Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <ored/portfolio/bond.hpp>

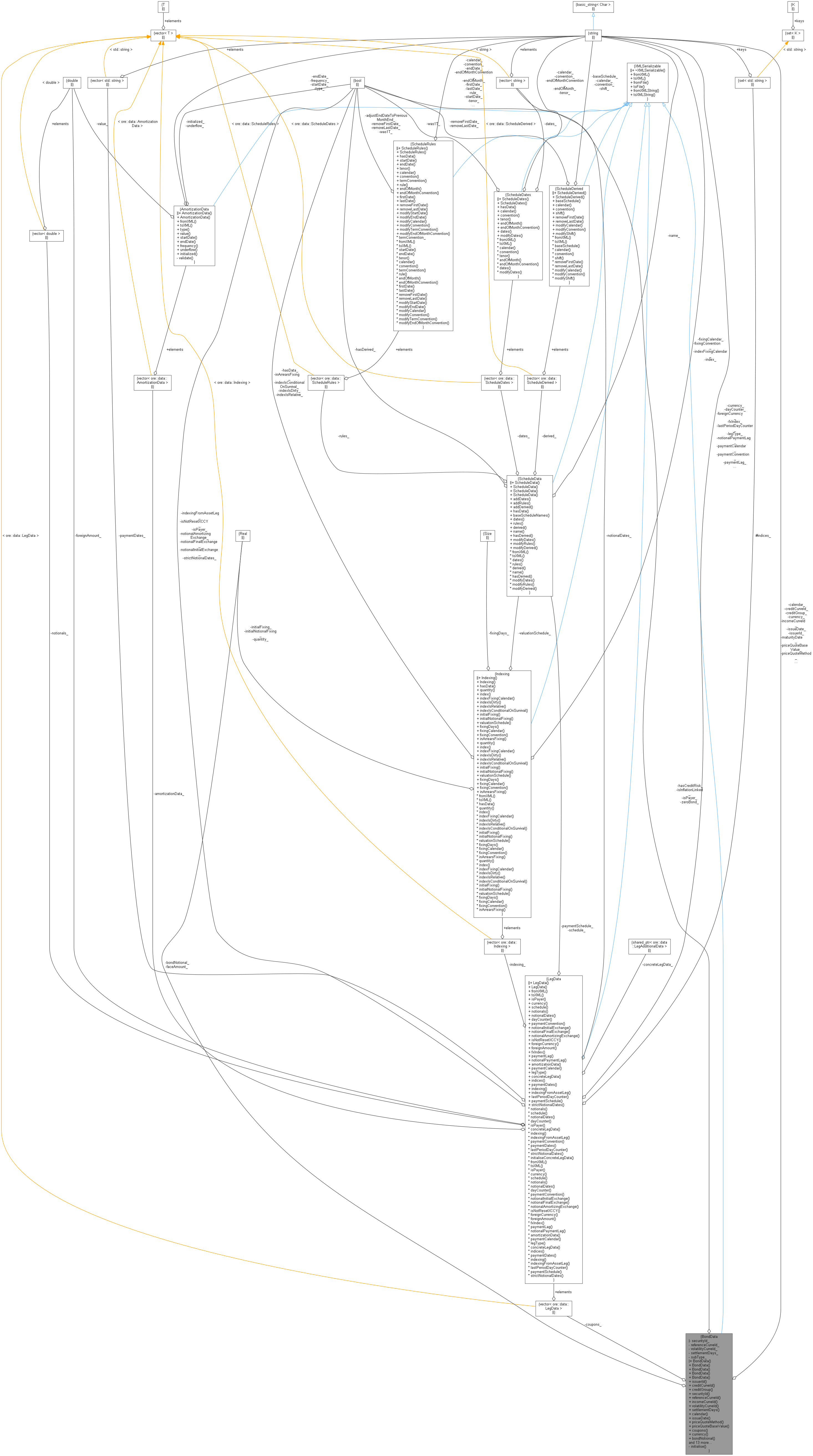

Inheritance diagram for BondData: Collaboration diagram for BondData:

Inheritance diagram for BondData: Collaboration diagram for BondData:Public Member Functions | |

| BondData () | |

| Default Contructor. More... | |

| BondData (string securityId, Real bondNotional, bool hasCreditRisk=true) | |

| Constructor to set up a bond from reference data. More... | |

| BondData (string issuerId, string creditCurveId, string securityId, string referenceCurveId, string settlementDays, string calendar, string issueDate, LegData &coupons, bool hasCreditRisk=true) | |

| Constructor for coupon bonds. More... | |

| BondData (string issuerId, string creditCurveId, string securityId, string referenceCurveId, string settlementDays, string calendar, string issueDate, const std::vector< LegData > &coupons, bool hasCreditRisk=true) | |

| Constructor for coupon bonds with multiple phases (represented as legs) More... | |

| BondData (string issuerId, string creditCurveId, string securityId, string referenceCurveId, string settlementDays, string calendar, Real faceAmount, string maturityDate, string currency, string issueDate, bool hasCreditRisk=true) | |

| Constructor for zero bonds, FIXME these can only be set up via this ctor, not via fromXML() More... | |

| const string & | issuerId () const |

| Inspectors. More... | |

| const string & | creditCurveId () const |

| const string & | creditGroup () const |

| const string & | securityId () const |

| const string & | referenceCurveId () const |

| const string & | incomeCurveId () const |

| const string & | volatilityCurveId () const |

| const string & | settlementDays () const |

| const string & | calendar () const |

| const string & | issueDate () const |

| QuantExt::BondIndex::PriceQuoteMethod | priceQuoteMethod () const |

| Real | priceQuoteBaseValue () const |

| const std::vector< LegData > & | coupons () const |

| const string & | currency () const |

| Real | bondNotional () const |

| bool | hasCreditRisk () const |

| bool | isPayer () const |

| bool | zeroBond () const |

| bool | isInflationLinked () const |

| Real | faceAmount () const |

| const string & | maturityDate () const |

| const string & | subType () const |

| virtual void | fromXML (XMLNode *node) override |

| XMLSerializable interface. More... | |

| virtual XMLNode * | toXML (XMLDocument &doc) const override |

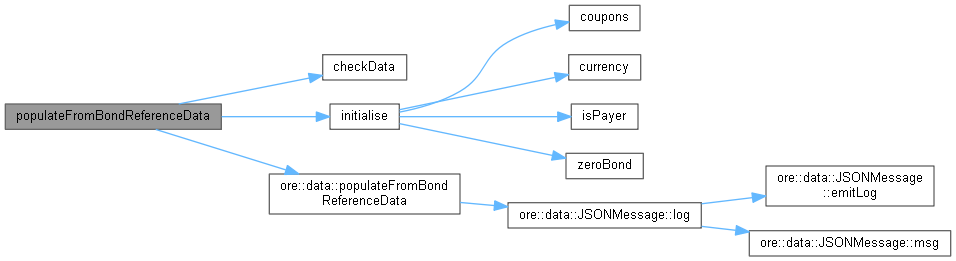

| void | populateFromBondReferenceData (const QuantLib::ext::shared_ptr< BondReferenceDatum > &referenceDatum, const std::string &startDate="", const std::string &endDate="") |

| populate data from reference datum and check data for completeness More... | |

| void | populateFromBondReferenceData (const QuantLib::ext::shared_ptr< ReferenceDataManager > &referenceData, const std::string &startDate="", const std::string &endDate="") |

| look up reference datum in ref data manager and populate, check data for completeness More... | |

| void | checkData () const |

| check data for completeness More... | |

| std::string | isdaBaseProduct () const |

| return isda sub type "Single Name", "Index" or throw if sub type can not be mapped More... | |

| Public Member Functions inherited from XMLSerializable | |

| virtual | ~XMLSerializable () |

| virtual void | fromXML (XMLNode *node)=0 |

| virtual XMLNode * | toXML (XMLDocument &doc) const =0 |

| void | fromFile (const std::string &filename) |

| void | toFile (const std::string &filename) const |

| void | fromXMLString (const std::string &xml) |

| Parse from XML string. More... | |

| std::string | toXMLString () const |

| Parse from XML string. More... | |

Private Member Functions | |

| void | initialise () |

Private Attributes | |

| string | issuerId_ |

| string | creditCurveId_ |

| string | creditGroup_ |

| string | securityId_ |

| string | referenceCurveId_ |

| string | incomeCurveId_ |

| string | volatilityCurveId_ |

| string | settlementDays_ |

| string | calendar_ |

| string | issueDate_ |

| string | priceQuoteMethod_ |

| string | priceQuoteBaseValue_ |

| std::vector< LegData > | coupons_ |

| bool | hasCreditRisk_ |

| Real | faceAmount_ |

| string | maturityDate_ |

| string | currency_ |

| bool | zeroBond_ |

| Real | bondNotional_ |

| bool | isPayer_ |

| bool | isInflationLinked_ |

| string | subType_ |

Serializable BondData FIXME zero bonds are only supported via the third constructor, but not in fromXML()

| BondData | ( | ) |

Default Contructor.

Definition at line 41 of file bond.hpp.

| BondData | ( | string | issuerId, |

| string | creditCurveId, | ||

| string | securityId, | ||

| string | referenceCurveId, | ||

| string | settlementDays, | ||

| string | calendar, | ||

| string | issueDate, | ||

| LegData & | coupons, | ||

| bool | hasCreditRisk = true |

||

| ) |

Constructor for coupon bonds.

Definition at line 50 of file bond.hpp.

Here is the call graph for this function:| BondData | ( | string | issuerId, |

| string | creditCurveId, | ||

| string | securityId, | ||

| string | referenceCurveId, | ||

| string | settlementDays, | ||

| string | calendar, | ||

| string | issueDate, | ||

| const std::vector< LegData > & | coupons, | ||

| bool | hasCreditRisk = true |

||

| ) |

Constructor for coupon bonds with multiple phases (represented as legs)

Definition at line 60 of file bond.hpp.

Here is the call graph for this function:| BondData | ( | string | issuerId, |

| string | creditCurveId, | ||

| string | securityId, | ||

| string | referenceCurveId, | ||

| string | settlementDays, | ||

| string | calendar, | ||

| Real | faceAmount, | ||

| string | maturityDate, | ||

| string | currency, | ||

| string | issueDate, | ||

| bool | hasCreditRisk = true |

||

| ) |

Constructor for zero bonds, FIXME these can only be set up via this ctor, not via fromXML()

Definition at line 70 of file bond.hpp.

Here is the call graph for this function:| const string & issuerId | ( | ) | const |

| const string & creditCurveId | ( | ) | const |

| const string & securityId | ( | ) | const |

| const string & referenceCurveId | ( | ) | const |

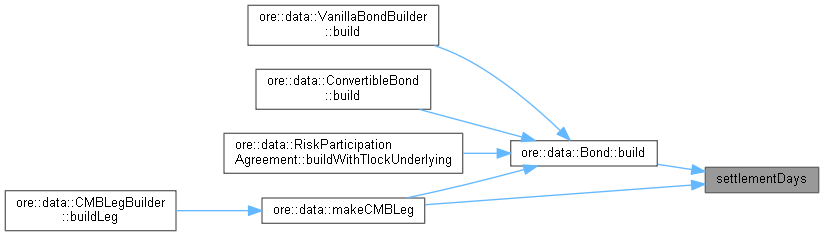

| const string & settlementDays | ( | ) | const |

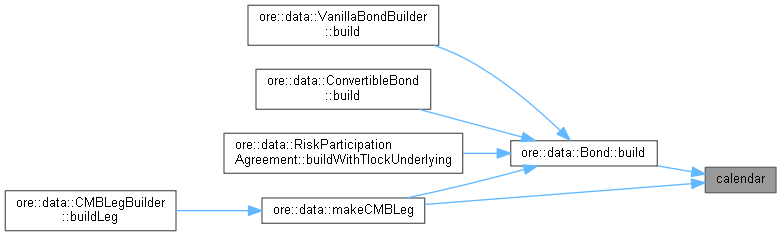

| const string & calendar | ( | ) | const |

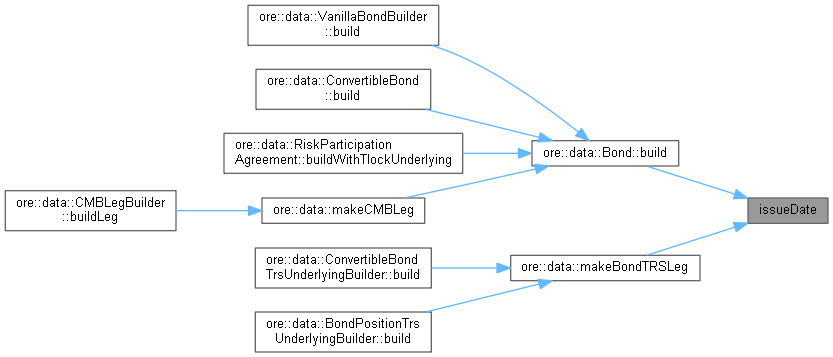

| const string & issueDate | ( | ) | const |

| QuantExt::BondIndex::PriceQuoteMethod priceQuoteMethod | ( | ) | const |

Definition at line 45 of file bond.cpp.

Here is the call graph for this function:| Real priceQuoteBaseValue | ( | ) | const |

Definition at line 50 of file bond.cpp.

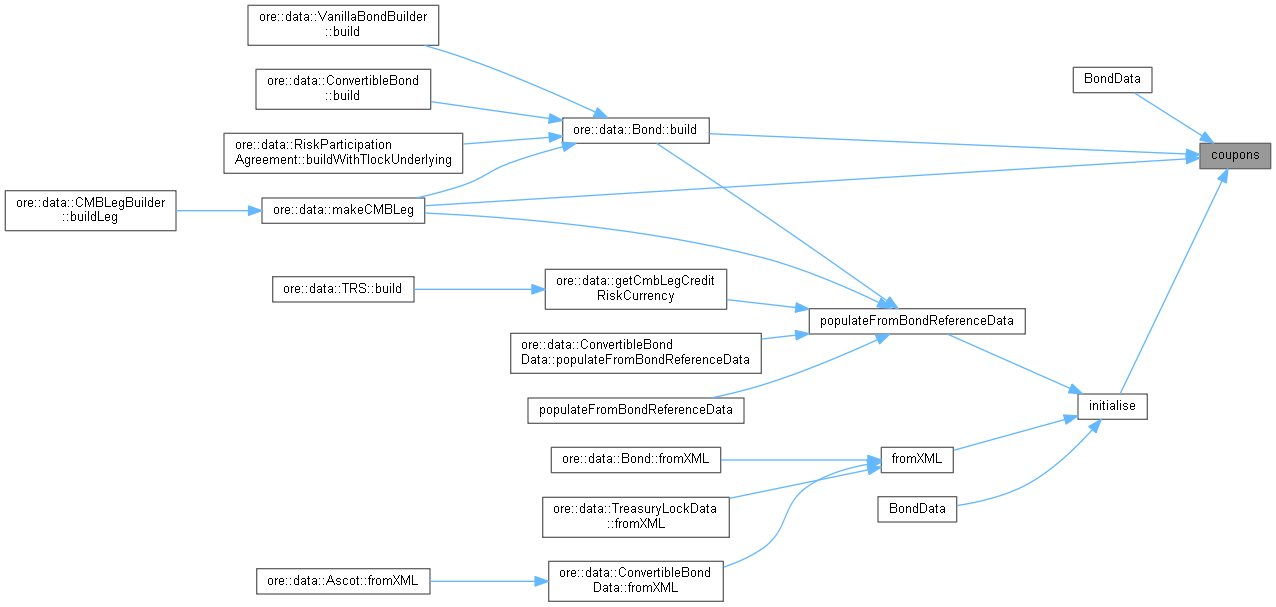

Here is the call graph for this function:| const std::vector< LegData > & coupons | ( | ) | const |

| const string & currency | ( | ) | const |

| Real bondNotional | ( | ) | const |

| bool hasCreditRisk | ( | ) | const |

| bool isPayer | ( | ) | const |

| bool zeroBond | ( | ) | const |

| Real faceAmount | ( | ) | const |

| const string & maturityDate | ( | ) | const |

| const string & subType | ( | ) | const |

|

overridevirtual |

XMLSerializable interface.

Implements XMLSerializable.

Definition at line 59 of file bond.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

overridevirtual |

Implements XMLSerializable.

Definition at line 95 of file bond.cpp.

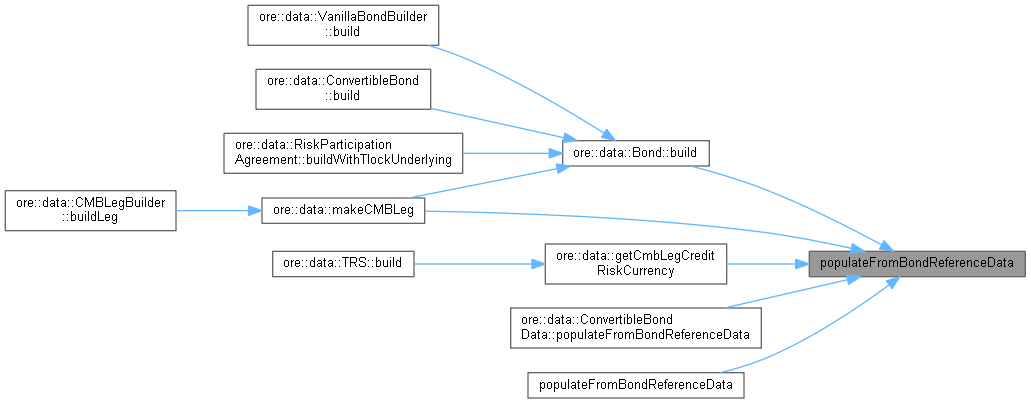

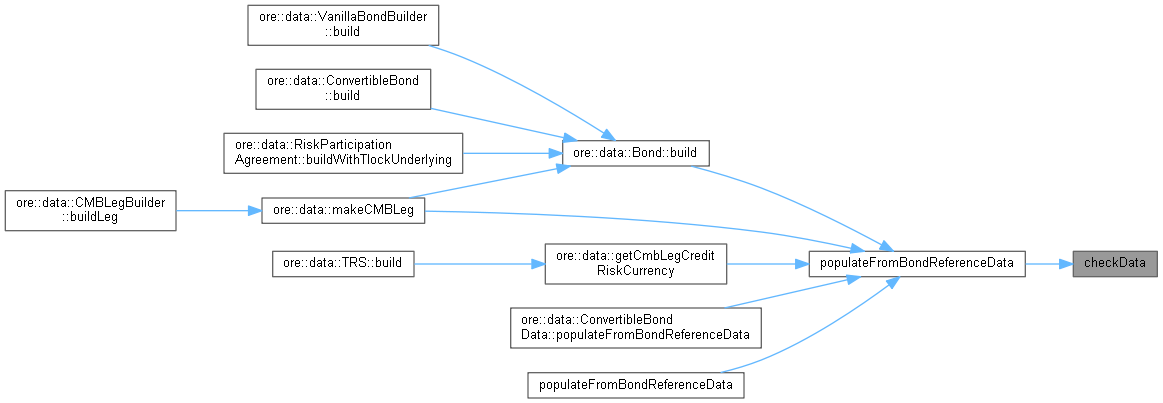

Here is the call graph for this function: Here is the caller graph for this function:| void populateFromBondReferenceData | ( | const QuantLib::ext::shared_ptr< BondReferenceDatum > & | referenceDatum, |

| const std::string & | startDate = "", |

||

| const std::string & | endDate = "" |

||

| ) |

populate data from reference datum and check data for completeness

Definition at line 175 of file bond.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void populateFromBondReferenceData | ( | const QuantLib::ext::shared_ptr< ReferenceDataManager > & | referenceData, |

| const std::string & | startDate = "", |

||

| const std::string & | endDate = "" |

||

| ) |

look up reference datum in ref data manager and populate, check data for completeness

Definition at line 186 of file bond.cpp.

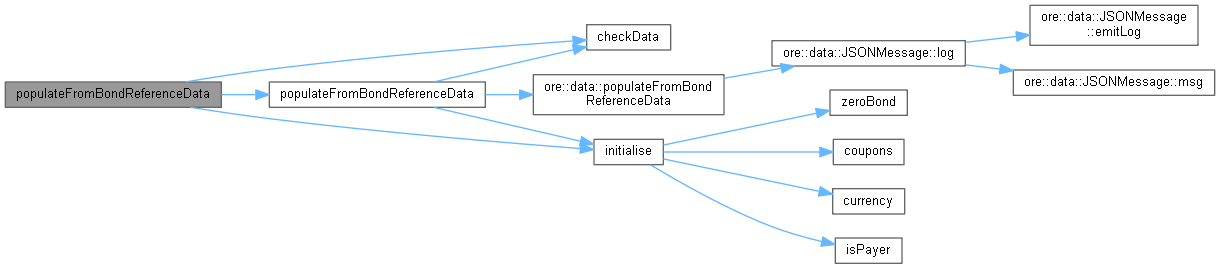

Here is the call graph for this function:| void checkData | ( | ) | const |

check data for completeness

Definition at line 201 of file bond.cpp.

Here is the caller graph for this function:| std::string isdaBaseProduct | ( | ) | const |

return isda sub type "Single Name", "Index" or throw if sub type can not be mapped

Definition at line 213 of file bond.cpp.

Here is the call graph for this function:

|

private |

Definition at line 130 of file bond.cpp.

Here is the call graph for this function: Here is the caller graph for this function: