Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

An Adjusted In Memory Loader,. More...

#include <ored/marketdata/adjustedinmemoryloader.hpp>

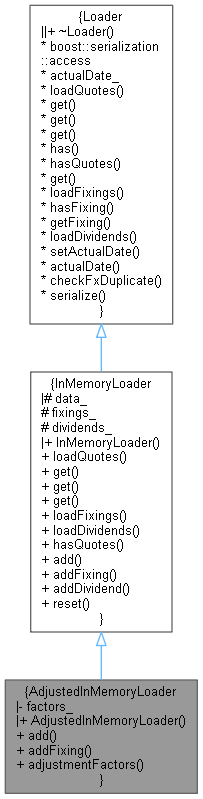

Inheritance diagram for AdjustedInMemoryLoader: Collaboration diagram for AdjustedInMemoryLoader:

Inheritance diagram for AdjustedInMemoryLoader: Collaboration diagram for AdjustedInMemoryLoader:Public Member Functions | |

| AdjustedInMemoryLoader (const ore::data::AdjustmentFactors &factors) | |

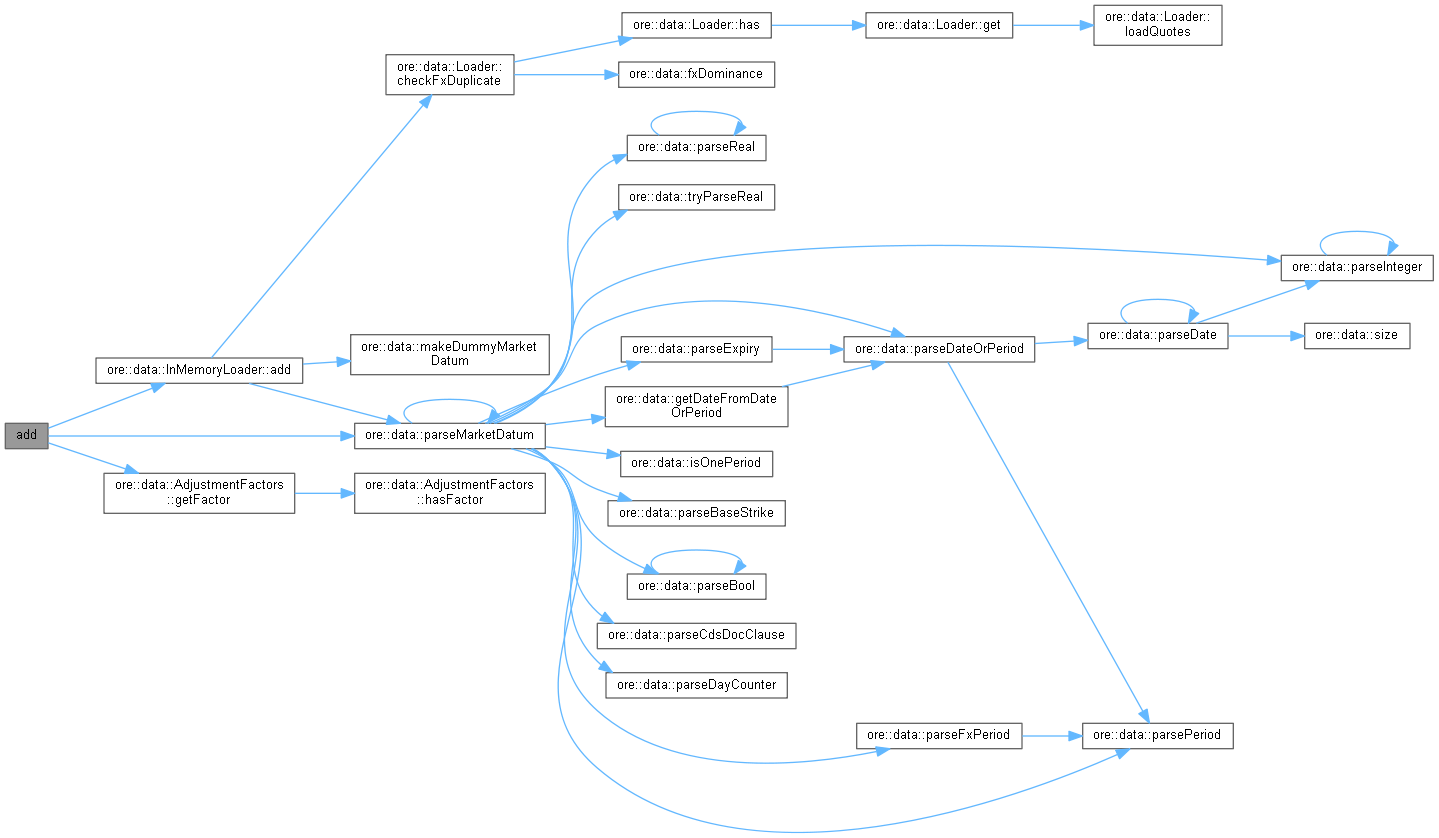

| virtual void | add (QuantLib::Date date, const std::string &name, QuantLib::Real value) override |

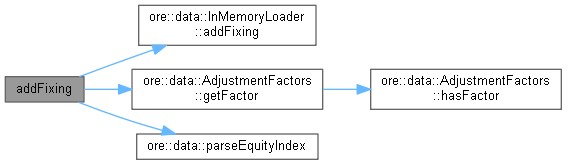

| virtual void | addFixing (QuantLib::Date date, const std::string &name, QuantLib::Real value) override |

| ore::data::AdjustmentFactors | adjustmentFactors () const |

| Public Member Functions inherited from InMemoryLoader | |

| InMemoryLoader () | |

| std::vector< QuantLib::ext::shared_ptr< MarketDatum > > | loadQuotes (const QuantLib::Date &d) const override |

| get all quotes, TODO change the return value to std::set More... | |

| QuantLib::ext::shared_ptr< MarketDatum > | get (const string &name, const QuantLib::Date &d) const override |

| get quote by its unique name, throws if not existent, override in derived classes for performance More... | |

| std::set< QuantLib::ext::shared_ptr< MarketDatum > > | get (const std::set< std::string > &names, const QuantLib::Date &asof) const override |

| get quotes matching a set of names, this should be overridden in derived classes for performance More... | |

| std::set< QuantLib::ext::shared_ptr< MarketDatum > > | get (const Wildcard &wildcard, const QuantLib::Date &asof) const override |

| get quotes matching a wildcard, this should be overriden in derived classes for performance More... | |

| std::set< Fixing > | loadFixings () const override |

| std::set< QuantExt::Dividend > | loadDividends () const override |

| Optional load dividends method. More... | |

| bool | hasQuotes (const QuantLib::Date &d) const override |

| check if there are quotes for a date More... | |

| virtual void | add (QuantLib::Date date, const string &name, QuantLib::Real value) |

| virtual void | addFixing (QuantLib::Date date, const string &name, QuantLib::Real value) |

| virtual void | addDividend (const QuantExt::Dividend ÷nd) |

| void | reset () |

| Public Member Functions inherited from Loader | |

| virtual | ~Loader () |

| virtual bool | has (const std::string &name, const QuantLib::Date &d) const |

| Default implementation, returns false if get throws or returns a null pointer. More... | |

| virtual QuantLib::ext::shared_ptr< MarketDatum > | get (const std::pair< std::string, bool > &name, const QuantLib::Date &d) const |

| virtual bool | hasFixing (const string &name, const QuantLib::Date &d) const |

| virtual Fixing | getFixing (const string &name, const QuantLib::Date &d) const |

| Default implementation for getFixing. More... | |

| void | setActualDate (const QuantLib::Date &d) |

| const Date & | actualDate () const |

| std::pair< bool, string > | checkFxDuplicate (const ext::shared_ptr< MarketDatum >, const QuantLib::Date &) |

Private Attributes | |

| ore::data::AdjustmentFactors | factors_ |

Additional Inherited Members | |

| Protected Attributes inherited from InMemoryLoader | |

| std::map< QuantLib::Date, std::set< QuantLib::ext::shared_ptr< MarketDatum >, SharedPtrMarketDatumComparator > > | data_ |

| std::set< Fixing > | fixings_ |

| std::set< QuantExt::Dividend > | dividends_ |

| Protected Attributes inherited from Loader | |

| Date | actualDate_ = Date() |

An Adjusted In Memory Loader,.

Definition at line 29 of file adjustedinmemoryloader.hpp.

| AdjustedInMemoryLoader | ( | const ore::data::AdjustmentFactors & | factors | ) |

Definition at line 31 of file adjustedinmemoryloader.hpp.

|

overridevirtual |

Reimplemented from InMemoryLoader.

Definition at line 24 of file adjustedinmemoryloader.cpp.

Here is the call graph for this function:

|

overridevirtual |

Reimplemented from InMemoryLoader.

Definition at line 38 of file adjustedinmemoryloader.cpp.

Here is the call graph for this function:| ore::data::AdjustmentFactors adjustmentFactors | ( | ) | const |

Definition at line 39 of file adjustedinmemoryloader.hpp.

|

private |

Definition at line 42 of file adjustedinmemoryloader.hpp.