Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <orea/app/analytics/scenarioanalytic.hpp>

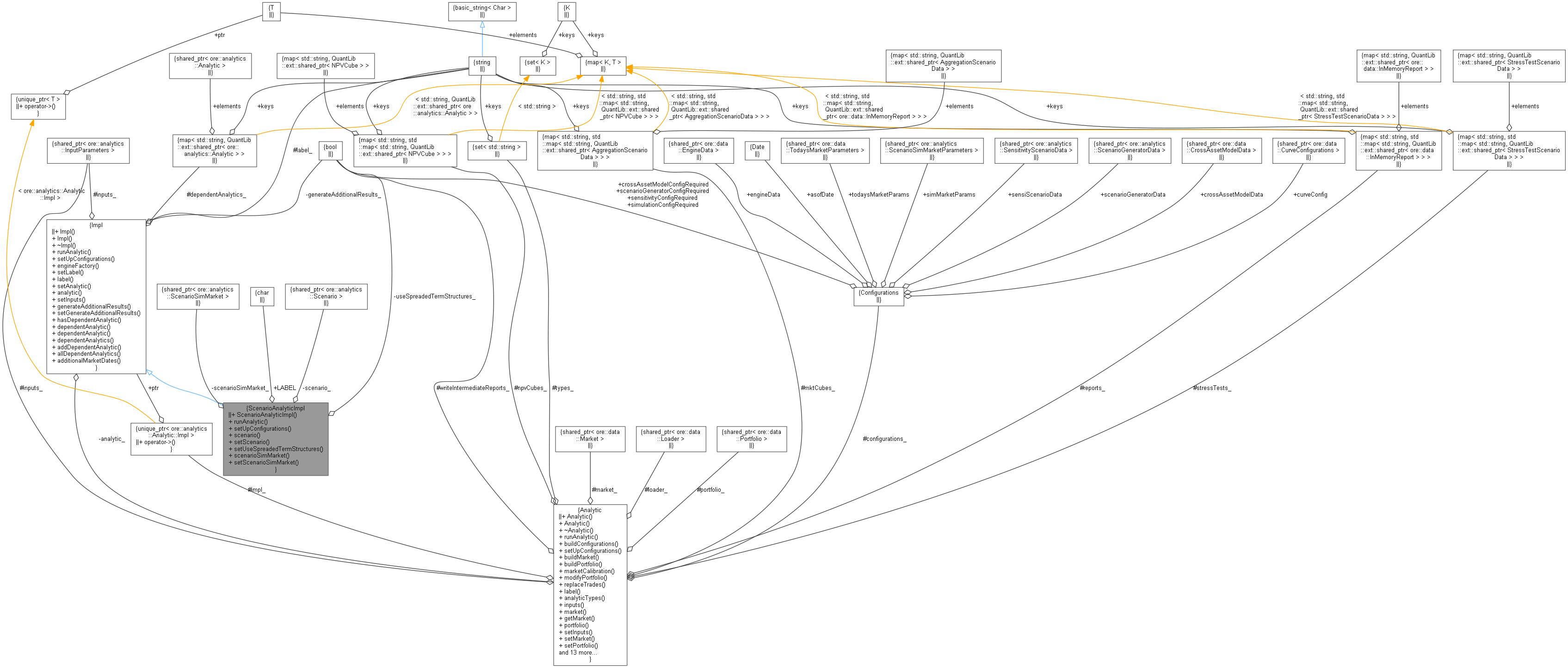

Inheritance diagram for ScenarioAnalyticImpl: Collaboration diagram for ScenarioAnalyticImpl:

Inheritance diagram for ScenarioAnalyticImpl: Collaboration diagram for ScenarioAnalyticImpl:Public Member Functions | |

| ScenarioAnalyticImpl (const QuantLib::ext::shared_ptr< InputParameters > &inputs) | |

| void | runAnalytic (const QuantLib::ext::shared_ptr< ore::data::InMemoryLoader > &loader, const std::set< std::string > &runTypes={}) override |

| void | setUpConfigurations () override |

| const QuantLib::ext::shared_ptr< ore::analytics::Scenario > & | scenario () const |

| void | setScenario (const QuantLib::ext::shared_ptr< ore::analytics::Scenario > &scenario) |

| void | setUseSpreadedTermStructures (const bool useSpreadedTermStructures) |

| const QuantLib::ext::shared_ptr< ore::analytics::ScenarioSimMarket > & | scenarioSimMarket () const |

| void | setScenarioSimMarket (const QuantLib::ext::shared_ptr< ore::analytics::ScenarioSimMarket > &ssm) |

| Public Member Functions inherited from Analytic::Impl | |

| Impl () | |

| Impl (const QuantLib::ext::shared_ptr< InputParameters > &inputs) | |

| virtual | ~Impl () |

| virtual void | runAnalytic (const QuantLib::ext::shared_ptr< ore::data::InMemoryLoader > &loader, const std::set< std::string > &runTypes={})=0 |

| virtual void | setUpConfigurations () |

| virtual QuantLib::ext::shared_ptr< ore::data::EngineFactory > | engineFactory () |

| build an engine factory More... | |

| void | setLabel (const string &label) |

| const std::string & | label () const |

| void | setAnalytic (Analytic *analytic) |

| Analytic * | analytic () const |

| void | setInputs (const QuantLib::ext::shared_ptr< InputParameters > &inputs) |

| bool | generateAdditionalResults () const |

| void | setGenerateAdditionalResults (const bool generateAdditionalResults) |

| bool | hasDependentAnalytic (const std::string &key) |

| template<class T > | |

| QuantLib::ext::shared_ptr< T > | dependentAnalytic (const std::string &key) const |

| QuantLib::ext::shared_ptr< Analytic > | dependentAnalytic (const std::string &key) const |

| const std::map< std::string, QuantLib::ext::shared_ptr< Analytic > > & | dependentAnalytics () const |

| void | addDependentAnalytic (const std::string &key, const QuantLib::ext::shared_ptr< Analytic > &analytic) |

| std::vector< QuantLib::ext::shared_ptr< Analytic > > | allDependentAnalytics () const |

| virtual std::vector< QuantLib::Date > | additionalMarketDates () const |

Static Public Attributes | |

| static constexpr const char * | LABEL = "SCENARIO" |

Private Attributes | |

| QuantLib::ext::shared_ptr< ore::analytics::Scenario > | scenario_ |

| QuantLib::ext::shared_ptr< ore::analytics::ScenarioSimMarket > | scenarioSimMarket_ |

| bool | useSpreadedTermStructures_ = false |

Additional Inherited Members | |

| Protected Attributes inherited from Analytic::Impl | |

| QuantLib::ext::shared_ptr< InputParameters > | inputs_ |

| std::string | label_ |

| label for logging purposes primarily More... | |

| std::map< std::string, QuantLib::ext::shared_ptr< Analytic > > | dependentAnalytics_ |

Definition at line 29 of file scenarioanalytic.hpp.

| ScenarioAnalyticImpl | ( | const QuantLib::ext::shared_ptr< InputParameters > & | inputs | ) |

Definition at line 33 of file scenarioanalytic.hpp.

Here is the call graph for this function:

|

overridevirtual |

Implements Analytic::Impl.

Definition at line 32 of file scenarioanalytic.cpp.

Here is the call graph for this function:

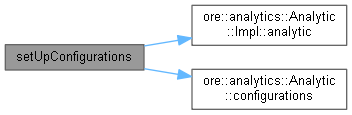

|

overridevirtual |

Reimplemented from Analytic::Impl.

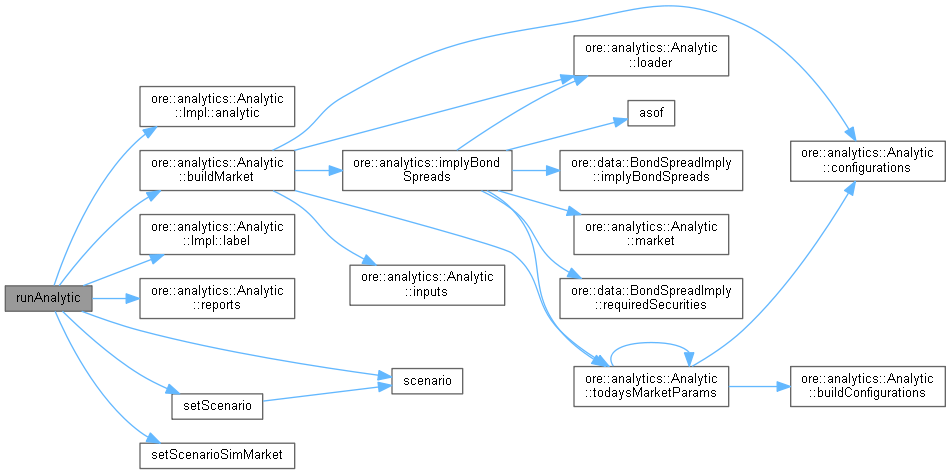

Definition at line 27 of file scenarioanalytic.cpp.

Here is the call graph for this function:| const QuantLib::ext::shared_ptr< ore::analytics::Scenario > & scenario | ( | ) | const |

Definition at line 41 of file scenarioanalytic.hpp.

Here is the caller graph for this function:| void setScenario | ( | const QuantLib::ext::shared_ptr< ore::analytics::Scenario > & | scenario | ) |

Definition at line 42 of file scenarioanalytic.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setUseSpreadedTermStructures | ( | const bool | useSpreadedTermStructures | ) |

| const QuantLib::ext::shared_ptr< ore::analytics::ScenarioSimMarket > & scenarioSimMarket | ( | ) | const |

Definition at line 47 of file scenarioanalytic.hpp.

Here is the caller graph for this function:| void setScenarioSimMarket | ( | const QuantLib::ext::shared_ptr< ore::analytics::ScenarioSimMarket > & | ssm | ) |

|

staticconstexpr |

Definition at line 31 of file scenarioanalytic.hpp.

|

private |

Definition at line 55 of file scenarioanalytic.hpp.

|

private |

Definition at line 56 of file scenarioanalytic.hpp.

|

private |

Definition at line 57 of file scenarioanalytic.hpp.