTo | ( | ) | const |

Definition at line 127 of file commoditylegdata.hpp.

| const std::vector< QuantLib::Real > & spreads | ( | ) | const |

Definition at line 128 of file commoditylegdata.hpp.

| const std::vector< std::string > & spreadDates | ( | ) | const |

Definition at line 129 of file commoditylegdata.hpp.

| const std::vector< QuantLib::Real > & gearings | ( | ) | const |

Definition at line 130 of file commoditylegdata.hpp.

| const std::vector< std::string > & gearingDates | ( | ) | const |

Definition at line 131 of file commoditylegdata.hpp.

| CommodityPricingDateRule pricingDateRule | ( | ) | const |

Definition at line 132 of file commoditylegdata.hpp.

| const std::string & pricingCalendar | ( | ) | const |

Definition at line 133 of file commoditylegdata.hpp.

| QuantLib::Natural pricingLag | ( | ) | const |

Definition at line 134 of file commoditylegdata.hpp.

| const std::vector< std::string > & pricingDates | ( | ) | const |

Definition at line 135 of file commoditylegdata.hpp.

| bool isAveraged | ( | ) | const |

Definition at line 136 of file commoditylegdata.hpp.

| bool isInArrears | ( | ) | const |

Definition at line 137 of file commoditylegdata.hpp.

| QuantLib::Natural futureMonthOffset | ( | ) | const |

Definition at line 138 of file commoditylegdata.hpp.

| QuantLib::Natural deliveryRollDays | ( | ) | const |

Definition at line 139 of file commoditylegdata.hpp.

| bool includePeriodEnd | ( | ) | const |

Definition at line 140 of file commoditylegdata.hpp.

| bool excludePeriodStart | ( | ) | const |

Definition at line 141 of file commoditylegdata.hpp.

| QuantLib::Natural hoursPerDay | ( | ) | const |

Definition at line 142 of file commoditylegdata.hpp.

| bool useBusinessDays | ( | ) | const |

Definition at line 143 of file commoditylegdata.hpp.

| const std::string & tag | ( | ) | const |

Definition at line 144 of file commoditylegdata.hpp.

| QuantLib::Natural dailyExpiryOffset | ( | ) | const |

Definition at line 145 of file commoditylegdata.hpp.

| bool unrealisedQuantity | ( | ) | const |

Definition at line 146 of file commoditylegdata.hpp.

| QuantLib::Natural lastNDays | ( | ) | const |

Definition at line 147 of file commoditylegdata.hpp.

| std::string const & fxIndex | ( | ) | const |

Definition at line 148 of file commoditylegdata.hpp.

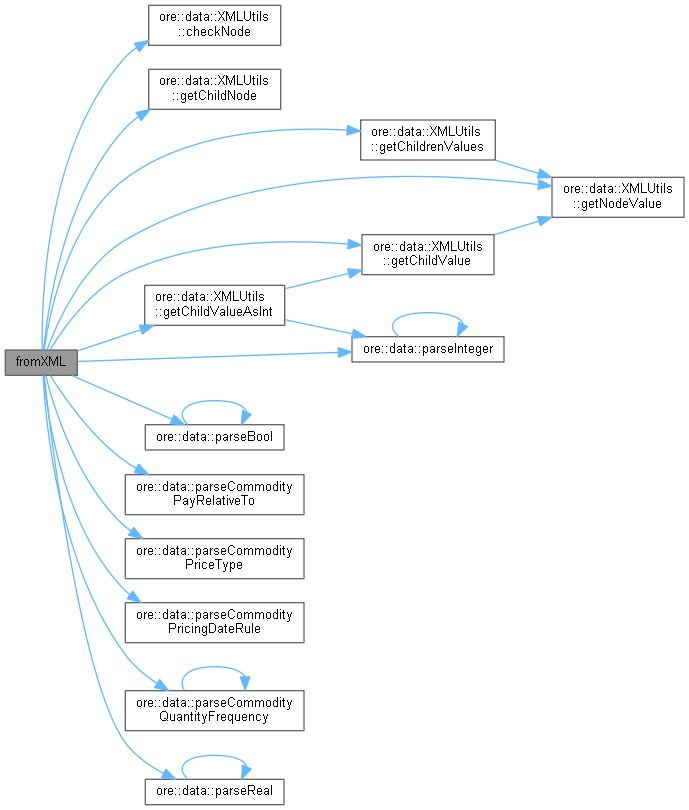

|

overridevirtual |

Implements XMLSerializable.

Definition at line 203 of file commoditylegdata.cpp.

Here is the call graph for this function:

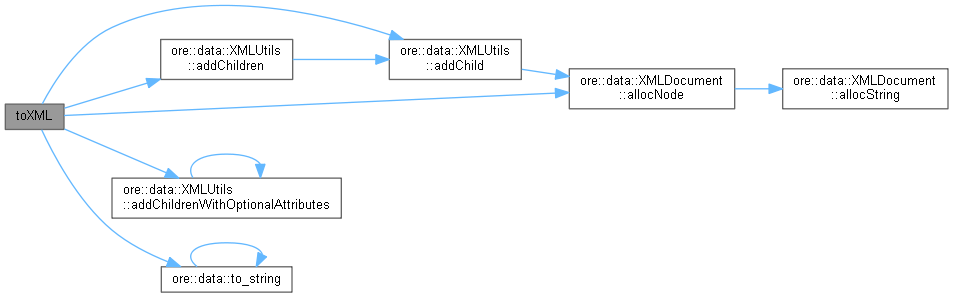

|

overridevirtual |

Implements XMLSerializable.

Definition at line 292 of file commoditylegdata.cpp.

Here is the call graph for this function:

|

private |

Definition at line 158 of file commoditylegdata.hpp.

|

private |

Definition at line 159 of file commoditylegdata.hpp.

|

private |

Definition at line 160 of file commoditylegdata.hpp.

|

private |

Definition at line 161 of file commoditylegdata.hpp.

|

private |

Definition at line 162 of file commoditylegdata.hpp.

|

private |

Definition at line 163 of file commoditylegdata.hpp.

|

private |

Definition at line 164 of file commoditylegdata.hpp.

|

private |

Definition at line 165 of file commoditylegdata.hpp.

|

private |

Definition at line 166 of file commoditylegdata.hpp.

|

private |

Definition at line 167 of file commoditylegdata.hpp.

|

private |

Definition at line 168 of file commoditylegdata.hpp.

|

private |

Definition at line 169 of file commoditylegdata.hpp.

|

private |

Definition at line 170 of file commoditylegdata.hpp.

|

private |

Definition at line 171 of file commoditylegdata.hpp.

|

private |

Definition at line 172 of file commoditylegdata.hpp.

|

private |

Definition at line 173 of file commoditylegdata.hpp.

|

private |

Definition at line 174 of file commoditylegdata.hpp.

|

private |

Definition at line 175 of file commoditylegdata.hpp.

|

private |

Definition at line 176 of file commoditylegdata.hpp.

|

private |

Definition at line 177 of file commoditylegdata.hpp.

|

private |

Definition at line 178 of file commoditylegdata.hpp.

|

private |

Definition at line 179 of file commoditylegdata.hpp.

|

private |

Definition at line 180 of file commoditylegdata.hpp.

|

private |

Definition at line 181 of file commoditylegdata.hpp.

|

private |

Definition at line 182 of file commoditylegdata.hpp.

|

private |

Definition at line 183 of file commoditylegdata.hpp.

|

private |

Definition at line 184 of file commoditylegdata.hpp.